Coding the Kase Convergence/Divergence indicator?

Is there anyone that would like to convert Cynthia Kase’s Convergence/Divergence indicator?

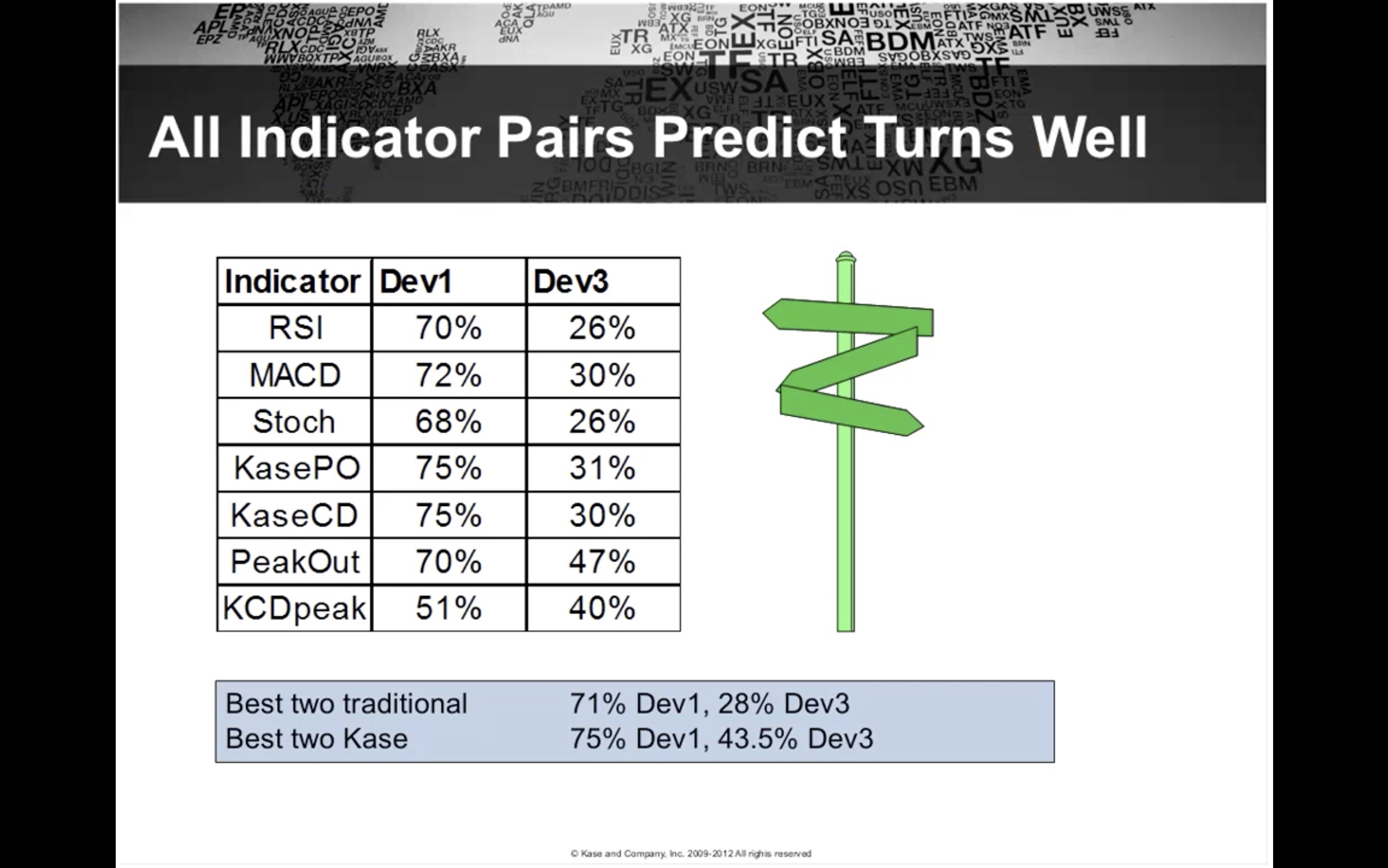

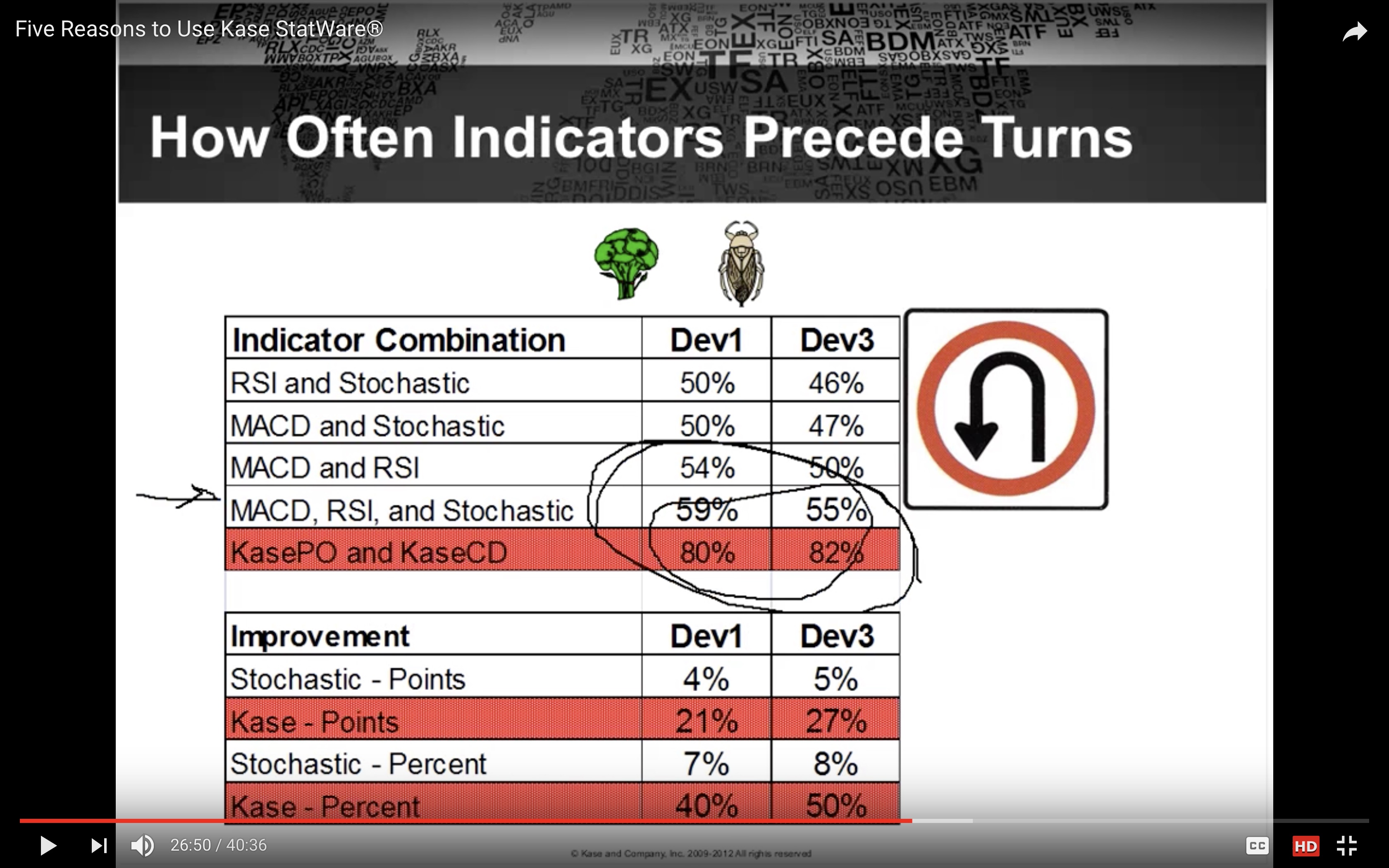

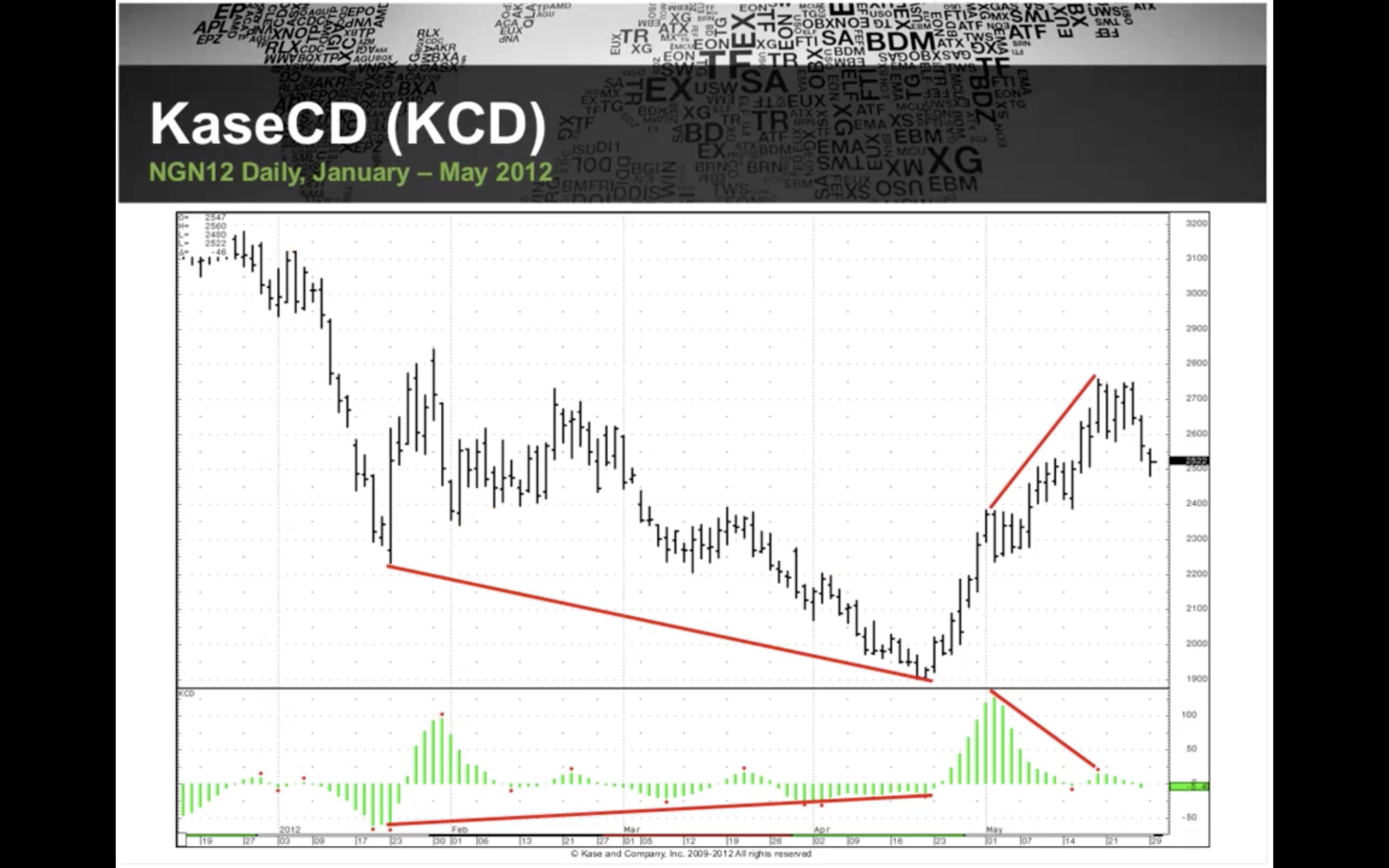

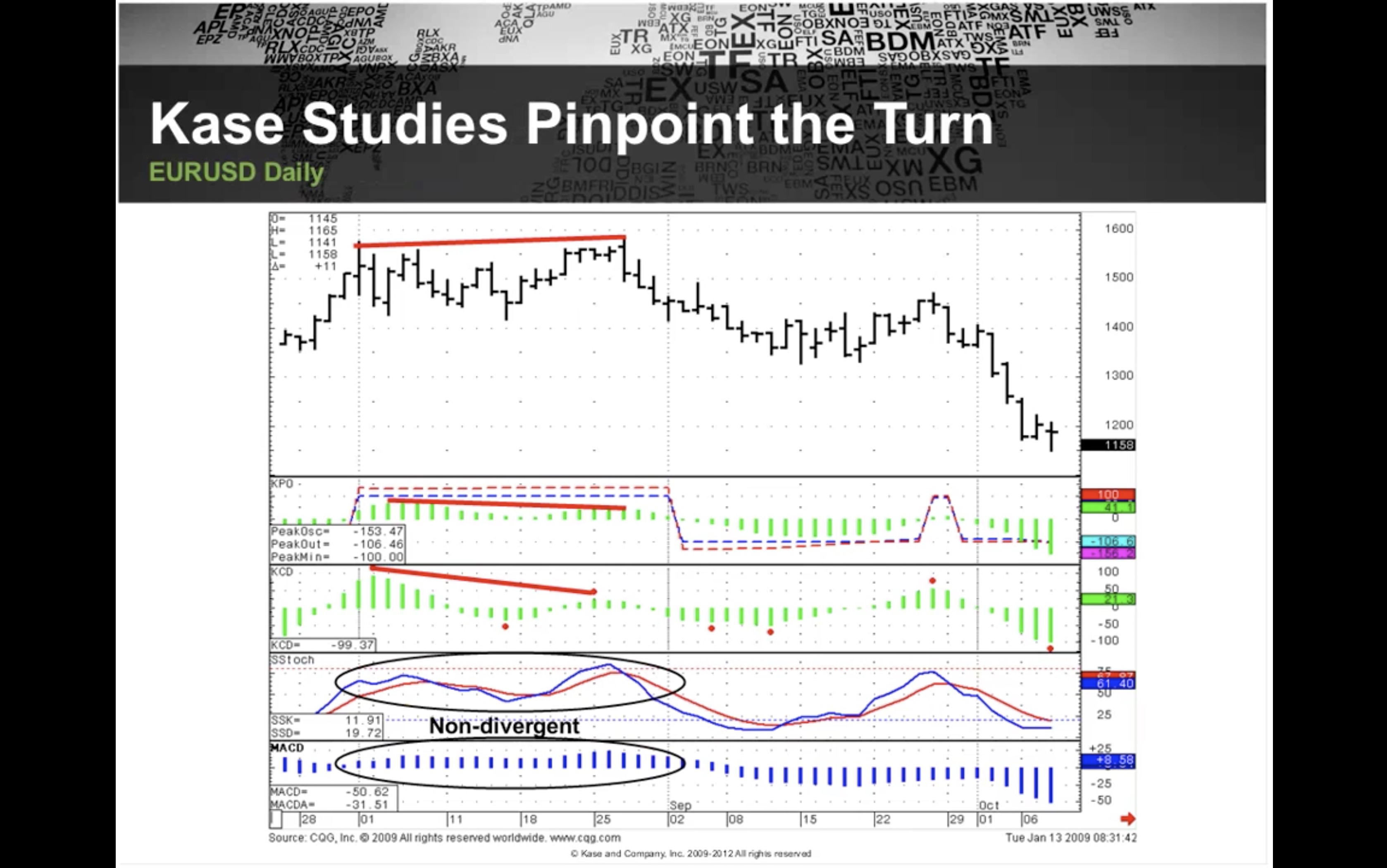

Kase has already statistically proven the validity of using her Kase Peak Oscillator (KPO) combined with the Convergence/Divergence (KCD) indicator and it out performs conventional indicators like RSI and MACD for picking out market turning points:

http://www.kaseco.com/support/articles/Proof_That_Technical_Analysis_Really_Works.pdf

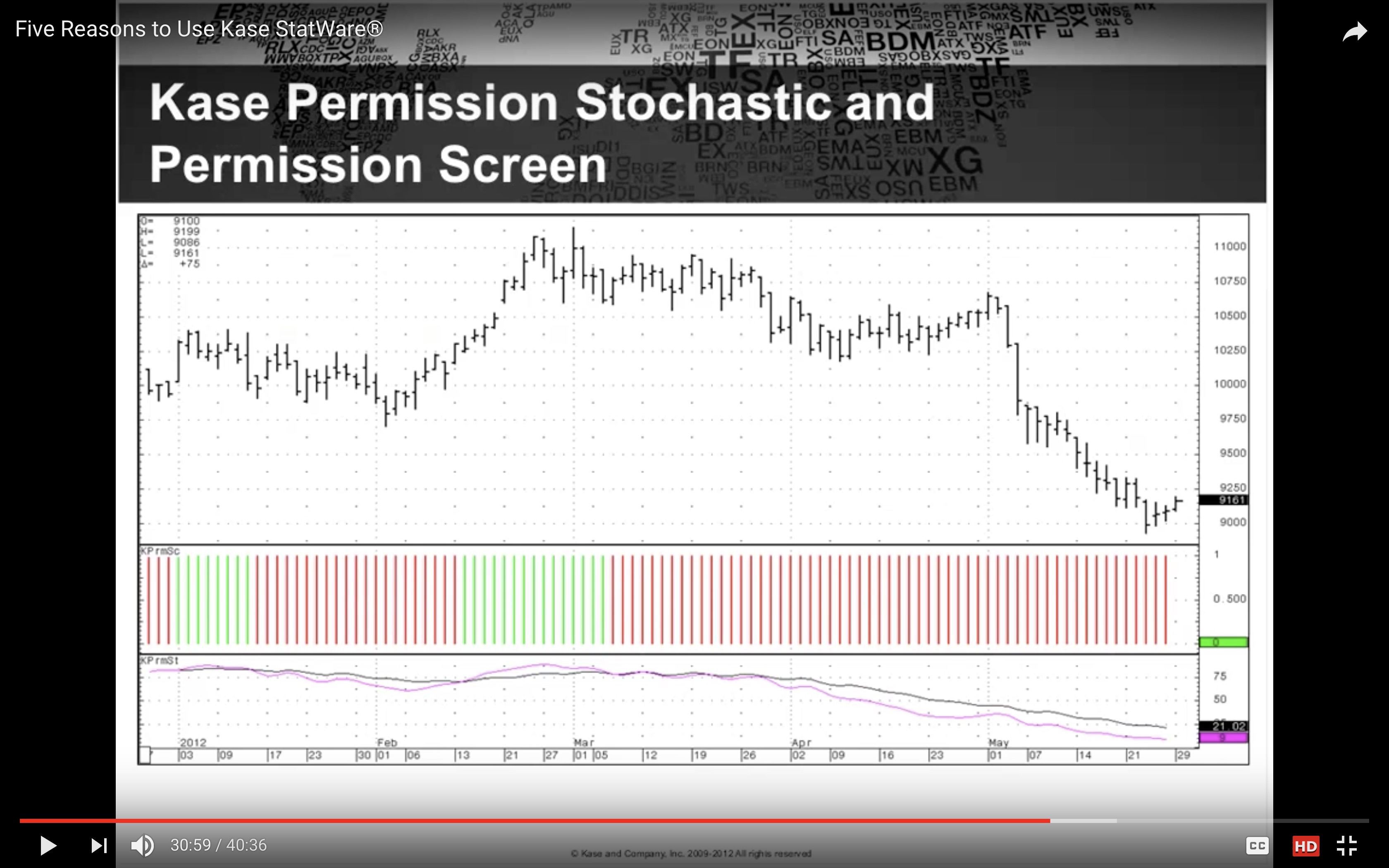

Using the KPO and Kase’s Dev Stops have produced more profitable results — on many different currency pairs and also Brent Crude, the Dow and DAX, (just change which Dev Stop to use due to individual markets having their own volatility profile) — than any other system/indicators I’ve used on PRT including the stunning John Ehlers indicators.

As @nicolas pointed out to me, the danger with mean reverting systems is that they can also potentially get you in on the wrong side of the trade resulting in wider movement against your position before the Dev Stop closes the position.

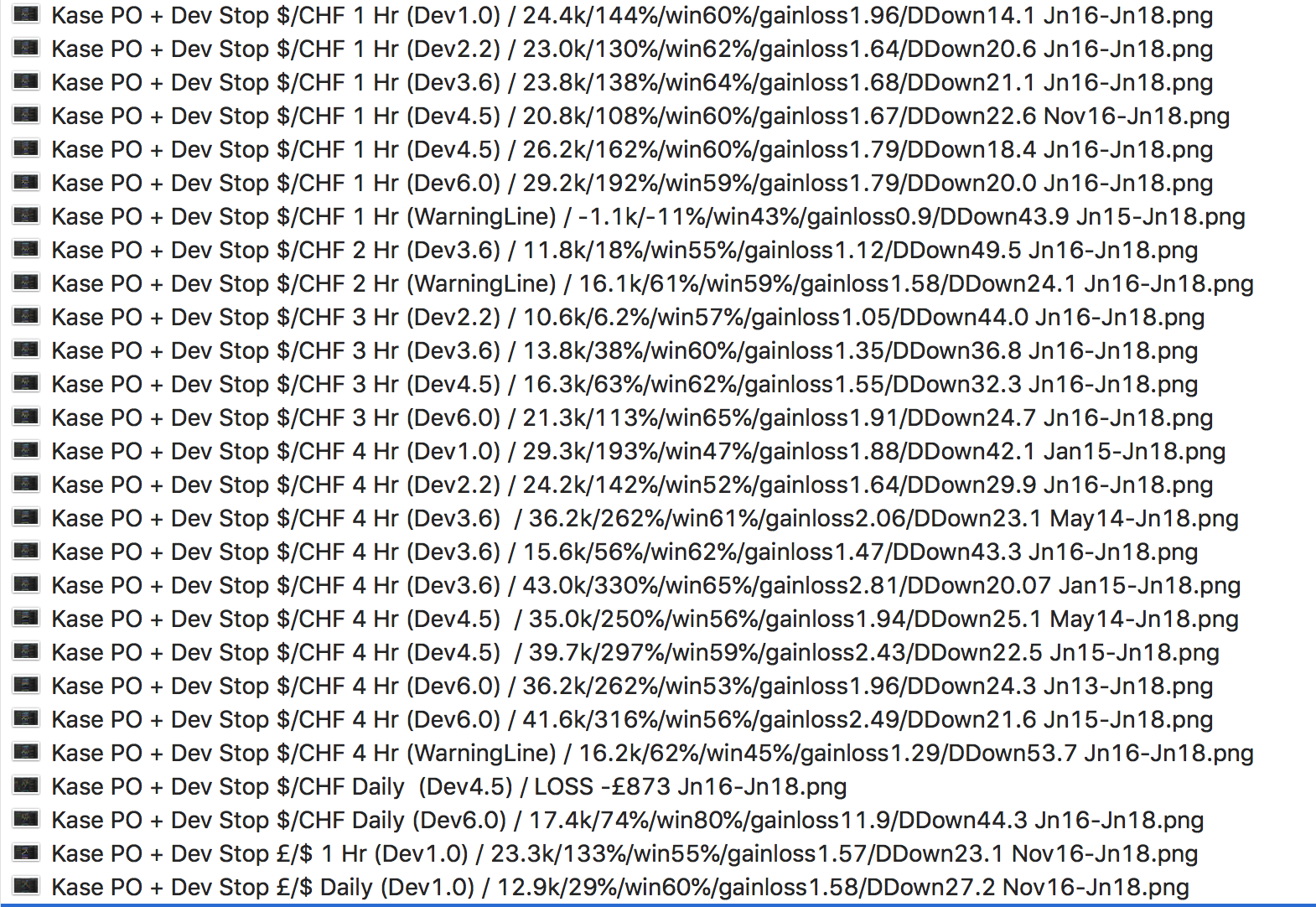

When testing, look at the Maximum Adverse Excursion column figures in the Detailed Report to gauge validity. I have taken out the ADX > 25 part of the entry code to minimise complexity and help future results being less robust than back tests. The simpler the system with the less parameters the more robust it will be in the future.

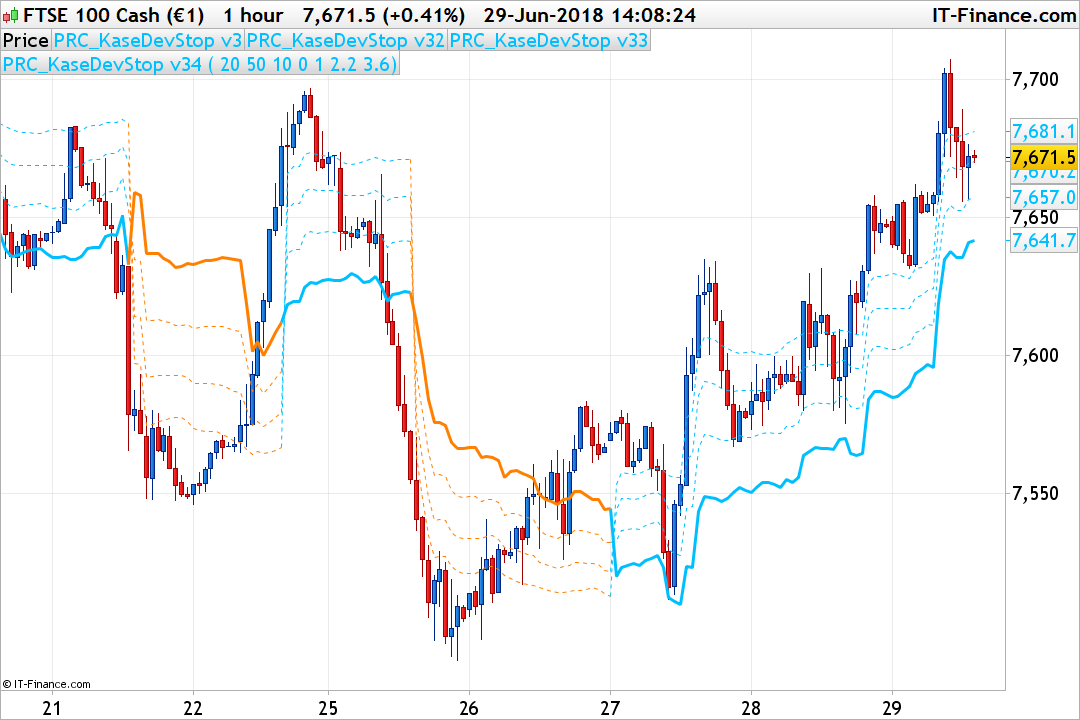

Please see screen shot for results on the (stable) Swissy (USD/CHF) usingi different time frames and Dev Stops:

The code for the KPO is on this forum as is the code for the Kase’s Dev Stops is below (check out KRev (Reversal) Amounts too to calculate your monetary risk per trade per Dev Stop stop line).

If anyone would like to add to this code below, maybe try different financial instruments or maybe add a trend filter or perhaps a Choppiness Index/Kaufman Efficiency Ratio – I haven’t had time yet – please feel free and post your results here.

When adding a Trailing Stop results were sometimes better, sometimes worse.

Thanks a lot,

Bard

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

// Conditions to enter long positions

ignored, ignored, ignored, ignored, indicator2 = CALL "Kase Peak Oscillator"

c1 = (indicator2 < 0) //Kase Pink Bar Peak Out Entry

IF c1 THEN

BUY 10 PERPOINT AT MARKET

ENDIF

// Conditions to exit long positions

ignored,ignored,ignored,ignored,indicator3, ignored = CALL "Kase Dev Stop Lisse +SAR+4.5/6"

c2 = (close CROSSES UNDER indicator3) // Kase Dev Stop 4.5

IF c2 THEN

SELL AT MARKET

ENDIF

// Conditions to enter short positions

ignored, ignored, ignored, ignored, indicator5 = CALL "Kase Peak Oscillator"

c3 = (indicator5 > 0)

IF c3 THEN

SELLSHORT 10 PERPOINT AT MARKET

ENDIF

// Conditions to exit short positions

ignored,ignored,ignored, ignored,indicator6, ignored = CALL "Kase Dev Stop Lisse +SAR+4.5/6"

c4 = (close CROSSES OVER indicator6)

IF c4 THEN

EXITSHORT AT MARKET

ENDIF

//KASE DEV STOP + 4.5 + 6.0

//Settings

n=30

p1=1.0

p2=2.2

p3=3.6

p4=4.5

p5=6.0

difference=0

Hg=highest[2](high)

Lw=lowest[2](low)

DTR=max(max(Hg-Lw,abs(Hg-close[2])),abs(Lw-close[2]))

aDTR=average[n](DTR)

for i=0 to n-1 do

difference=difference+square(DTR[i]-aDTR)

next

difference=difference/n

sdev=sqrt(difference)

dev0=close-aDTR

dev1=close-aDTR-p1*sdev

dev2=close-aDTR-p2*sdev

dev3=close-aDTR-p3*sdev

dev4=close-aDTR-p4*sdev

dev5=close-aDTR-p5*sdev

if dev0<dev0[1] and close>dev5[1] then

dev0=dev0[1]

endif

if dev1<dev1[1] and close>dev5[1] then

dev1=dev1[1]

endif

if dev2<dev2[1] and close>dev5[1] then

dev2=dev2[1]

endif

if dev3<dev3[1] and close>dev5[1] then

dev3=dev3[1]

endif

if dev4<dev4[1] and close>dev5[1] then

dev4=dev4[1]

endif

if dev5<dev5[1] and close>dev5[1] then

dev5=dev5[1]

endif

dev6=close+aDTR

dev7=close+aDTR+p1*sdev

dev8=close+aDTR+p2*sdev

dev9=close+aDTR+p3*sdev

dev10=close+aDTR+p4*sdev

dev11=close+aDTR+p5*sdev

if dev6>dev6[1] and close<dev11[1] then

dev6=dev6[1]

endif

if dev7>dev7[1] and close<dev11[1] then

dev7=dev7[1]

endif

if dev8>dev8[1] and close<dev11[1] then

dev8=dev8[1]

endif

if dev9>dev9[1] and close<dev11[1] then

dev9=dev9[1]

endif

if dev10>dev10[1] and close<dev11[1] then

dev10=dev10[1]

endif

if dev11>dev11[1] and close<dev11[1] then

dev11=dev11[1]

endif

if close>dev11[1] then

flag=-1

else

if close<dev5[1] then

flag=1

endif

endif

if flag=-1 then

ind0=dev0

ind1=dev1

ind2=dev2

ind3=dev3

ind4=dev4

ind5=dev5

//k=1

r=0

g=191

b=255

else

ind0=dev6

ind1=dev7

ind2=dev8

ind3=dev9

ind4=dev10

ind5=dev11

//k=-1

r=255

g=128

b=0

endif

//ORANGE AND LIGHT BLUE

return ind0 coloured(r,g,b) style(dottedline,2) as "Warning Line", ind1 coloured(r,g,b) style(dottedline,2) as "Dev Stop 1.0", ind2 coloured(r,g,b) style(dottedline,2) as "Dev Stop 2.2", ind3 coloured(r,g,b) style(line,2) as "Dev Stop 3.6", ind4 coloured(r,g,b) style(dottedline,2) as "Dev Stop 4.5", ind5 coloured(r,g,b) style(line,2) as "Dev Stop 6.0"