Bard

BardParticipant

Master

Yes that would make sense, more likelihood of clashing orders in a 1 min TF compared to daily or 4 hr. When I decreased the boxsize from 100 to 50 I then got a tbt warning whereas before it hadn’t given me tbt warning during the 100 boxsize test?

BardParticipant

Master

@Vonasi, even just having”dead” optimisation variables for qty and Random left in a system, despite no actual VRT code in the system, makes a difference to the results.

I just compared the same system today with a screenshot of profit results from a few days ago. The system today has no VRT code as I stripped it out, but it still contained “dead” optimisation settings (Q: 2 to 10and R: 1 to 10) at the top.

I could not replicate the results today with those from a few days ago? I had to delete the Q and R settings from the optimisation variables window first before the results then matched with those of a few days ago? Any ideas!?

The question though, is why is the VRT code giving different results compared to a non VRT system with the same code?

Not sure what you mean and I can’t get anything useful from your screenshot because I don’t have a magnifying glass powerful enough.

Do you mean that you have a strategy with the VRT code in it but turned off and an identical strategy but with no VRT code in it at all and they return different results? If so then the only answer can be because the strategy part of the code is not identical or the variable settings are not identical or they are being tested on different data samples.

I had to delete the Q and R settings from the optimisation variables window first before the results then matched with those of a few days ago? Any ideas!?

I don’t recall the variables being called Q and R in the robustness tester – they were Qty and Random – or are you abbreviating? If not then perhaps there are variables in the strategy code called Q and R – as I say I’ve not looked at the code.

I don’t recall the variables being called Q and R

I changed them to q and r cuz i’m lazy. Bard has my version of the VRT

BardParticipant

Master

Not sure what you mean and I can’t get anything useful from your screenshot because I don’t have a magnifying glass powerful enough.

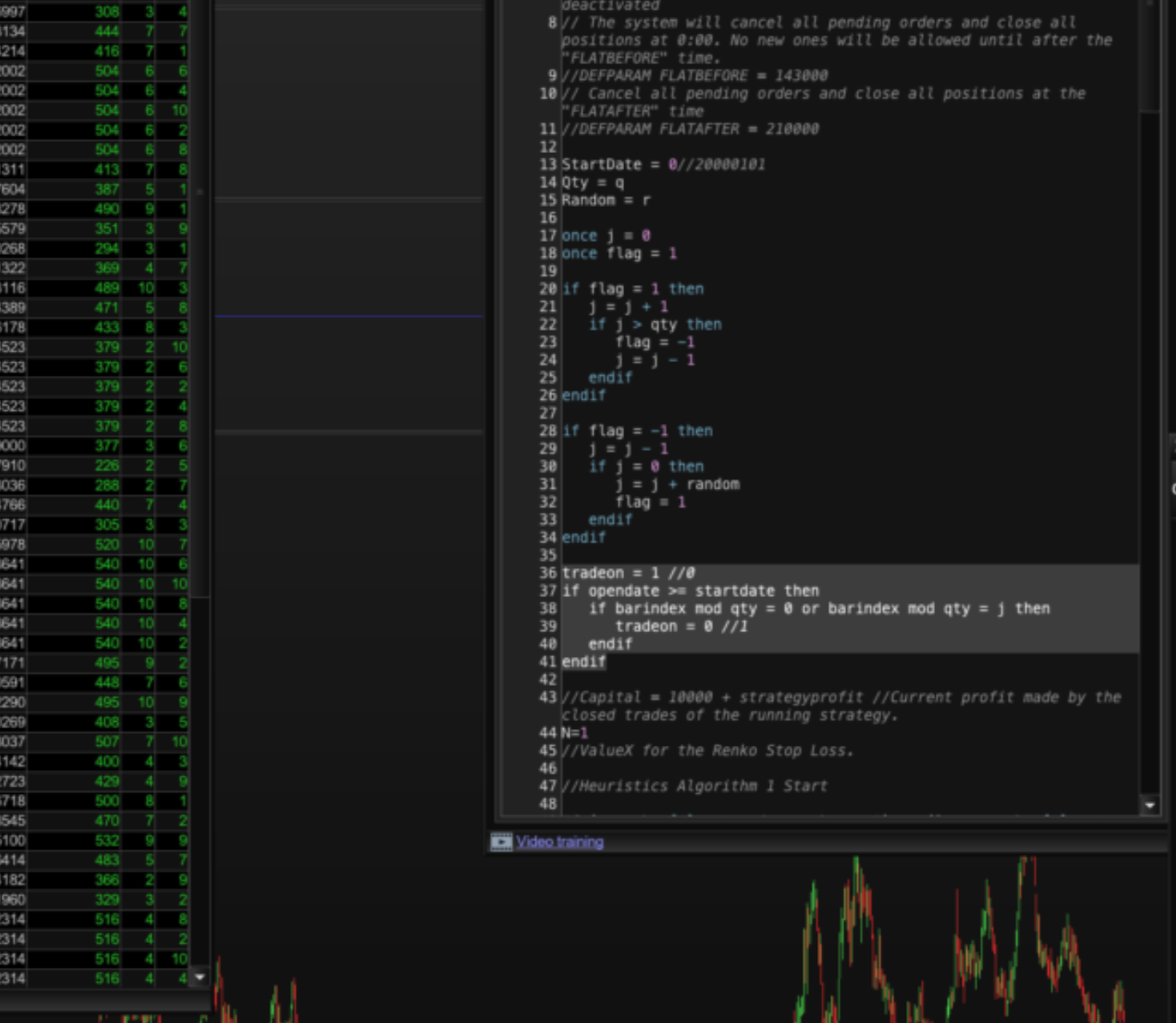

The screen relates to tradeon=1 and it not working to turn off the VRT. The screenshot was taken on a 50″ LG tv. This is it zoomed in: Pls see image.

Do you mean that you have a strategy with the VRT code in it but turned off.

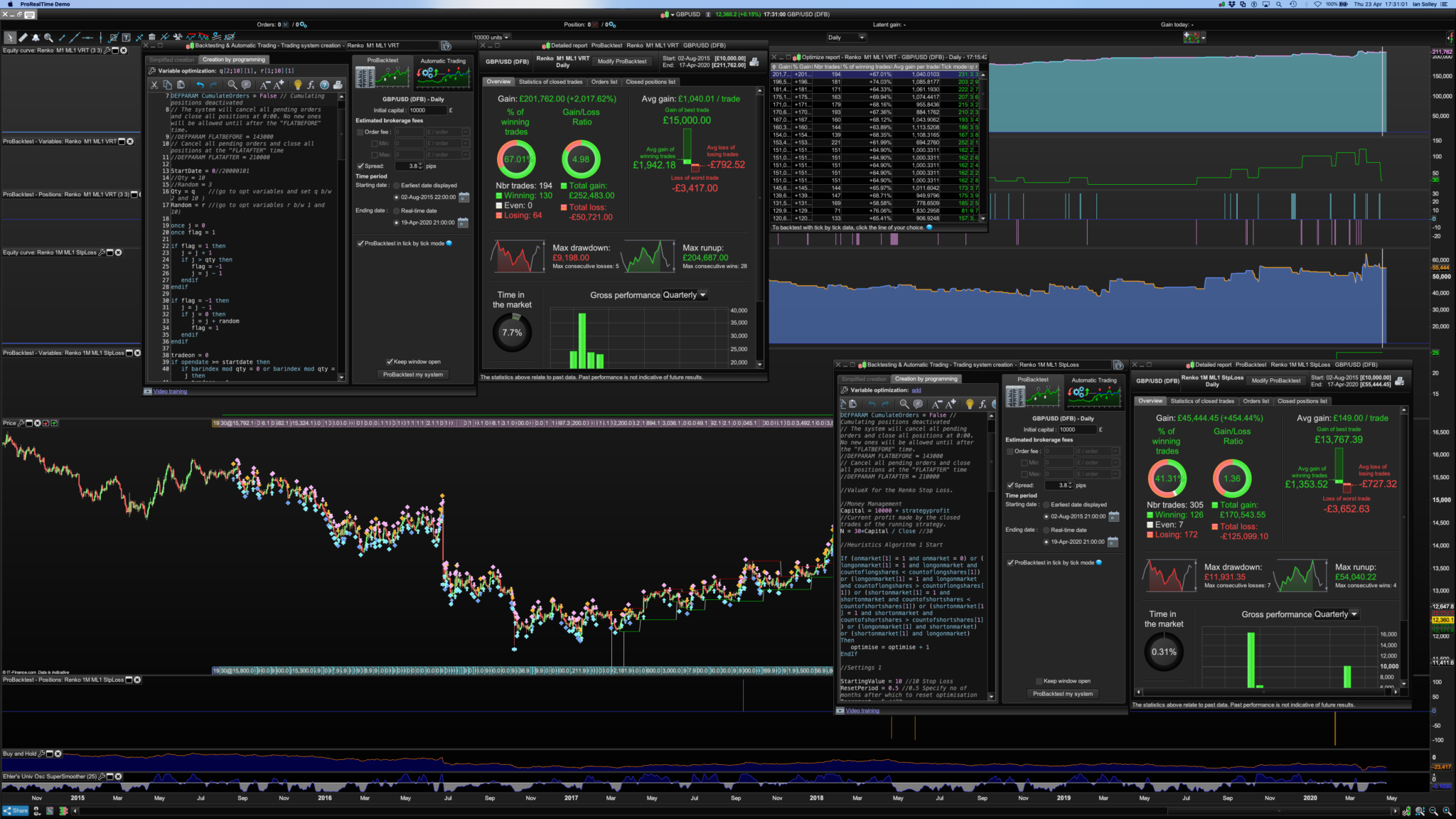

Yes, all rem’d out and tradeon taken out of “If buy and sell statements.” The only part of the VRT I left in was the variables in the very top of the system creation window and it made a big +ve difference to the profits. (Yes they’re abbreviations for qty and random). I can also test a non VRT system against a complete (and non rem’d) VRT coded system and the results are very different compared to the non VRT version but I’m guessing that’s not meant to happen? Pls see screen with VRT version makes £211k – top equity curve whilst Bottom equity curve and not a VRT system makes £55k:

Code otherwise identical thanks to text-compare.com

When you said:

“Click on the avg gain per trade tab in the optimiser window to organise the results in low to high and also drag the results into Excel.“

Did you mean that the smallest numbers at the bottom and largest at the top, only reading the Robustness thread I saw GraHal had a google spreadsheet with the smallest values at the top and the largest at the bottom which threw me? I’m really looking forward to getting Excel to behave and using this great piece of kit! Cheers.

Did you mean that the smallest numbers at the bottom and largest at the top

No – smallest at the top. Excel draws graphs using values from the top of the data to the bottom. You will notice that all the graphs slope up from left to right so that is low to high.

I just downloaded and imported Nonetheless’s last posted ITF and added the code I posted earlier to allow me to turn the VRT on or off and it worked just fine. With VRT off all the results were identical and with it on they were all different. I then // out all the VRT code and just left tradeon = 1 in the code and it returned one result that was identical to with the VRT code in the strategy but turned off.

This works well for modifying the period and type of an MA. I included an on/off so can be isolated.

ONCE EnableHeuristics = 1

If EnableHeuristics = 1 then // Start of Heuristics Algorithm 1

If onmarket[1] = 1 and onmarket = 0 Then

optimize = optimize + 1

EnDif

StartingValue = 45

ResetPeriod = 10 //Specify no of months after which to reset optimization

Increment = 5

MaxIncrement = 10 //Limit of no of increments either up or down

Reps = 20 //Number of trades to use for analysis

MaxValue = 75 //Maximum allowed value

MinValue = 25 //Minimum allowed value

once monthinit = month

once yearinit = year

If (year = yearinit and month = (monthinit + ResetPeriod)) or (year = (yearinit + 1) and ((12 - monthinit) + month = ResetPeriod)) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

monthinit = month

yearinit = year

EndIf

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

//once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

//Graph StratAvgA*-1 as "StratAvgA"

//once BestA = 300

//GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

//once BestB = 300

//GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// End of Heuristics Algorithm 1 ; Start of Heuristics Algorithm 2

If onmarket[1] = 1 and onmarket = 0 Then

optimize2 = optimize2 + 1

EnDif

StartingValue2 = 3

ResetPeriod2 = 10 //Specify no of months after which to reset optimization

Increment2 = 1

MaxIncrement2 = 8 //Limit of no of increments either up or down

Reps2 = 20 //Number of trades to use for analysis

MaxValue2 = 8 //Maximum allowed value

MinValue2 = 0 //Minimum allowed value

once monthinit2 = month

once yearinit2 = year

If (year = yearinit2 and month = (monthinit2 + ResetPeriod2)) or (year = (yearinit2 + 1) and ((12 - monthinit2) + month = ResetPeriod2)) Then

ValueY = StartingValue2

WinCountB2 = 0

StratAvgB2 = 0

BestA2 = 0

BestB2 = 0

monthinit2 = month

yearinit2 = year

EndIf

once ValueY = StartingValue2

once PIncPos2 = 1 //Positive Increment Position

once NIncPos2 = 1 //Neative Increment Position

once Optimize2 = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode2 = 1 //Switches between negative and positive increments

//once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize2 = Reps2 Then

WinCountA2 = 0 //Initialize current Win Count

StratAvgA2 = 0 //Initialize current Avg Strategy Profit

For i = 1 to Reps2 Do

If positionperf(i) > 0 Then

WinCountA2 = WinCountA2 + 1 //Increment Current WinCount

EndIf

StratAvgA2 = StratAvgA2 + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

//Graph StratAvgA*-1 as "StratAvgA"

//once BestA = 300

//GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA2 >= StratAvgB2 Then

StratAvgB2 = StratAvgA2 //Update Best Strategy Profit

BestA2 = ValueY

EndIf

//once BestB = 300

//GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA2 >= WinCountB2 Then

WinCountB2 = WinCountA2 //Update Best Win Count

BestB2 = ValueY

EndIf

If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then

Mode2 = 0

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

EndIf

If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then

If BestA2 = BestB2 Then

ValueY = BestA2

Else

If reps2 >= 10 Then

WeightedScore2 = 10

Else

WeightedScore2 = round((reps2/100)*100)

EndIf

ValueY = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos2 = 1

PIncPos2 = 1

ElsIf ValueY > MaxValue2 Then

ValueY = MaxValue2

ElsIf ValueY < MinValue2 Then

ValueY = MinValue2

EndIF

Optimize2 = 0

EndIf

graph valuex coloured(0,255,0,255) as "period"

graph valuey coloured(255,0,0,255) as "type"

// Heuristics Algorithm 2 End

endif

If EnableHeuristics = 0 then

ValueX = 45

ValueY = 3

endif

ma = average[ValueX,ValueY](close)

cnd1 = ma > ma[1]

cnd2 = ma < ma[1]

Good morning,

I find that the while loop is a duplicate with the if condition.

You tried without the loop while

IF high > renkoMax + boxSize THEN

WHILE high > renkoMax + boxSize

renkoMax = renkoMax + boxSize

renkoMin = renkoMin + boxSize

WEND

ELSIF low < renkoMin - boxSize THEN

WHILE low < renkoMin - boxSize

renkoMax = renkoMax - boxSize

renkoMin = renkoMin - boxSize

WEND

ENDIF

My browser e-find tells me there is 6 instances of ‘while’ on this page, but I can’t find two of them??

Nonetheless posted code has no ‘while’ in the code?

So I’ll have to ask … Fifi, who are you speaking to and which System are you referring to please?

The bard code

The code set out on page 13

The results are different with and without the while loop.

The code set out on page 13

It’s always best if we Quote a small / most relevant part of the post we are referring to (as I have above) else folks will assume (as I did) that we are referring to the post immediately above our post.

I referred to the code renko 1 m ML1 stploss

I find that the while loop is a duplicate with the if condition.

You tried without the loop

So below is Bard’s code (from page 13 Line 145 to Line 155) which is the same as you show in your post?

So what should Bard have done with the code?

IF high > renkoMax + boxSize THEN

WHILE high > renkoMax + boxSize

renkoMax = renkoMax + boxSize

renkoMin = renkoMin + boxSize

WEND

ELSIF low < renkoMin - boxSize THEN

WHILE low < renkoMin - boxSize

renkoMax = renkoMax - boxSize

renkoMin = renkoMin - boxSize

WEND

ENDIF