@GraHal try this 🙂 The HeuristicsCycleLimit parameter will determine how many ‘cycles’ each algorithm gets. If someone is up to it I also think we should look at introducing different performance metrics like Drawdown vs Profit Ratio to the existing WinRate (WinCount) and AvgProfit (StratAvg) metrics

HeuristicsCycleLimit = 2

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

If HeuristicsAlgo1 = 1 Then

//Heuristics Algorithm 1 Start

If onmarket[1] = 1 and onmarket = 0 Then

optimize = optimize + 1

EnDif

StartingValue = 200

ResetPeriod = 8 //Specify no of months after which to reset optimization

Increment = 20

MaxIncrement = 4 //Limit of no of increments either up or down

Reps = 3 //Number of trades to use for analysis

MaxValue = 270 //Maximum allowed value

MinValue = increment //Minimum allowed value

once monthinit = month

once yearinit = year

If (year = yearinit and month = (monthinit + ResetPeriod)) or (year = (yearinit + 1) and ((12 - monthinit) + month = ResetPeriod)) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

monthinit = month

yearinit = year

EndIf

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

//once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

//Graph StratAvgA*-1 as "StratAvgA"

//once BestA = 300

//GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

//once BestB = 300

//GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// Heuristics Algorithm 1 End

ElsIf HeuristicsAlgo2 = 1 Then

// Heuristics Algorithm 2 Start

If onmarket[1] = 1 and onmarket = 0 Then

optimize2 = optimize2 + 1

Endif

StartingValue2 = 200

ResetPeriod2 = 8 //Specify no of months after which to reset optimization

Increment2 = 20

MaxIncrement2 = 4 //Limit of no of increments either up or down

Reps2 = 3 //Number of trades to use for analysis

MaxValue2 = 270 //Maximum allowed value

MinValue2 = increment //Minimum allowed value

once monthinit2 = month

once yearinit2 = year

If (year = yearinit2 and month = (monthinit2 + ResetPeriod2)) or (year = (yearinit2 + 1) and ((12 - monthinit2) + month = ResetPeriod2)) Then

ValueY = StartingValue2

WinCountB2 = 0

StratAvgB2 = 0

BestA2 = 0

BestB2 = 0

monthinit2 = month

yearinit2 = year

EndIf

once ValueY = StartingValue2

once PIncPos2 = 1 //Positive Increment Position

once NIncPos2 = 1 //Neative Increment Position

once Optimize2 = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode2 = 1 //Switches between negative and positive increments

//once WinCountB2 = 3 //Initialize Best Win Count

//GRAPH WinCountB2 coloured (0,0,0) AS "WinCountB2"

//once StratAvgB2 = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB2 coloured (0,0,0) AS "StratAvgB2"

If Optimize2 = Reps2 Then

WinCountA2 = 0 //Initialize current Win Count

StratAvgA2 = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i2 = 1 to Reps2 Do

If positionperf(i) > 0 Then

WinCountA2 = WinCountA2 + 1 //Increment Current WinCount

EndIf

StratAvgA2 = StratAvgA2 + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1-2"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2-2"

//Graph StratAvgA2*-1 as "StratAvgA2"

//once BestA2 = 300

//GRAPH BestA2 coloured (0,0,0) AS "BestA2"

If StratAvgA2 >= StratAvgB2 Then

StratAvgB2 = StratAvgA2 //Update Best Strategy Profit

BestA2 = ValueY

EndIf

//once BestB2 = 300

//GRAPH BestB2 coloured (0,0,0) AS "BestB2"

If WinCountA2 >= WinCountB2 Then

WinCountB2 = WinCountA2 //Update Best Win Count

BestB2 = ValueY

EndIf

If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then

Mode = 0

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode = 1

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

EndIf

If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then

If BestA2 = BestB2 Then

ValueY = BestA

Else

If reps2 >= 10 Then

WeightedScore2 = 10

Else

WeightedScore2 = round((reps2/100)*100)

EndIf

ValueY = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos2 = 1

PIncPos2 = 1

ElsIf ValueY > MaxValue2 Then

ValueY = MaxValue2

ElsIf ValueY < MinValue2 Then

ValueY = MinValue2

EndIF

Optimize2 = 0

EndIf

// Heuristics Algorithm 2 End

EndIf

Here is the version of the algo outputting ‘ValueY

Referring to Line numbers of the version2 / ValueY posted with the link above, the ‘2’ is missed off …

Line 123 – increment

Line 157 & 160 – i

Line 180 & 188 – Mode

Line 201 – BestA

I’m not trying to be clever, I ran the ValueY version on its own as part of a trial of my ‘barindex idea’ and the syntax checker told me the above were not defined! 🙂

I’ll now have a go with the HeuristicsCycleLimit.

As an aside … anybody got any ideas / code to identify even & odd number barindex ?

identify even & odd number barindex

Good how ideas come when away from the screen!? 🙂

I’m not there yet, but I’m thinking around ?? …

If barindex mod 2 = 1 Then //odd barindex

AND

If barindex mod 2 = 0 Then //even barindex

Below is the HeuristicsCycleLimit code with the corrections mentioned 2 posts above … 2 was missing here and there in Algo 2.

Least I can do to save JuanJ some time for letting us in on his coding gems! 🙂

HeuristicsCycleLimit = 2

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

If HeuristicsAlgo1 = 1 Then

//Heuristics Algorithm 1 Start ////////////////////////////////////////////////////

If onmarket[1] = 1 and onmarket = 0 Then

optimize = optimize + 1

EnDif

StartingValue = 8 //200

ResetPeriod = 8 //Specify no of months after which to reset optimization

Increment = 2 //20

MaxIncrement = 24 //4 //Limit of no of increments either up or down

Reps = 3 //Number of trades to use for analysis

MaxValue = 48 //270 //Maximum allowed value

MinValue = increment //Minimum allowed value

once monthinit = month

once yearinit = year

If (year = yearinit and month = (monthinit + ResetPeriod)) or (year = (yearinit + 1) and ((12 - monthinit) + month = ResetPeriod)) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

monthinit = month

yearinit = year

EndIf

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

//once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

//Graph StratAvgA*-1 as "StratAvgA"

//once BestA = 300

//GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

//once BestB = 300

//GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// Heuristics Algorithm 1 End //////////////////////////////////////////////////////

ElsIf HeuristicsAlgo2 = 1 Then

// Heuristics Algorithm 2 Start ////////////////////////////////////////////////////

If onmarket[1] = 1 and onmarket = 0 Then

optimize2 = optimize2 + 1

Endif

StartingValue2 = 16 //200

ResetPeriod2 = 8 //Specify no of months after which to reset optimization

Increment2 = 2 //20

MaxIncrement2 = 24 //4 //Limit of no of increments either up or down

Reps2 = 3 //Number of trades to use for analysis

MaxValue2 = 48 //270 //Maximum allowed value

MinValue2 = increment2 //Minimum allowed value

once monthinit2 = month

once yearinit2 = year

If (year = yearinit2 and month = (monthinit2 + ResetPeriod2)) or (year = (yearinit2 + 1) and ((12 - monthinit2) + month = ResetPeriod2)) Then

ValueY = StartingValue2

WinCountB2 = 0

StratAvgB2 = 0

BestA2 = 0

BestB2 = 0

monthinit2 = month

yearinit2 = year

EndIf

once ValueY = StartingValue2

once PIncPos2 = 1 //Positive increment2 Position

once NIncPos2 = 1 //Neative increment2 Position

once Optimize2 = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode2 = 1 //Switches between negative and positive increments

//once WinCountB2 = 3 //Initialize Best Win Count

//GRAPH WinCountB2 coloured (0,0,0) AS "WinCountB2"

//once StratAvgB2 = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB2 coloured (0,0,0) AS "StratAvgB2"

If Optimize2 = Reps2 Then

WinCountA2 = 0 //Initialize current Win Count

StratAvgA2 = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i2 = 1 to Reps2 Do

If positionperf(i2) > 0 Then

WinCountA2 = WinCountA2 + 1 //Increment Current WinCount

EndIf

StratAvgA2 = StratAvgA2 + (((PositionPerf(i2)*countofposition[i2]*100000)*-1)*-1)

Next

StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1-2"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2-2"

//Graph StratAvgA2*-1 as "StratAvgA2"

//once BestA2 = 300

//GRAPH BestA2 coloured (0,0,0) AS "BestA2"

If StratAvgA2 >= StratAvgB2 Then

StratAvgB2 = StratAvgA2 //Update Best Strategy Profit

BestA2 = ValueY

EndIf

//once BestB2 = 300

//GRAPH BestB2 coloured (0,0,0) AS "BestB2"

If WinCountA2 >= WinCountB2 Then

WinCountB2 = WinCountA2 //Update Best Win Count

BestB2 = ValueY

EndIf

If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then

Mode2 = 0

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

EndIf

If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then

If BestA2 = BestB2 Then

ValueY = BestA2

Else

If reps2 >= 10 Then

WeightedScore2 = 10

Else

WeightedScore2 = round((reps2/100)*100)

EndIf

ValueY = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos2 = 1

PIncPos2 = 1

ElsIf ValueY > MaxValue2 Then

ValueY = MaxValue2

ElsIf ValueY < MinValue2 Then

ValueY = MinValue2

EndIF

Optimize2 = 0

EndIf

// Heuristics Algorithm 2 End ////////////////////////////////////////////////////////

JuanJ you sure below code works please?

I can’t get any results using below … despite trying what I thought was logical re changes etc! 🙂

Maybe you try it if you get chance please?

Or anybody else get below to work (using the full code above)?

HeuristicsCycleLimit = 2

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

If HeuristicsAlgo1 = 1 Then

Ah! I forgot to initialize the variables:

HeuristicsCycleLimit = 2

once HeuristicsCycle = 0

once HeuristicsAlgo1 = 1

once HeuristicsAlgo2 = 0

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

I should be able to GRAPH ValueX and ValueY as normal?

If yes then mine isn’t working with the 2 Algos as ValueX and ValueY GRAPH as constant starting values.

I’m going to start again with one Algo! 🙂

I give up! I can’t get it to work, it doesnt give bad results … it doesn’t even even start.

I’m sure it is something simple, although I’m sure I’ve tried everything simple!? 🙂

I thought I was getting 1 x Algo to work. but I realise now that I was optimising the starting value and the starting value continued to be used for all trades!

Seems to have gone quiet after the first few flurries of excitement?

Anybody else got it to work?

@Juanj I have changed your values to my respective values etc, but how are you defining … Best Avg Strategy Profit?

I feel somewhat stupid but I don’t have a clue what this heuristic algo code does ! Maybe I’m not the only one…can anybody explain in a few sentences how does it work?

Thanks

can anybody explain in a few sentences how does it work

It optimises 1 x variable value up / down 1 x pre-set increment depending on the performance of the previous 3 (pre-set number) trades.

I am reading between the lines of the code (as I can’t follow it all) but what I’m not clear about is … how does the heuristics decide that the one or all of the past 3 trades were not just bad trades anyway?? As we all know we can get a bad run for while.

I guess the heuristics must be comparing against an average profit … which is why I asked JuanJ how Best Avg Strategy Profit is defined as this must be critical.

But at this stage I’d be happy if I could see the GRAPH of ValueX moving from it’s starting value! 🙂

@GraHal Please share the ITF file of the strategy you wish to implement the algorithm to and I will have a look to see where the problem is.

Then to further elaborate on GraHal’s explanation:

The algorithm also keeps track of the following:

- Best average performance (Profit) measured over all the previous evaluation periods (StratAvgB)

- Best win rate (Win %) measured over a all the previous evaluation periods (WinCountB)

It then measures and saves the same metrics but only for the last evaluation period (StratAvgA and WinCountA) and compares them to the above.

It then starts by systematically incrementing the target variables both up and down to see what appears to improve performance most

There are also some other calculations going on but that is mostly to achieve the above.

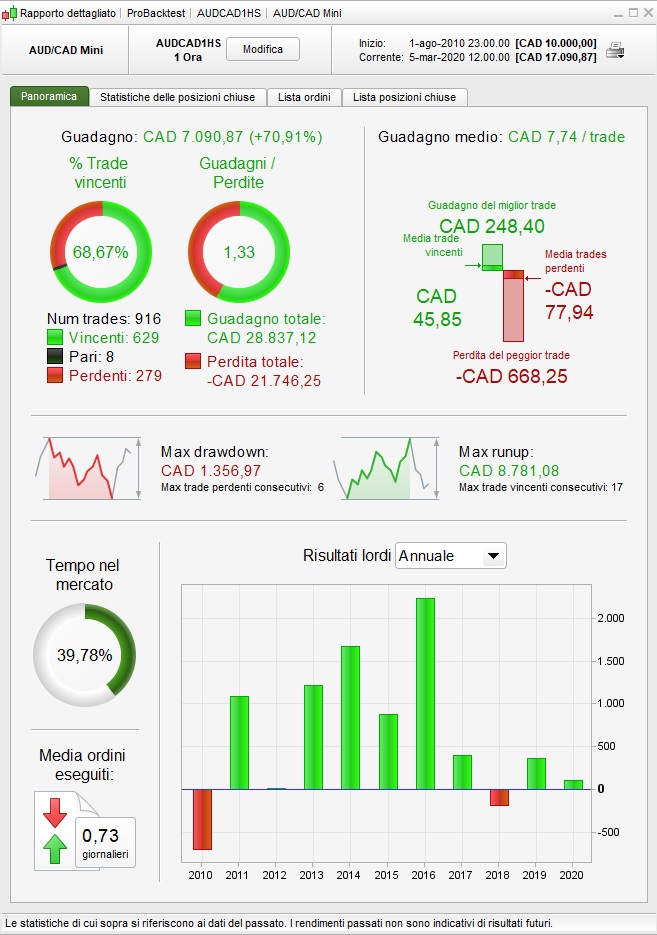

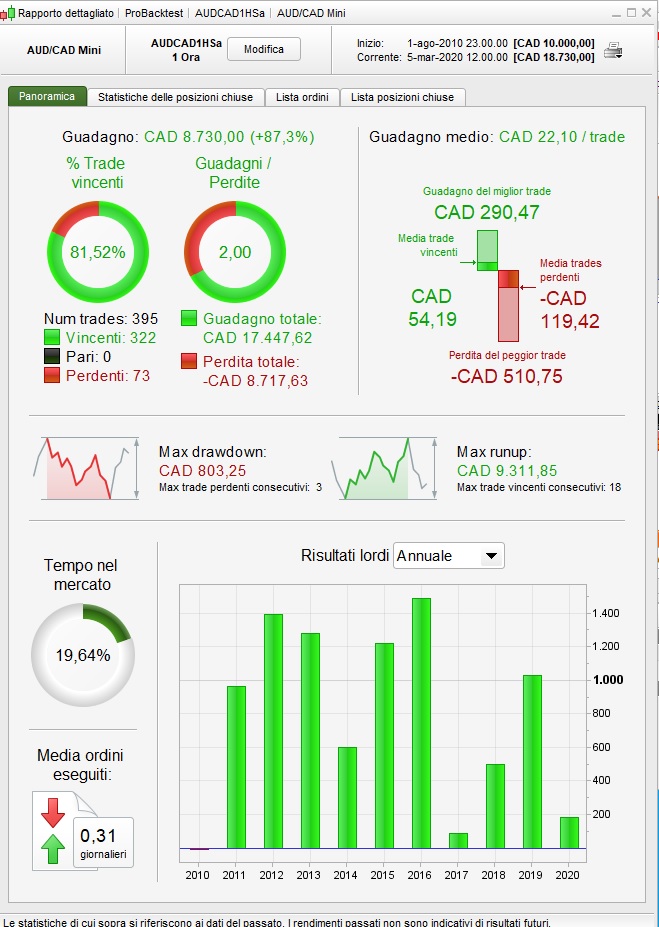

I just added the machine learning into a system, here’s the results (before and after).

Very impressive, and also the robustness test went up in total average!

I will have a look to see where the problem is.

Thank you, I may take you up on the offer! 🙂

I am learning stuff by me keep asking myself … “why the eff isn’t it working?” and as your code is applicable to any strategy it is time well sweated over! But it sure don’t feel like it yet! 🙂

I got it going on another strategy.

Should your heuristic code work on strategies that switch position from Long to Short with no bars not onmarket ?

Should your heuristic code work on strategies that switch position from Long to Short with no bars not onmarket ?

Yip that is the problem. Solution;

Replace this:

If onmarket[1] = 1 and onmarket = 0 Then

optimize = optimize + 1

EndIf

With This:

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize = optimize + 1

EndIf

Paul

PaulParticipant

Master

hi juanj

one algo works, but 2 fails somewhere.

I created a basic strategy on a second timeframe for testing. Can you see what is wrong please below?

defparam cumulateorders = false

defparam preloadbars = 10000

defparam flatbefore = 080000

defparam flatafter = 220000

period1=7

period2=14

HeuristicsCycleLimit = 2

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

If HeuristicsAlgo1 = 1 Then

//Heuristics Algorithm 1 Start

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize = optimize + 1

EndIf

StartingValue = period1

ResetPeriod = 3 //Specify no of months after which to reset optimization

Increment = 1

MaxIncrement = 7 //Limit of no of increments either up or down

Reps = 3 //Number of trades to use for analysis

MinValue = 2 //Minimum allowed value

MaxValue = 14 //Maximum allowed value

If monthinit = 1 or monthinit = 3 or monthinit = 5 or monthinit = 7 or monthinit = 8 or monthinit = 10 or monthinit = 12 Then

MonthDays = 31

ElsIf monthinit = 4 or monthinit = 6 or monthinit = 9 or monthinit = 11 Then

MonthDays = 30

ElsIf monthinit = 2 Then

If (yearinit/4 = round(yearinit/4)) or (yearinit/400 = round(yearinit/400)) Then //haha not sure how exactly to do this

MonthDays = 29 //leap year

Else

MonthDays = 28

EndIf

EndIf

If (month = monthinit and day = dayinit + ResetPeriod) or (month = monthinit + 1 and (day + (MonthDays - dayinit)) >= ResetPeriod) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

dayinit = day

monthinit = month

yearinit = year

EndIf

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

//once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

//Graph StratAvgA*-1 as "StratAvgA"

//once BestA = 300

//GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

//once BestB = 300

//GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// Heuristics Algorithm 1 End

ElsIf HeuristicsAlgo2 = 1 Then

// Heuristics Algorithm 2 Start

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize2 = optimize2 + 1

EndIf

StartingValue2 = period2

ResetPeriod2 = 3 //Specify no of months after which to reset optimization

Increment2 = 1

MaxIncrement2 = 7 //Limit of no of increments either up or down

Reps2 = 3 //Number of trades to use for analysis

MinValue2 = 15 //Minimum allowed value

MaxValue2 = 28 //Maximum allowed value

If monthinit2 = 1 or monthinit2 = 3 or monthinit2 = 5 or monthinit2 = 7 or monthinit2 = 8 or monthinit2 = 10 or monthinit2 = 12 Then

MonthDays2 = 31

ElsIf monthinit2 = 4 or monthinit2 = 6 or monthinit2 = 9 or monthinit2 = 11 Then

MonthDays2 = 30

ElsIf monthinit2 = 2 Then

If (yearinit2/4 = round(yearinit2/4)) or (yearinit2/400 = round(yearinit2/400)) Then //haha not sure how exactly to do this

MonthDays2 = 29 //leap year

Else

MonthDays2 = 28

EndIf

EndIf

If (month = monthinit2 and day = dayinit2 + ResetPeriod2) or (month = monthinit2 + 1 and (day + (MonthDays2 - dayinit2)) >= ResetPeriod2) Then

ValueY = StartingValue2

WinCountB2 = 0

StratAvgB2 = 0

BestA2 = 0

BestB2 = 0

dayinit2 = day

monthinit2 = month

yearinit2 = year

EndIf

once ValueY = StartingValue2

once PIncPos2 = 1 //Positive Increment Position

once NIncPos2 = 1 //Neative Increment Position

once Optimize2 = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode2 = 1 //Switches between negative and positive increments

//once WinCountB2 = 3 //Initialize Best Win Count

//GRAPH WinCountB2 coloured (0,0,0) AS "WinCountB2"

//once StratAvgB2 = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB2 coloured (0,0,0) AS "StratAvgB2"

If Optimize2 = Reps2 Then

WinCountA2 = 0 //Initialize current Win Count

StratAvgA2 = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i2 = 1 to Reps2 Do

If positionperf(i) > 0 Then

WinCountA2 = WinCountA2 + 1 //Increment Current WinCount

EndIf

StratAvgA2 = StratAvgA2 + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1-2"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2-2"

//Graph StratAvgA2*-1 as "StratAvgA2"

//once BestA2 = 300

//GRAPH BestA2 coloured (0,0,0) AS "BestA2"

If StratAvgA2 >= StratAvgB2 Then

StratAvgB2 = StratAvgA2 //Update Best Strategy Profit

BestA2 = ValueY

EndIf

//once BestB2 = 300

//GRAPH BestB2 coloured (0,0,0) AS "BestB2"

If WinCountA2 >= WinCountB2 Then

WinCountB2 = WinCountA2 //Update Best Win Count

BestB2 = ValueY

EndIf

If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then

Mode = 0

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode = 1

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

EndIf

If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then

If BestA2 = BestB2 Then

ValueY = BestA

Else

If reps2 >= 10 Then

WeightedScore2 = 10

Else

WeightedScore2 = round((reps2/100)*100)

EndIf

ValueY = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos2 = 1

PIncPos2 = 1

ElsIf ValueY > MaxValue2 Then

ValueY = MaxValue2

ElsIf ValueY < MinValue2 Then

ValueY = MinValue2

EndIF

Optimize2 = 0

EndIf

// Heuristics Algorithm 2 End

EndIf

c1=average[valuex](close)

c2=average[valuey](close)

//

condbuy =c1 crosses over c2 and rsi[14](close)<70

condsell=c1 crosses under c2 and rsi[14](close)>30

//

if condbuy then

buy at market

endif

if condsell then

sellshort at market

endif

pp=positionperf(0)*100

if pp<-0.125 then

sell at market

exitshort at market

endif

set stop %loss 0.5 // exit sooner on performance criteria above

set target %profit 0.25

graph valuex coloured(121,141,35,255) as "fastperiod1"

graph valuey coloured(255,0,0,255) as "slowperiod"