may be you may advice the correct code to get the current position size which the latest capital can afford, thanks.

JS

JSParticipant

Veteran

This is the basic version that I use:

ONCE Capital = 10000

ONCE MarginPerc=0.05

IF StrategyProfit <> 0 THEN

Equity = Capital + StrategyProfit

Margin = Close * MarginPerc

MaxPosSize=Equity/Margin

EndIf

Instead of:

once capital=8888

if strategyprofit <> strategyprofit[1] then

capital = capital + (strategyprofit - strategyprofit[1])

endif

you can write:

once capital=8888

updatedCapital = capital + strategyprofit

so that you don’t have to do any math with the outcome of the strategy so far.

Hi WingYip

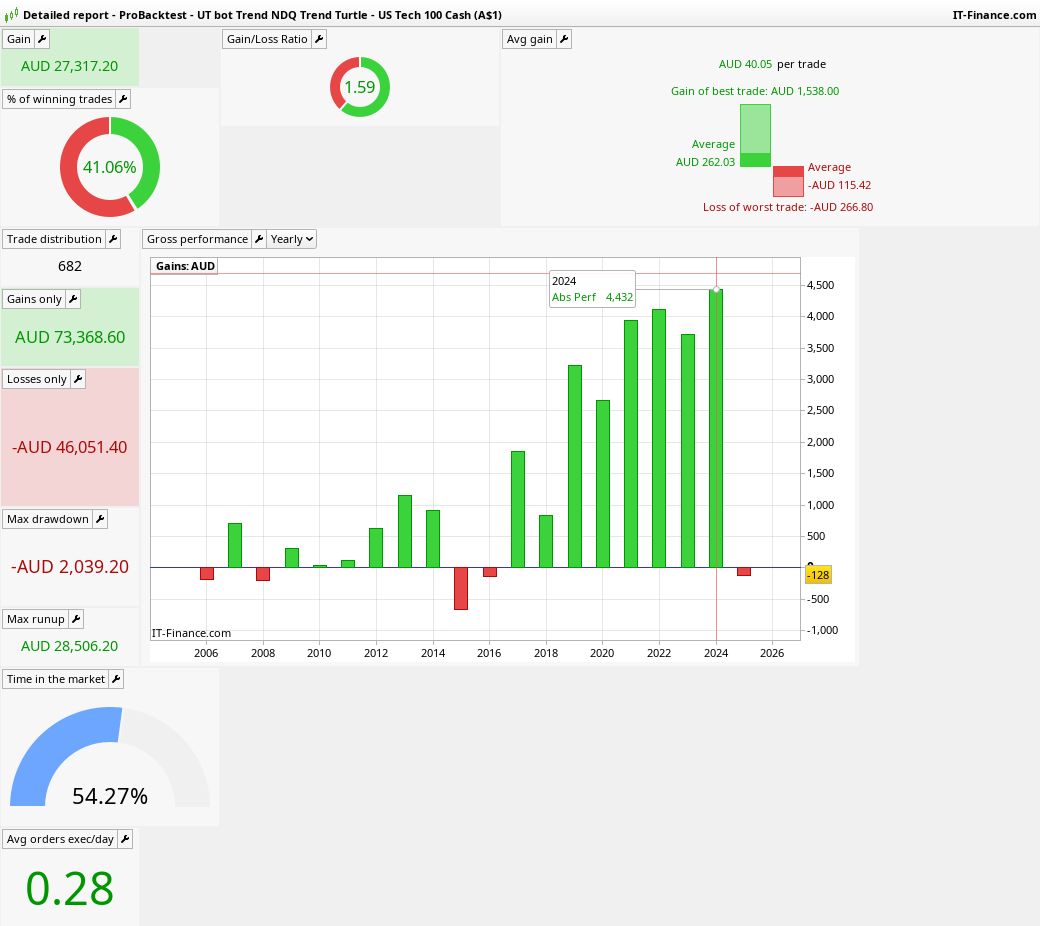

You either invented an „ATM“ spitting out kind of unlimited cash every day / week / month, or a perfect cash burning system, so perfect not for you but for your broker. While I assume you believe having invented an ATM, I will try to collect my thoughts about why it could be possibly an AAM: account annihilation machine. I whish of course your equity grows kind of exponentially in live trading as it grew in backtest, yet personally I would not „buy“ such system because it does not match by far my criteria of „sound system“ – in fact its performance parameters are quite opposite of what I am expecting from competitive approach/trading system. So here you are:

Win rate of your system is ~ 80%

I think in trading markets one has to figure out how to a) survive and b) earn money by having win rate of 20% (ok, does not have to be exactly 20%, can be 10% or 30% – anyway well below 50%). I think high rates shown in any backtests are simply not sustainable, they will not continue. Or if they continue, account still might be wiped out – and this is because of other paramter, which is kind of always same behind systems with huge win rates:

Avrg losing trades of your system are significantly bigger than avrg winners (in your system by ~ 1.5 times)

I think in the competitive system avrg winners have to be 2x or 5x or 10x bigger than avrg losers, anyway bigger or much bigger than the losers.

You might think you are okay with your avrg losers being bigger than winners – because anyway 80% of your trades are winners, so „probabilities“ are on your side? I don’t know how to express or explain that, but „win rate“ of what ever % is not a probability. It is not a probability in the common sense like we know it from school or university, it is not a probability at all. According your backtest you had 5 consecutive losers at maximum. What about if you have in the future 15 consecutive losers? Or 25? You think it’s kind of impossible because you have proven 80% probability of winning? Long, very long series of losers might come sooner than you think, and more frequent that you think is possible with the (historical) win rate of 80%.

You tell you increase position after losing trades. Check out then what happens with the equity if you have 15 or 25 consecutive losers and after each one you increase the position. Will you be comfortable with the outcome? Will you continue trading? And it does not have to be consecutive losers: check out what happens if you have winner/loser/winner/loser… etc with 15 winners and losers following each other and after each loser you increase position.

You tell:

„as long as the core system is a overall winner, the money management is a bonus“

I would like to say – no, it’s not a bonus. it’s crucial part of the overall strategy.

Broker’s agents looking at your system’s backtest performace would probably cry to you „perfectly done! Put now maximum money to your account and run it live“.

I tried to do the opposite. Maybe it inspires you, and maybe even saves you some hundreds or thousands of BGP. I wanted to make you a bit sceptical when ever you see (or develop yourself) a system with exponential equity growth. With some tricks and „optimization“ it’s not so difficult to develop such backtests. But markets are not ATMs.

Cheers

justisan

Did anyone not notice the initial stat report posted didn’t include brokerage? That is NOT a sleep at night algo. It looks fantastic but it could be a Never Sleep Again algo. I’ve done that by mistake once or twice and everything I did was amazing.

So much so I sit down with my 6 and 8 year old and demonstrate the ‘Disappearing Island’ and explain to them why brokerage is the best business ever created (for the brokers). We are in the wrong game! But why the expectations? Because one is approaching it from an income perspective. Trying to make algos look like a paycheck is a tough ask, but have no doubt some can pull it off. Everything in wealth creation is divided by TIME. That is where expectations fall flat on their face.

Justisan is soo right. I worked out some time ago why so many others fail and it is not knowledge or capabilites, it is about expectations being far far too high OR in some cases

needs being too great relative to account size and outgoings. Achieving profit after expenses is not a unique trading problem, it’s any businesses growth problem. It’s why large accounts win. PeterSt once said I think that it all looks very different once you have all the money you need to live. 40% months manually sure, why not. I’ve done it before and Tom Houguard is doin it right now. Automatically though? Realistically for an entry level quant(2yr live) like me? Mid time frames, Gain/Loss 1.3-2, 10%DD and 40-56%WR. A basket of little correlated ‘Slow Bots’ as I call them can comfortably net you 0.8-1% per week. Not only that they are easy to find and run off a few lines of code = robust. So if you gear that to a low DD, say 5% and an average year nets you 60-85% ROI. This is

without compounding and

without withdrawals then that is as good as I can get it so far and it’s very realistic expectations for algorithmic trading after many many hrs work. I hope that encourages someone, because at the start you don’t know what to aim for. Buy and hold is a joke, a scam. But so is the Dissapearing Island, a mirage. Some don’t achieve because scared or bored with the idea of slow growth that they don’t even try again because expectations are too high and the mind only wants to protect from failure of meeting that high price.

Next there is the obvious relationship between RR and WR. Take any bot you have (I know everyone has done this) instead of 1:1 make it 1.5:1 or neg RR. Of course our WR goes up but stability goes way down and usually profit. Now the next test, same thing but remove any targets and add a trailing stop or even a super tight stop then watch your trade size soar and your WR go Kaput. If you resonate with those sentences then you are way past surviving in markets. Now, pick a style that you can live with, just like a wife because one needs a serious commitment to their bots and work to follow through.

Then of course as Justisan nearly alluded too, win rate is not static. Just a feel good number, and who doesn’t want that?

That’s probably enough from me. I’m very passionate about these topics and particularly Expectations divided by Time as that is what set me free in the end. Everyone can train the ability.

CC

Thank You for your wise words coincatcha.

initial stat report posted didn’t include brokerage

Are you saying ‘broker spread’ is also missing from initial stat report or are you refering to (just) overnight fees etc that are not included in initial stat report?

Grahal, I noticed Brokerage missing on the report. If brokerage is missing, then I think also ‘What else is missing?’ Every time I approach any topic in trading it must be asked what is real and what is fake? I ask these of every strategy and every paradigm in my head… every topic I read. We all, no matter how smart or prepared or how well capitalised we enter markets —–you guessed it, we learn through the school of hard knocks.

I ran something similar (except the WR) once. I wanted a new car by Christmas and my live testing and backtesting told me I was going to get it. I showed the worst of it in the PRA thread in 2023. We all had that drawdown, the US markets ate retail algos and ground us into paste. Only the ones with conviction and appropriate expectations survived. Thankfully I traded my way out but with a huge lesson learnt and hopefully to the benefit of others here.

I think once a trader has churned 200K on 150 or more live tests over YEARS then they have a pretty good feel for what can be done. That’s what it took me anyway.

Maybe be a bit late to the thread to also try and help Wingyip from a very painful experience. It’s at that point in the DD like Justisan said, Are you feeling lucky? Because that is the exact point a trader loses money that cannot be made back in the same fashion and switches it off. Now they strategy jump.

Imagine if Gavel (I think his name was in the PRA thread), didn’t keep the basket of bots running? Now go and look at their equity curve from the Oct low ’23. The start of the largest runs in history. I wouldn’t of had a new car by Christmas, but I would have had a new second hand car by Feb.

Expectations.

Regarding

expectations… It came to my mind what some former portfolio manager once told as a joke, more or less like this: „People buy a lottery ticket and expect to win 5 million. Exactly same way they trade markets“.

While it’s sure extremely exaggerated analogy, I think it is still quite good description of the state of mind of the majority pouring every day into this business of trading. Very little capital + almost no effort, yet enormous expectations towards earnings. Not saying that I myself was so much different in the beginning 😊

Hand in hand with above goes usually also disrespect/ignorance for risk side of the business. Here in particular I mean simply the drawdowns, their magnitude, frequency and their length. Just recently I came across the post of some system/bot-seller, announcing his system-portfolio’s January 2025 result of +50% and commenting himself that result as „hard to beat“. Really? Few months ago in 2024 same portfolio made -50% in one month (almost sure the drawdown was bigger than that…) – yep, still hard to beat? I would say “hard to trade” – or rather impossible, psychologically.

I think folks very much overestimate their mental ability to stand their trading losses. They might really think they can stand loss of -50% of capital in one month, maybe because they made +30% + 20% +50% in the months before. I assume one can stand it – if one has an account of 500EUR and it does not matter / does not „hurt“ for the person in case it’s lost in the end. But will one trade that portfolio with such risk parameters when having in the account 50k? 500k? 5m? 50m? possibly also managing other people’s money?

Coincatcha,

Amazing that you were able to explain your 6 and 8 years old how cool brokerage business is. Are you able also to explain to them trading/speculating? My 8 years old sometimes comes to me and asks what I am doing. I think so far she got only that I am buying something and selling something. And that it is not apples what I am trading. Most of all she likes to change colours of my price charts! Maybe some day in the future her excitement goes beyond that…

Cheers

justisan

<p data-start=”0″ data-end=”88″>My neighbor, who works for an FX fund, once told me: <em data-start=”143″ data-end=”355″>”We’re all just like kids picking up stones on the railway tracks. We hear plenty of warning signals, but most of the time, the train doesn’t come. But one day, it actually will—and a lot of kids will get hit.”</p>

<p data-start=”0″ data-end=”88″>With a relativlly large stop loss and multiple steps to exit winning trades, achieving a “good result” like this isn’t particularly difficult. However, the real challenge lies in managing risk before that inevitable train arrives. This strategy might be well-suited for trading QQQ options.</p>

@Justisan

It’s always fun watching children try and work out what we are doing. To be honest, my 8yr old has a far greater understanding than my in-laws because he grasps the probability concepts as to systematic approaches. And yes he has grasped not so much the financial markets/instruments but that EVERYONE is trading something. Be it time/skill for money or a tangible asset. That is what I was hoping to teach him.

@dipont

Nice analogy. With every man and his dog able to write a profitable Nasdaq algo, and particularly since 2020 the results booming, I do wonder for how long? Something like the strategy in this thread perhaps could capitalise very quickly but would fall over just as fast? This is a phenomena I’m monitoring very closely, these outsized gains I have benefited from but choose to run a regime filter to cut out below a 1hr 1000ma so as to trade a bit slower. For all of them I have a volatility setting that makes them still profitable should the range ever die back. Not a bet I want to place as what are the chances technology stagnates? but ready nonetheless.