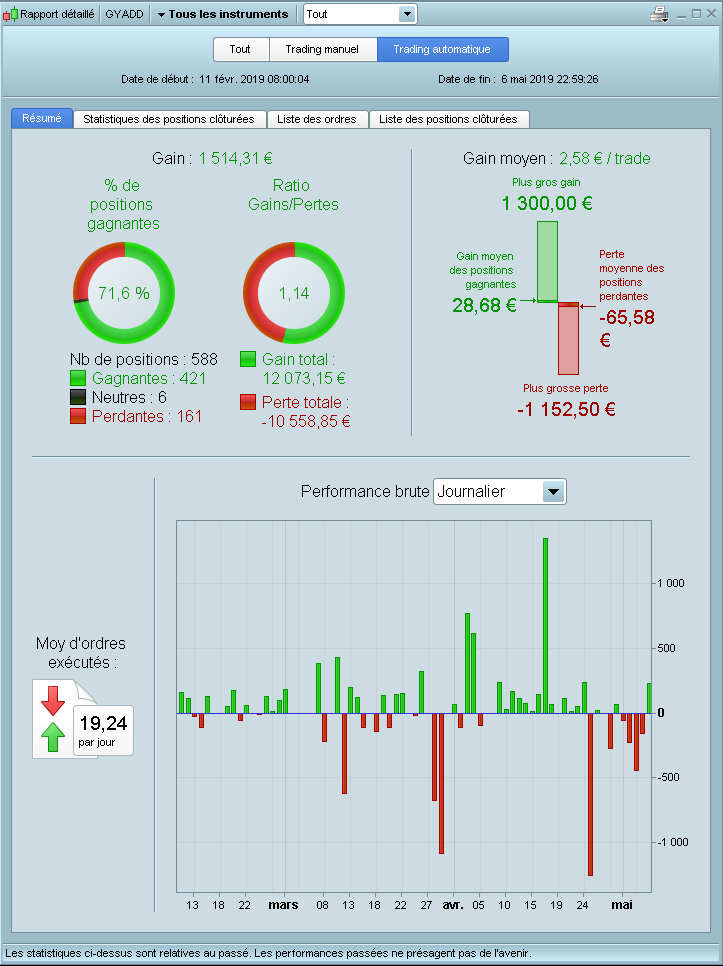

My live PRT

I’m going to profit this year so far. Unfortunately, I started a DAX 3 min algo that destroyed a nice trend I had.

The win is a bit better than the graph shows because I stopped an algo manually which would otherwise run over the weekend. The results of the two winnings do not show when I stop the algo with the mobile phone.

I stopped an algo manually

Do you stop algos manually often?

I used to do it, then stopped, but have started again to see if I can increase average gain per week / month etc. It is working so far! 🙂

My rationale for manual stop is that my Auto-Systems are imperfect and I can judge better direct with my eyes.

I also enjoy manual trading so this is a kind of halfway house / compromise … Auto entry and Manual exit! 🙂

Interesting thread. Is there a thread in this forum that evaluates the published strategies? How they perform forward? Would be an interesting read…

/P

How they perform forward? Would be an interesting read

There is, but nobody is

interested enough to spend a few minutes entering the data!? 🙁

This Thread enables us to share Systems that have been Forward Tested either Live or Demo.

My live PRT

What Timeframes are you trading on Moda?

My live PRT from 2019-04

Now i have got more stable returns.

I only run two algos on 5 min timeframe.

+300 Euro/1,5 months

I went through cycles of winning and then losing all or more of the winnings (although I always managed to (more or less) protect my initial capital), before finding my way of profitable algorithmic trading. I very much agree with

@jebus89 above; you need to run a portfolio of uncorrelated systems to reach any stability. But I am profitable. Not every day, not every week, not even every month. My objective is to be profitable on an annual basis, in the order of 15-25% on capital reserved for margin. Most of the time my margin requirements do not exceed 10% of my capital reserved for margin. If they do exceed 10%, it is invariably because several (hopefully) uncorrelated systems are in position simultaneously.

It takes a lot of work and you have to be really stubborn. It is really rewarding when it starts to work, because machines do it for you. But you can never stop developing and adapting. Markets change and you have to be prepared to change with them. Also, as you gain experience you refine your skills and your programs.

However, as a quantitative trader, be prepared to always chuck 99% of your work in the bin….

Daveys book is the basis for all of my trading now it provided a great framework

You can be profitable but as has been said you need to have a diversified set of trading systems and realistic expectations, you will not be able to have several hundred % returns each year and systems do not last forever, if you look at some of the systems that were added to the library a couple of years ago then most no longer work into todays market

Hi Nicolas,

Could you be more specific on this?

Thanks

Chris

Tip of the day: Wanna earn money easily? Make a simple ETF portfolio and wait.

Hi Nicolas,

Better with quote 😉

Can you be more specific on how to build this?

Thanks

sfl

sflParticipant

Average

“The people earning money with their automated strategies usually talk about things like: C++, Java, Python or any other programming language, 100.000 or 1.000.000 lines of code, connections next to stock market, teams of analysts, consistent adjustment of the strategy basket (right, not one strategy, multiple !) … how should then be something with less then 100 lines of code ever be successful”

Hi, I disagree.

If you want to code a full algorithmic trading framework, you need high level programming language and thousands of hours of work because you have to take care about getting data, streaming data handling event driven architecture and a very complex software architecture.

Thus, you cannot compare this kind of software with the strategy coding part only, they are just different because they are taking care of different resources.

I am on the idea of the smaller the simplier which means less chance of overfitting data.

If you have your own algotrading sw you have much more flexibility, this is something I agree with you, but this bring also complexity in management that sometimes can be very high expecially for someone who wants to automate for lacking of free time.

This is my opinion, the main issue with automatic trading is to understand that a system dosent work for good and that overfitting is the real enemy.

thank you for your opinion

In fact there’s some ways to check the overfitting’s weight in the results.

No experienced coder would ever start a system just after doing the backtest 🙂