Expert Services

No recent search

Modular Algo System V2.0 inkl. DAX Intraday 1m System

- Forums

- ProRealTime Forum Deutsch

- ProOrder: Automatischer Handel & Backtesting

- Modular Algo System V2.0 inkl. DAX Intraday 1m System

-

AuthorPosts

-

Anbei mein zwischenzeitlich stark erweiterter modularer Algorithmus-Code

inkl. eines “Starter-Paketes zum Experimentieren.

Viel Spaß!

Kommentare sind natürlich willkommen!//*************************************************************************//

//Modular Algorithm Library V2.0 //

//*************************************************************************//

//Modules:

//Market-Data-Definition+Parameter

///Monthly/Weekly/Daily-Modifiers, Xetra-HLC-Correction, Strategy-Stop-Code mit Money-Management

//Moving-Average-Clustering-Filter, Robustness-Test, Stop-Loss/Trailing-Routines Long/Short/Risk

//Long/Short-Support2/Resistance2-Break-Filter, HexenSabbat-Filter

//Trading Code//*************************************************************************//

//Parameter //

//*************************************************************************//

DEFPARAM PreLoadBars = 10000

DEFPARAM CumulateOrders = false

ONCE TradeON = 0

ONCE Tradeday = 0ONCE IndexFaktoring = 0 // 1=ON 0=OFF Faktoring des Indexkurses

ONCE ClusterSave = 2 // 0=OFF 1=small 2=large 3=all MovingAverage-Clustering-Filter

ONCE startingsize = 0.25 // starting position size

ONCE maxsize = 2 // maximal positionsize

ONCE ForbiddenLSFlag = 0 // 0=OFF 1=ON 2=Reverse 3=Strict 4=StrictReverse S1/S2/Short-R1/R2/Long-Filter

ONCE RobustnessTest = 0 // 0=OFF 1=ON Robustness-Test

ONCE SSC = 0 // 0=OFF 1=ON 2=Alternative Strategy-Stop-Code

ONCE Reinvest = 1 // 0=OFF 1=ON Gewinne reinvestieren

ONCE ReinvestValue = 0.5 //Reinvestitionsanteil

ONCE StartingCapital = 20000 // Startkapital

ONCE Modifiers = 1 // 0=OFF 1=ON Modifikatoren auf PositionSize

ONCE DaySLFlag = 1 // 0=OFF 1=ON Intraday Short/Long-Reversal-Flag (Modifier)

ONCE MarketFlag = 1 // 1=DAX 2=DJI Marktauswahl

ONCE HexSabFilter = 1 // 0=OFF 1=ON HexenSabbatFilter

ONCE Overnight = 1 // 0=NO 1=YES Overnight Holding allowed//*************************************************************************//

//Market Data //

//*************************************************************************//

ONCE Opening = 080000 // Eröffnungszeit DAX

ONCE Closing = 220000 // Schlusszeit DAX

ONCE TF = 1 // TimeFrame in Minuten DAX

ONCE SpreadGeb = 4 // Spread+Gebühren DAX

ONCE Indexfaktor = 13000

ONCE Faktor1 = Close / Indexfaktor

ONCE FaktorTS = 1 // Trailing-Stop-MultiplikatorIF MarketFlag = 1 THEN

Opening = 080000 // Eröffnungszeit DAX

Closing = 220000 // Schlusszeit DAX

TF = 1 // TimeFrame in Minuten DAX

SpreadGeb = 4 // Spread+Gebühren DAX

ONCE FaktorTS = 1 // Trailing-Stop-Multiplikator

IF IndexFaktoring = 1 THEN

Indexfaktor = 14000

ELSIF Indexfaktoring = 0 THEN

Indexfaktor = Close

ENDIF

Faktor1 = Close / Indexfaktor

ENDIFIF MarketFlag = 2 THEN

Opening = 080000 // Eröffnungszeit DJI

Closing = 220000 // Schlusszeit DJI

TF = 1 // TimeFrame in Minuten DJI

SpreadGeb = 4 // Spread+Gebühren DJI

IF IndexFaktoring = 1 THEN

Indexfaktor = 30000

ELSIF Indexfaktoring = 0 THEN

Indexfaktor = Close

ENDIF

Faktor1 = Close / Indexfaktor

ONCE FaktorTS = 2.5 // Trailing-Stop-Multiplikator

ENDIFIF OpenDayOfWeek > 0 AND OpenDayOfWeek < 6 AND NOT (Month = 10 AND Day = 3) AND NOT (Month = 5 AND Day = 1) AND NOT (Month = 12 AND Day = 24) AND NOT (MONTH = 12 AND Day = 25) AND NOT (MONTH = 12 AND Day = 26) AND NOT (MONTH = 12 AND Day = 30) AND NOT (MONTH = 12 AND Day = 26) THEN

Tradeday = 1

ELSE

Tradeday = 0

ENDIF//Flat Failsave

If ONMARKET AND Overnight = 0 AND (Time < Opening OR Time > Closing) THEN

SELL AT Market

EXITSHORT AT Market

ENDIF//*************************************************************************//

//Algorithm Robustness-Test //

//*************************************************************************//

StartDate = 20000101 // Parameter

Qty = 5 // Parameter

Rndom = 3 // Parameter

once j = 0

once flag = 1IF RobustnessTest = 1 THEN

if flag = 1 then

j = j + 1

if j > qty then

flag = -1

j = j - 1

endif

endif

if flag = -1 then

j = j - 1

if j = 0 then

j = j + rndom

flag = 1

endif

endifif opendate >= startdate AND (barindex mod qty = 0 or barindex mod qty = j) then

tradeon = 1

ELSIF opendate >= startdate AND NOT (barindex mod qty = 0 or barindex mod qty = j) then

tradeon = 0

endif

ENDIF//*************************************************************************//

//Strategy-Stop-Code, Money Management/ReInvest //

//*************************************************************************//

barsbeforenextcheck = 30 // number of bars between performance checks

drawdownquitting = 1 // drawdown quitting on or off (on=1 off=0)

winratequit = 50 // minimum win rate in % allowed before quitting (0 = off)

tradesbeforewrquit = 50 // number of trades required before a win rate stop of strategy is allowed to happen

increase = 1 // position size increasing on or off (on=1 off=0)

decrease = 1 // position size decreasing on or off (on=1 off=0)

capital = StartingCapital // starting capital

minpossize = 1 // minimum position size allowed

gaintoinc = 5 // % profit rise needed before an increase in position size is made

losstodec = 5 // % loss needed before a decrease in position size is made

maxdrawdown = 50 // maximum % draw down allowed from highest ever equity before stopping strategy

maxcapitaldrop = 50 // maximum % starting capital lost before stopping strategy

ONCE highestprofit = 0

ONCE count = 0

ONCE win = 0

ONCE winrate = 0

ONCE MMpositionsize = 1

ONCE psperc = (MMpositionsize*startingsize) / (capital/100)

ONCE equity = StartingCapital

ONCE Profit1 = 0IF SSC = 1 THEN

if strategyprofit < strategyprofit[1] then

Profit1 = highestprofit - (strategyprofit[1] - strategyprofit)

highestprofit = highestprofit - Profit1

Profit1 = 0

ELSIF strategyprofit > strategyprofit[1] then

Profit1 = (strategyprofit - strategyprofit[1])*0.7

highestprofit = highestprofit + Profit1

Profit1 = 0

if count < tradesbeforewrquit OR winrate > winratequit/100 then

count = count + 1

if strategyprofit > strategyprofit[1] then

win = win + 1

endif

ENDIF

winrate = win/count

ENDIF

if count >= tradesbeforewrquit AND winrate < winratequit/100 then

quit

endif

if barindex mod barsbeforenextcheck = 0 AND drawdownquitting AND highestprofit <> 0 then

if (capital + strategyprofit) <= (capital + highestprofit) - ((capital + highestprofit)*(maxdrawdown/100)) then

quit

endif

endif

if count >= tradesbeforewrquit AND highestprofit = 0 then

if (capital + strategyprofit) <= capital - (capital * (maxcapitaldrop/100)) then

quit

endif

ENDIF

IF SSC = 2 THEN

MMpositionsize = max(((equity)/startingcapital),minpossize)

ENDIF

ENDIF//*******************************************************************************************//

//Position Size,Monthly,Weekly,Daily,Intra,Trend,Reversal Modifiers (optional) //

//*******************************************************************************************//

//Berechnung am Schluss löschen ( auf 1 setzen) für Löschen des Modifikators

ONCE PSizeL = startingsize

ONCE PSizeS = startingsize

ONCE MonthSizeL = 0

ONCE MonthSizeS = 0

ONCE WeekSizeL = 0

ONCE WeekSizeS = 0

ONCE DaySizeL = 0

ONCE DaySizeS = 0

ONCE Monatsanfang = 0

ONCE Monatsende = 0

ONCE IntraSizeL = 0

ONCE IntraSizeS = 0

ONCE GapCloseup = 0

ONCE GapClosedown = 0

ONCE VBaisse = 0

ONCE VHausse = 0

ONCE SentimentSizeL = 0

ONCE SentimentSizeS = 0

ONCE MidMonthSizeL = 0IF Modifiers = 1 THEN

IF MarketFlag = 1 THEN

IF XetraClose > XetraCloseOld THEN

VHausse = VHausse +1

VBaisse = 0

ELSIF XetraClose < XetraCloseOld THEN

VHausse = 0

VBaisse = VBaisse +1

ENDIF

IF VHausse > 5 THEN

SentimentSizeS = 0.5

ELSIF VBaisse > 5 THEN

SentimentSizeL = 0.5

ENDIF

IF Day > 8 AND Day < 12 THEN

MidMonthSizeL = 0.5

ELSE

MidMonthSizeL = 0

ENDIF

IF CurrentMonth = 1 THEN

MonthSizeS = 0.25

MonthSizeL = 0

ELSIF CurrentMonth >= 2 AND CurrentMonth >= 3 THEN

MonthSizeS = 0

MonthSizeL = 0.25

ELSIF CurrentMonth = 4 THEN

MonthSizeS = 0

PMonthSizeL = 0.5

ELSIF CurrentMonth = 5 THEN

MonthSizeS = 0

MonthSizeL = 0

ELSIF CurrentMonth = 6 THEN

MonthSizeS = 0.25

MonthSizeL = 0

ELSIF CurrentMonth = 7 THEN

MonthSizeS = 0

MonthSizeL = 0.25

ELSIF CurrentMonth >= 8 AND CurrentMonth <= 9 THEN

MonthSizeS = 0.25

MonthSizeL = 0

ELSIF CurrentMonth >= 10 AND CurrentMonth <= 12 THEN

MonthSizeS = 0

MonthSizeL = 0.5

ENDIF

IF Time = Opening THEN

If Day >= 01 AND Day <= 08 THEN

Monatsanfang = 1

ELSIF Day >= 25 AND Day <= 31 THEN

Monatsende = 1

ENDIF

ENDIF

IF Monatsanfang = 1 THEN

IF CurrentMonth >= 1 AND CurrentMonth <= 7 THEN

WeekSizeL = 0.25

WeekSizeS = 0

ELSIF CurrentMonth >= 8 AND CurrentMonth <= 9 THEN

WeeksizeL = 0

WeekSizeS = 0.25

ELSIF CurrentMonth = 10 THEN

WeeksizeL = 0

WeekSizeS = 0

ELSIF CurrentMonth >= 11 AND CurrentMonth <= 12 THEN

WeekSizeL = 0.25

WeekSizeS = 0

ENDIF

ENDIF

IF Monatsende = 1 THEN

IF CurrentMonth = 1 THEN

WeekSizeL = 0.25

WeekSizeS = 0

ELSIF CurrentMonth = 2 THEN

WeekSizeL = 0

WeekSizeS = 0

ELSIF CurrentMonth >= 3 AND CurrentMonth <= 6 THEN

WeeksizeL = 0.25

WeekSizeS = 0

ELSIF CurrentMonth = 7 THEN

WeekSizeL = 0

WeekSizeS = 0

ELSIF CurrentMonth >= 8 AND CurrentMonth <= 9 THEN

WeekSizeL = 0

WeekSizeS = 0.5

ELSIF CurrentMonth >= 10 AND CurrentMonth <= 12 THEN

WeeksizeL = 0.5

WeekSizeS = 0

ENDIF

ENDIF

IF OpenDayofWeek = 1 THEN

DaySizeL = 0.25

DaySizeS = 0

ELSIF OpenDayofWeek = 5 Then

DaySizeL = 0

DaySizeS = 0.25

ELSIF OpenDayofWeek <1 OR (OpenDayofWeek >= 2 AND OpenDayOfWeek <= 4) OR OpenDayofWeek = 6 THEN

DaySizeL = 0

DaySizeS = 0

ENDIF

IF Close < DLow(1) AND DaySLFlag = 1 THEN

IntraSizeL = 0.25

IntraSizeS = 0

ELSIF Close > DHigh(1) AND DaySLFlag = 1 THEN

IntraSizeL = 0

IntraSizeS = 0.25

ELSIF DaySLFlag = 0 THEN

IntraSizeL = 0

IntraSizeS = 0

ENDIF

IF Time >= Opening AND Time <= Closing THEN

IF Close > ResR2 THEN

IDReversalL = 0.25

ELSIF Close > ResR3 THEN

IDReversalL = 0.5

ELSIF Close < SupS2 AND Close > SupS3 THEN

IDReversalS = 0.25

ELSIF Close < SupS3 THEN

IDReversalS = 0.5

ELSIF Close < ResR2 AND Close > SupS2 THEN

IDReversalL = 0

IDReversalS = 0

ENDIF

ENDIF

IF Time = Closing THEN

TrendUp = 0

TrendDown = 0

ENDIF

IF Time = Opening THEN

IF DHigh(1) > DHigh(2) AND DLow(1) > DLow(2) THEN

TrendUp = 0.25

TrendDown = 0

ELSIF DHigh(1) < DHigh(2) AND DLow(1) < DLow(2) THEN

TrendUp = 0

TrendDown = 0.25

ENDIF

ENDIF

IF Time = Opening AND XetraCloseOld > XetraClose AND Close < XetraClose-10 THEN

GapCloseup = 0.5

GapClosedown = 0

ELSIF Time = Opening AND XetraCloseOld < XetraClose AND Close > XetraClose+10 THEN

GapCloseup = 0

GapClosedown = 0.5

ENDIF

ELSIF MarketFlag = 2 THEN

IF CurrentMonth = 1 THEN

MonthSizeS = 0.25

MonthSizeL = 0

ELSIF CurrentMonth = 3 OR CurrentMonth = 4 OR CurrentMonth = 5 THEN

MonthSizeS = 0

PMonthSizeL = 0.25

ELSIF CurrentMonth = 6 THEN

MonthSizeS = 0.25

MonthSizeL = 0

ELSIF CurrentMonth = 7 OR CurrentMonth = 8 THEN

MonthSizeS = 0

MonthSizeL = 0

ELSIF CurrentMonth = 9 THEN

MonthSizeS = 0.25

MonthSizeL = 0

ELSIF CurrentMonth >= 10 AND CurrentMonth <= 12 THEN

MonthSizeS = 0

MonthSizeL = 0.5

ENDIF

ENDIF

ENDIF//Einzelne Komponenten können nach belieben hier gelöscht werden, um die Modifikationen an eigene Vorstellungen anzupassen

IF Reinvest = 1 THEN

PositionSizeLong = (PSizeL*(PSizeL+TrendUp+IDReversalL+IntraSizeL+DaySizeL+WeekSizeL+MonthSizeL+GapCloseup+SentimentSizeL+MidMonthSizeL)*Min(maxsize,(1+(strategyprofit/startingcapital)*Reinvestvalue))*MMpositionsize)

PositionSizeShort = (PSizeS*(PSizeS+TrendDown+IDReversalS+IntraSizeS+DaySizeS+WeekSizeL+MonthSizeS+GapClosedown+SentimentSizeS)*Min(maxsize,(1+(strategyprofit/startingcapital)*Reinvestvalue))*MMpositionsize)

ELSIF Reinvest = 0 THEN

PositionSizeLong = Min(maxsize,(PSizeL*(PSizeL+TrendUp+IDReversalL+IntraSizeL+DaySizeL+WeekSizeL+MonthSizeL+GapCloseup+SentimentSizeL+MidMonthSizeL))*MMpositionsize)

PositionSizeShort = Min(maxsize,(PSizeS*(PSizeS+TrendDown+IDReversalS+IntraSizeS+DaySizeS+WeekSizeL+MonthSizeS+GapClosedown+SentimentSizeS))*MMpositionsize)

ELSIF Modifiers = 0 THEN

PositionSizeLong = Min(maxsize,(PSizeL*MMpositionsize))

PositionSizeShort = Min(maxsize,(PSizeS*MMpositionsize))

ENDIF//*************************************************************************//

//Xetra-Korrektur High Low Close, Pivot, Resistance, Support , Flags //

//*************************************************************************//

ONCE DayClose = 14536 // last numbers before start of algorithm

ONCE DayHigh = 14586

ONCE DayLow = 14389

ONCE XetraClose = 14523

ONCE XetraCloseOld = 14423ONCE ReachedXetra = 1

ONCE ReachedDayClose = 1

ONCE Reachedboth = 1

ONCE ClosetryCount = 0IF Time = 060000 THEN

ReachedXetra = 0

ReachedDayClose = 0

Reachedboth = 0

ClosetryCount = 0

ENDIFIF Time >= 070000 AND Time <= 113000 THEN

IF Close >= XetraClose-15 AND Close <= XetraClose+12 THEN

ReachedXetra = 1

ENDIF

IF Close >= DayClose-10 AND Close <= DayClose+12 THEN

ReachedDayClose = 1

ENDIF

IF (ReachedXetra = 1) AND (ReachedDayClose = 1) THEN

Reachedboth = 1

ENDIF

ENDIFOverboth = (Close-5 > XetraClose AND XetraClose > DayClose) OR (Close-5 > DayClose AND DayClose > XetraClose)

Underboth = (Close+5 < XetraClose AND XetraClose < DayClose) OR (Close+5 < DayClose AND DayClose < XetraClose)

AmplitudeMin = 10

hi = Highest[15](close[1])

lo = Lowest[15](close[1])IF Time = 174400 AND OPENDAYOFWEEK <6 AND OPENDAYOFWEEK >0 AND Tradeday THEN

IF (Close < XetraClose AND (Highest[585] < XetraClose-5)) OR ((Close > XetraClose) AND Lowest[585] > XetraClose+5) THEN

XetraCloseOld = XetraClose

ENDIF

ENDIF

IF TIME = 174500 AND OPENDAYOFWEEK <6 AND OPENDAYOFWEEK >0 AND Tradeday THEN

XetraClose = Close[0]

ENDIFIF Time = 220000 AND OPENDAYOFWEEK <6 AND OPENDAYOFWEEK >0 AND Tradeday then

DayClose = Close[0]

DayHigh = Highest[(840/TF)](close[0])

DayLow = Lowest[(840/TF)](close[0])

ENDIFif Time = 220000 AND OPENDAYOFWEEK <6 AND OPENDAYOFWEEK >0 AND Tradeday then

Pivot = (DayHigh + DayLow + DayClose) / 3

ResR1 = Pivot + (Pivot - DayLow)

ResR2 = Pivot + (Dayhigh - Daylow)

ResR3 = Dayhigh + (2 * (Pivot - Daylow))

SupS1 = Pivot - (Dayhigh - Pivot)

SupS2 = Pivot - (Dayhigh - Daylow)

SupS3 = Daylow - (2 * (Dayhigh - Pivot))

ENDIF//*************************************************************************//

//Moving-Average-Clustering-FilterCode (optional) //

//*************************************************************************//

xx = 15*pipsize //20-pip range

xy = 15*pipsize //20-pip range

ma4500 = Average[4500,0](close)

ma2500 = Average[2500,0](close)

ma1000 = average[1000,0](close)

ma50 = average[50,0](close)

ma100 = average[100,0](close)

ma200 = average[200,0](close)

MaxMA = max(ma1000,max(ma2500,max(ma100,ma200)))

MinMA = min(ma1000,min(ma2500,min(ma100,ma200)))IF ClusterSave = 1 OR ClusterSave = 3 THEN

IF (MaxMA - MinMA) <= xx THEN

Tradeon = 0

ELSIF (MaxMA - MinMA) > xx THEN

IF RobustnessTest = 0 THEN

Tradeon = 1

ELSIF opendate >= startdate AND NOT (barindex mod qty = 0 or barindex mod qty = j) THEN

Tradeon = 0

ENDIF

ENDIF

ENDIF

IF ClusterSave >= 2 THEN

IF (max(ma4500,ma2500)-min(ma4500,ma2500) < xy) OR (max(ma4500,ma1000)-min(ma4500,ma1000) < xy) OR (max(ma2500,ma1000)-min(ma2500,ma1000) < xy) THEN

Tradeon = 0

ENDIF

ENDIF//*************************************************************************//

//R2-Long/S2-Short Filter (optional) //

//*************************************************************************//

ONCE ForbiddenLong = 0

ONCE ForbiddenShort = 0IF ForbiddenLSFlag = 1 THEN

ForbiddenLong = Close < SupS2

ForbiddenShort = Close > ResR2

ELSIF ForbiddenLSFlag = 2 THEN

ForbiddenLong = Close > ResR2

ForbiddenShort = Close < SupS2

ELSIF ForbiddenLSFlag = 3 THEN

ForbiddenLong = Close < SupS1

ForbiddenShort = Close > ResR1

ELSIF ForbiddenLSFlag = 4 THEN

ForbiddenLong = Close > ResR1

ForbiddenShort = Close < SupS1

ELSIF ForbiddenLSFlag = 0 THEN

ForbiddenLong = 0

ForbiddenShort = 0

ENDIF//*************************************************************************//

//MA20/MA50- MA30/50- MA100/200- Cross-Flag //

//*************************************************************************//

MA20 = Average[20](close)

MA30 = Average[30](close)

MA50 = Average[50](close)

MA100 = Average[100](close)

MA200 = Average[200](close)

MA20over = (MA20 crosses over MA50)

MA20under = (MA20 crosses under MA50)

MA30over = (MA30 crosses over MA50)

MA30under = (MA30 crosses under MA50)

MA100over = (MA100 > MA200)

MA100under = (MA100 < MA200)//*************************************************************************//

//HexenSabbat-Filter //

//*************************************************************************//

IF HexSabFilter = 1 THEN

IF (CurrentMonth = 3 OR CurrentMonth = 6 OR CurrentMonth = 9 OR CurrentMonth = 12) AND OpenDayofWeek = 5 AND Day >= 15 AND Day <= 21 THEN

TradeDay = 0

ELSIF RobustnessTest = 0 AND Opening AND Tradeday THEN

TradeOn = 1

ELSE

TradeON = 0

ENDIF

ELSIF RobustnessTest = 0 AND Opening AND Tradeday THEN

TradeON = 1

ELSE

TradeON = 0

ENDIF//*************************************************************************//

//Daytrend-Flag //

//*************************************************************************//

ONCE TrendFlag = 0IF Time = Opening THEN

IF DHigh(1) > DHigh(2) AND DLow(1) > DLow(2) THEN

TrendFlag = 1

ELSIF DHigh(1) < DHigh(2) AND DLow(1) < DLow(2) THEN

TrendFlag = -1

ELSIF NOT (DHigh(1) > DHigh(2) AND DLow(1) > DLow(2)) AND NOT (DHigh(1) < DHigh(2) AND DLow(1) < DLow(2)) THEN

TrendFlag = 0

ENDIF

ENDIF

TrendUp = (TrendFlag = 1)

TrendDown = (TrendFlag = -1)//*************************************************************************//

//trailing stop function Risk, Long, Short //

//*************************************************************************//

//wenn gewünscht die Parameter ändern oder die SET STOP-CODES löschen

// TrailingFlag = 0 Special (Code im Modul)

// TrailingFlag = 1 Normal

// TrailingFlag = 2 Risk

trailingstartL = 35*FaktorTS*Faktor1 //LONG trailing will start @trailinstart points profit, TrailingFlag = 0

trailingstartS = 35*FaktorTS*Faktor1 //SHORT trailing will start @trailinstart points profit, TrailingFlag = 0

trailingL = 13*FaktorTS*Faktor1 //trailing to move the "stoploss"

trailingS= 13*FaktorTS*Faktor1 //trailing to move the "stoploss"

trailingR= 11*FaktorTS*Faktor1 //trailing start+to move the "stoploss" for risky positions, TrailingFlag = 2

SaveDistanceL = 16*Faktor1 //Minimum Stop-Abstand 10 lt IG

SaveDistanceS = 16*Faktor1 //Minimum Stop-Abstand 10 lt IG

SaveDistanceR = 16*Faktor1 //Minimum Stop-Abstand 10 lt IG

MinimumPlus = SpreadGeb //Anzahl Pips zum Breakeven inkl. Spread+Gebühren

ONCE TrailingFlag = 0

ONCE newSL = 0//reset the stoploss value

IF NOT ONMARKET THEN

TrailingFlag = 0

newSL = 0

ENDIF//************************//

//manage long positions //

//***********************//

IF LOngONMarket AND TrailingFlag = 1 THEN

newSL = tradeprice-(trailingstartL*pipsize)

ENDIF

//breakeven

IF LOngONMarket AND (close-tradeprice) >= ((SaveDistanceL+MinimumPlus)*pipsize) AND TrailingFlag = 1 THEN

newSL = Close-((SaveDistanceL)*pipsize)

TrailingFlag = 3

ENDIF

IF LOngONMarket AND (close-newSL) >= ((trailingL)*pipsize) AND TrailingFlag = 3 THEN

newSL = close-(trailingL*pipsize)

ENDIF

IF LongOnMarket AND TrailingFlag = 2 THEN

newSL = Close-(trailingR*pipsize)

ENDIF

//breakeven

IF LongOnMarket AND (close-tradeprice) >= ((MinimumPlus+SaveDistanceL)) THEN

newSL = Close-(SaveDistanceL)

TrailingFlag = 4

ENDIF

IF LongOnMarket AND (close-newSL) > (trailingL) AND TrailingFlag = 4 THEN

newSL = newSL+(close-trailingL)

ENDIF//************************//

//manage Short positions //

//************************//

IF ShortONMarket AND TrailingFlag = 1 THEN

newSL = tradeprice+(trailingstartS*pipsize)

ENDIF

//breakeven

IF ShortOnMarket AND (tradeprice-close) >= ((SaveDistanceS+MinimumPlus)*pipsize) AND TrailingFlag = 1 THEN

TrailingFlag = 3

newSL = Close+((SaveDistanceS)*pipsize)

ENDIF

IF ShortOnMarket AND (newSL-close) >= (trailingS*pipsize) AND TrailingFlag = 3 THEN

newSL = close+(trailingS*pipsize)

ENDIF

IF ShortOnMarket AND TrailingFlag = 2 THEN

newSL = Close+(trailingR*pipsize)

ENDIF

//breakeven

IF ShortOnMarket AND (tradeprice-close) >= ((MinimumPlus+SaveDistanceS)) THEN

newSL = Close-(SaveDistanceS)

TrailingFlag = 4

ENDIF

IF ShortOnMarket AND (newSL-close) => (trailingS) AND TrailingFlag = 4 THEN

newSL = close+((trailingS))

ENDIF//**********************************//

//stop order to exit the positions //

//*********************************//

IF LONGONMARKET AND Close <= Lowest[1440] AND newSL > 0 THEN

SELL AT MARKET

TrailingFlag = 0

ELSIF ShortOnMarket AND Close >= Highest[1440] AND NewSL > 0 THEN

EXITSHORT AT MARKET

TrailingFlag = 0

ENDIF

IF LongonMarket AND newSL > 0 AND close < newSL THEN

SELL AT MARKET

ELSIF ShortOnMarket AND newSL > 0 AND close > newSL THEN

EXITSHORT AT MARKET

ENDIF

IF LONGOnMarket AND newSL > 0 AND ((Close < newSL) OR (Average[20] crosses under Average[30] AND Average[30] < Average[50] AND Close < Average[2000] AND Close < Average[100] AND Average[100] < Average[200]) AND Close < Close[1] AND Close < tradeprice-100) THEN

SELL AT MARKET

TrailingFlag = 0

ELSIF ShortOnMarket AND newSL > 0 AND ((Close => newSL) OR (Average[20] > Average[30] AND Average[30] > Average[50] AND Close > Average[2000] AND Close > Average[100] AND Average[100] > Average[200]) AND Close > Close[1] AND Close > tradeprice+100 ) THEN

EXITSHORT AT MARKET

TrailingFlag = 0

ENDIF

IF Time = 220000 THEN

IF LongOnMarket THEN

newSL = newSL +2

ELSIF ShortOnMarket THEN

newSL = newSL -2

ENDIF

ENDIF//stop order to exit the positions if price went high/low enough

IF LongonMarket AND (Close - TradePrice) > 250 THEN

SELL AT MARKET

newSL = 0

TrailingFlag = 0

ELSIF ShortonMarket AND (TradePrice - Close) > 250 THEN

EXITSHORT AT MARKET

newSL = 0

TrailingFlag = 0

ENDIF//stop order to exit the positions if marketClose and price went high/low enough

IF LongonMarket AND (Time >= 220000 OR Time <= 070000) AND (Close - TradePrice) > MinimumPlus THEN

SELL AT MARKET

TrailingFlag = 0

newSL = 0

ELSIF ShortonMarket AND (Time >= 220000 OR Time <= 070000) AND (TradePrice - Close) > MinimumPlus THEN

EXITSHORT AT MARKET

TrailingFlag = 0

newSL = 0

ENDIF//*************************************************************************//

//Dayly-Gap-Strategy //

//*************************************************************************//

IF ClosetryCount < 10 THEN

IF ((TIME = 065900)) AND TradeON AND TradeDay AND NOT OnMarket THEN

IF NOT Forbiddenshort AND Close > Pivot+8 AND Close < Pivot+100 AND Aroondown > 5 AND RSI < 75 AND NOT Trendup AND Close < Average[10000] AND Close < Supertrend THEN

Sellshort PositionSizeShort Contracts AT MARKET

SET TARGET pProfit (Close-Pivot)-5

SET STOP pLOSS 50*Faktor1

ClosetryCount = ClosetryCount +1

ENDIF

IF Not Forbiddenlong AND Close < Pivot-8 AND Close > Pivot-55 AND Aroonup > 0 AND RSI > 20 AND NOT Trenddown AND Close = Highest[30] THEN

Buy PositionSizeLong Contracts AT MARKET

SET TARGET pProfit (Pivot-Close)-5

SET STOP pLOSS 50*Faktor1

ClosetryCount = ClosetryCount +1

ENDIF

ENDIFIF ((TIME = 075900)) AND NOT Reachedboth AND TradeON AND TradeDay AND NOT OnMarket THEN

IF NOT Forbiddenshort AND Close > Pivot+8 AND Close < Pivot+100 AND Aroondown > 5 AND RSI < 75 AND MACD < 2 AND NOT Trendup AND Close < Average[10000] AND Close < Supertrend THEN

Sellshort PositionSizeShort Contracts AT MARKET

SET TARGET pProfit (Close-Pivot)-5

SET STOP pLOSS 50*Faktor1

ClosetryCount = ClosetryCount +1

ENDIF

IF Not Forbiddenlong AND Close < Pivot-8 AND Close > Pivot-55 AND Aroonup > 0 AND RSI > 20 AND MACD > -1 AND NOT Trenddown AND Close = Highest[30] THEN

Buy PositionSizeLong Contracts AT MARKET

SET TARGET pProfit (Pivot-Close)-5

SET STOP pLOSS 50*Faktor1

ClosetryCount = ClosetryCount +1

ENDIF

ENDIFIF ((TIME >= 085400) AND (TIME <= 085500)) AND TradeON AND TradeDay THEN

IF NOT Forbiddenshort AND NOT OnMarket AND Close > Pivot+8 AND Close < Pivot+100 AND Aroondown > 10 AND RSI < 75 AND MACD < 2 AND Close < Average[200] AND Close < Average[10] AND NOT Trendup AND Close < Supertrend THEN

Sellshort PositionSizeShort Contracts AT MARKET

SET TARGET pProfit (Close-Pivot)-5

SET STOP pLOSS 50*Faktor1

ClosetryCount = ClosetryCount +1

ENDIF

IF Not Forbiddenlong AND NOT OnMarket AND Close < Pivot+8 AND Close > Pivot-55 AND Aroonup > 10 AND RSI > 20 AND MACD > -1 AND Close > Average[200] AND CLose > Average[1000] THEN

Buy PositionSizeLong Contracts AT MARKET

SET TARGET pProfit (Pivot-Close)-5

SET STOP pLOSS 50*Faktor1

ClosetryCount = ClosetryCount +1

ENDIF

ENDIFIF ((TIME >= 092500) AND (TIME <= 093500)) AND TradeON AND TradeDay THEN

IF NOT Forbiddenshort AND NOT OnMarket AND Close > Pivot+8 AND Close < Pivot+100 AND Aroondown > 20 AND RSI < 70 AND MACD < 1 AND Close < Average[200] AND Average[50] < Average[100] AND Average[100] < Average[200] AND Close < Average[10000] AND Overboth AND Close = Lowest[90] THEN

Sellshort PositionSizeShort Contracts AT MARKET

SET TARGET pProfit (Close-Pivot)-5

SET STOP pTrailing 100*Faktor1

ClosetryCount = ClosetryCount +1

ENDIF

IF Not Forbiddenlong AND NOT Onmarket AND Close < Pivot+8 AND Close > Pivot-100 AND Aroonup > 20 AND RSI > 25 AND MACD > 0 AND Close > Average[200] AND Average[50] > Average[200] AND Average[100] > Average[200] AND Close < XetraClose AND Underboth AND Close = Highest[90] THEN

Buy PositionSizeLong Contracts AT MARKET

SET TARGET pProfit (Pivot-Close)-5

SET STOP pTrailing 100*Faktor1

ClosetryCount = ClosetryCount +1

ENDIF

ENDIFIF (TIME >= 080000 AND TIME <= 113000) AND Tradeon AND Tradeday THEN

IF NOT ForbiddenShort AND Not Onmarket AND Overboth AND Reachedboth = 0 AND (Close > Average[4500]) AND (Close > Average[100]) AND (Close > Average[1000]) AND ((Average[2500] > Average[1000]) OR (Average[4500] > Average[2500]) OR (Average[4500] > Average[1000])) AND Aroondown > 5 AND RSI < 75 AND MACD < 2 AND Close < Highest[600] AND Close < Close[1] AND Close < Supertrend THEN

Sellshort PositionSizeShort Contracts AT MARKET

ClosetryCount = ClosetryCount +1

IF Close > DayClose+10 AND DayClose > (max(Pivot,XetraClose)) THEN

SET TARGET pProfit (Close - DayClose)-5

ELSE

SET TARGET pProfit (Close-min(min(DayClose,XetraClose),Pivot))-5

ENDIF

SET STOP pTrailing 220*Faktor1

ELSIF NOT ForbiddenShort AND Not Onmarket AND Reachedboth = 0 AND (Close > Average[100]) AND (Close < Average[1000]) AND (Average[2500] < Average[1000]-15) AND (Average[4500] < Average[2500]) AND Aroondown > 5 AND RSI < 75 AND MACD < 2 AND Close < Highest[600] AND NOT Trendup AND Close < Close[1] AND Close < Supertrend THEN

Sellshort PositionSizeShort Contracts AT MARKET

ClosetryCount = ClosetryCount +1

IF Close > DayClose+10 AND DayClose > (max(Pivot,XetraClose)) THEN

SET TARGET pProfit (Close - DayClose)-5

ELSE

SET TARGET pProfit (Close-max(max(DayClose,XetraClose),Pivot))-5

ENDIF

SET STOP pTrailing 170*Faktor1

ELSIF NOT ForbiddenLong AND NOT OnMarket AND Underboth AND Reachedboth = 0 AND ((Close < Average[4500]) AND Close < Average[100]) AND ((Average[2500] < Average[1000]) OR (Average[4500] < Average[2500]) OR (Average[4500] < Average[1000])) AND Aroonup > 15 AND RSI > 20 AND RSI < 75 AND Close > Close[1] AND Close > Supertrend THEN

Buy PositionSizeLong Contracts AT MARKET

ClosetryCount = ClosetryCount +1

IF Close < DayClose-10 AND DayClose < (min(XetraClose,Pivot)) THEN

SET TARGET pProfit (DayClose-Close)-5

ELSE

SET TARGET pProfit (max(max(DayClose,XetraClose),Pivot)-Close)-5

ENDIF

SET STOP pTrailing 170*Faktor1

ELSIF NOT ForbiddenLOng AND NOT OnMarket AND Underboth AND Reachedboth = 0 AND ((Close > Average[4500]) AND Close > Average[100]) AND ((Average[2500] > Average[1000]) AND (Average[4500] < Average[2500]) AND (Average[4500] < Average[1000])) AND Aroonup > 5 AND RSI > 20 AND MACD > -5 AND NOT Trenddown AND RSI < 75 AND Close > Close[1] AND Close > Supertrend THEN

Buy PositionSizeLong Contracts AT MARKET

ClosetryCount = ClosetryCount +1

IF Close < DayClose-10 AND DayClose < (min(XetraClose,Pivot)) THEN

SET TARGET pProfit (DayClose-Close)-5

ELSE

SET TARGET pProfit (max(XetraClose,Pivot)-Close)-5

ENDIF

SET STOP pTrailing 170*Faktor1

ELSIF NOT ForbiddenLong AND NOT OnMarket AND Underboth AND Reachedboth = 0 AND ((Average[2500] > Average[1000]) OR (Average[4500] > Average[2500]) OR (Average[4500] > Average[1000])) AND Close > Average[100] AND Average[200] > Average[1000] AND Aroonup > 5 AND RSI > 20 AND MACD > -5 AND NOT Trenddown AND RSI < 75 AND Close > Close[1] AND Close > Supertrend THEN

Buy PositionSizeLong Contracts AT MARKET

ClosetryCount = ClosetryCount +1

IF Close < DayClose-10 AND DayClose < (min(XetraClose,Pivot)) THEN

SET TARGET pProfit (DayClose-Close)-5

ELSE

SET TARGET pProfit (max(XetraClose,Pivot)-Close)-5

ENDIF

SET STOP pTrailing 170*Faktor1

ELSIF NOT ForbiddenLong AND NOT OnMarket AND Underboth AND Reachedboth = 0 AND ((Average[2500] > Average[1000]) AND (Average[4500] > Average[2500]) AND (Average[1000] > Average[200]) AND Average[200] > Average[100]) AND Close > Average[100] AND Aroonup > 5 AND RSI > 20 AND MACD > -2 AND RSI < 75 AND Close > Close[1] AND Close > Supertrend THEN

Buy PositionSizeLong Contracts AT MARKET

ClosetryCount = ClosetryCount +1

IF Close < DayClose-10 AND DayClose < (min(XetraClose,Pivot)) THEN

SET TARGET pProfit (DayClose-Close)-5

ELSE

SET TARGET pProfit (max(XetraClose,Pivot)-Close)-5

ENDIF

SET STOP pTrailing 200*Faktor1

ENDIF

ENDIF

ENDIF//*************************************************************************//

//Tagesschluss Rallye und Down M/W/D: o/o/o //

//*************************************************************************//

//up

IF Time >= 164500 AND Time <= 173000 AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenLong AND Close => hi THEN

IF Close > (Pivot) THEN

IF RSI > 20 AND MACD > -2 AND Close > Average[100] AND AroonUp > 5 AND MA20over AND Close < Highest[840] THEN

BUY PositionsizeLong CONTRACTS AT MARKET

SET STOP pLOSS 60*Faktor1

ENDIF

ELSIF Close < Pivot AND RSI > 20 AND MACD > -2 AND Close > Average[100] AND AroonUp > 0 AND MA20over AND Average[50] > Average[100] THEN

BUY PositionsizeLong CONTRACTS AT MARKET

SET STOP pLOSS 60*Faktor1

ENDIF

ENDIFIF Time >= 175000 AND Time <= 210000 AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenLong AND Close => hi THEN

IF Close < (Pivot) THEN

IF RSI > 20 AND MACD > -2 AND Close > Average[100] AND Average[100] > Average[200] AND Average[200] < Average[1000] AND Average[1000] < Average[2500] AND Average[2500] < Average[4500] AND AroonUp > 0 AND MA20over THEN

BUY PositionsizeLong CONTRACTS AT MARKET

SET STOP pLOSS 60*Faktor1

ENDIF

ENDIF

ENDIF//down

IF (Time >= 164500 AND Time <= 173000) AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenShort AND Close <= lo THEN

IF Close < (Pivot) THEN

IF RSI < 85 AND MACD < 2 AND Close < Average[50] AND AroonDown > 5 AND MA20under THEN

SellShort PositionsizeShort CONTRACTS AT MARKET

SET STOP pLOSS 60*Faktor1

ENDIF

ENDIF

ENDIFIF Opendayofweek = 5 AND (Time >= 175000 AND Time <= 184500) AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenShort AND Close <= lo THEN

IF Close > Pivot AND RSI < 25 AND MACD < -2 AND Close < Average[20] AND Close < Average[50] AND AroonDown > 5 AND Close < Average[100] THEN

SellShort PositionsizeShort CONTRACTS AT MARKET

SET STOP pLOSS 60*Faktor1

ENDIF

ENDIFIF (Time >= 180000 AND Time <= 190000) AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenShort AND Close <= lo THEN

IF Close > Pivot AND NOT ReachedXetra AND RSI < 75 AND MACD < 2 AND Close < Average[50] AND AroonDown > 5 AND MA20under AND Average[100] < Average[200] THEN

SellShort PositionsizeShort CONTRACTS AT MARKET

SET STOP pLOSS 60*Faktor1

ENDIF

ENDIFIF Time >= 180000 AND Time <= 200000 AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenShort AND Close <= lo THEN

IF Close > (Pivot) THEN

IF RSI < 75 AND MACD < 2 AND Close < Average[100] AND Average[100] < Average[200] AND Average[100] > Average[1000]+25 AND Average[1000] > Average[2500] AND AroonDown > 0 AND MA20under THEN

Sellshort PositionsizeShort CONTRACTS AT MARKET

SET STOP pLOSS 60*Faktor1

ENDIF

ENDIF

ENDIFIF Time >= 190000 AND Time <= 215900 AND TradeDay AND TRADEON THEN

IF Close > ResR1 AND NOT ONMARKET AND NOT ForbiddenShort AND Close <= lo THEN

IF RSI < 75 AND MACD < 2 AND Close < Average[10] AND Average[10] < Average[30] AND Average[100] < Average[200] AND Average[200] > Average[1000] AND MA30under AND AroonDown > 0 THEN

Sellshort PositionsizeShort CONTRACTS AT MARKET

SET STOP pLOSS 60*Faktor1

ENDIF

ELSIF Close < SupS1 AND NOT ONMARKET AND NOT ForbiddenLong AND Close >= hi THEN

IF RSI > 25 AND MACD > -2 AND Close > Average[10] AND Average[10] < Average[30] AND MA30over AND Average[100] > Average[200] AND Average[200] < Average[1000] AND AroonUp > 0 THEN

Buy PositionsizeLong CONTRACTS AT MARKET

SET STOP pLOSS 60*Faktor1

ENDIF

ENDIF

ENDIF// JahresendRallye

IF Time >= 143000 AND Time <= 171500 AND Close > Average[10000] AND Tradeday AND TradeON AND NOT ForbiddenLong AND NOT Trenddown AND NOT ONMARKET AND Close > Close[1] AND RSI > 25 AND RSI < 85 AND Close > Average[10] AND Average[20] > Average[30] AND AroonUp > 5 AND Close = Highest[60] AND Close < ResR3 AND (Close MOD 100) > 20 AND MACDLine < 10 AND Close > Average[1000] THEN

BUY PositionSizeLong CONTRACTS AT MARKET

SET STOP pTrailing 100*Faktor1

ENDIF// Nachmittagsanstieg

IF Time >= 143000 AND Time <= 200000 AND NOT Reachedboth AND Tradeday AND TradeON AND NOT ForbiddenLong AND Trendup AND CurrentMonth < 10 AND NOT ONMARKET AND Close > Close[1] AND RSI > 25 AND RSI < 85 AND Close > Average[10] AND Average[20] > Average[30] AND AroonUp > 5 AND Close = Highest[60] AND (Close MOD 100) > 20 AND MACDLine < 10 AND Close > Average[1000] THEN

BUY PositionSizeLong CONTRACTS AT MARKET

SET STOP pTrailing 100*Faktor1

ENDIF//*************************************************************************// //Modular Algorithm Library V2.0 // //*************************************************************************// //Modules: //Market-Data-Definition+Parameter ///Monthly/Weekly/Daily-Modifiers, Xetra-HLC-Correction, Strategy-Stop-Code mit Money-Management //Moving-Average-Clustering-Filter, Robustness-Test, Stop-Loss/Trailing-Routines Long/Short/Risk //Long/Short-Support2/Resistance2-Break-Filter, HexenSabbat-Filter //Trading Code //*************************************************************************// //Parameter // //*************************************************************************// DEFPARAM PreLoadBars = 10000 DEFPARAM CumulateOrders = false ONCE TradeON = 0 ONCE Tradeday = 0 ONCE IndexFaktoring = 0 // 1=ON 0=OFF Faktoring des Indexkurses ONCE ClusterSave = 2 // 0=OFF 1=small 2=large 3=all MovingAverage-Clustering-Filter ONCE startingsize = 0.25 // starting position size ONCE maxsize = 2 // maximal positionsize ONCE ForbiddenLSFlag = 0 // 0=OFF 1=ON 2=Reverse 3=Strict 4=StrictReverse S1/S2/Short-R1/R2/Long-Filter ONCE RobustnessTest = 0 // 0=OFF 1=ON Robustness-Test ONCE SSC = 0 // 0=OFF 1=ON 2=Alternative Strategy-Stop-Code ONCE Reinvest = 1 // 0=OFF 1=ON Gewinne reinvestieren ONCE ReinvestValue = 0.5 //Reinvestitionsanteil ONCE StartingCapital = 20000 // Startkapital ONCE Modifiers = 1 // 0=OFF 1=ON Modifikatoren auf PositionSize ONCE DaySLFlag = 1 // 0=OFF 1=ON Intraday Short/Long-Reversal-Flag (Modifier) ONCE MarketFlag = 1 // 1=DAX 2=DJI Marktauswahl ONCE HexSabFilter = 1 // 0=OFF 1=ON HexenSabbatFilter ONCE Overnight = 1 // 0=NO 1=YES Overnight Holding allowed //*************************************************************************// //Market Data // //*************************************************************************// ONCE Opening = 080000 // Eröffnungszeit DAX ONCE Closing = 220000 // Schlusszeit DAX ONCE TF = 1 // TimeFrame in Minuten DAX ONCE SpreadGeb = 4 // Spread+Gebühren DAX ONCE Indexfaktor = 13000 ONCE Faktor1 = Close / Indexfaktor ONCE FaktorTS = 1 // Trailing-Stop-Multiplikator IF MarketFlag = 1 THEN Opening = 080000 // Eröffnungszeit DAX Closing = 220000 // Schlusszeit DAX TF = 1 // TimeFrame in Minuten DAX SpreadGeb = 4 // Spread+Gebühren DAX ONCE FaktorTS = 1 // Trailing-Stop-Multiplikator IF IndexFaktoring = 1 THEN Indexfaktor = 14000 ELSIF Indexfaktoring = 0 THEN Indexfaktor = Close ENDIF Faktor1 = Close / Indexfaktor ENDIF IF MarketFlag = 2 THEN Opening = 080000 // Eröffnungszeit DJI Closing = 220000 // Schlusszeit DJI TF = 1 // TimeFrame in Minuten DJI SpreadGeb = 4 // Spread+Gebühren DJI IF IndexFaktoring = 1 THEN Indexfaktor = 30000 ELSIF Indexfaktoring = 0 THEN Indexfaktor = Close ENDIF Faktor1 = Close / Indexfaktor ONCE FaktorTS = 2.5 // Trailing-Stop-Multiplikator ENDIF IF OpenDayOfWeek > 0 AND OpenDayOfWeek < 6 AND NOT (Month = 10 AND Day = 3) AND NOT (Month = 5 AND Day = 1) AND NOT (Month = 12 AND Day = 24) AND NOT (MONTH = 12 AND Day = 25) AND NOT (MONTH = 12 AND Day = 26) AND NOT (MONTH = 12 AND Day = 30) AND NOT (MONTH = 12 AND Day = 26) THEN Tradeday = 1 ELSE Tradeday = 0 ENDIF //Flat Failsave If ONMARKET AND Overnight = 0 AND (Time < Opening OR Time > Closing) THEN SELL AT Market EXITSHORT AT Market ENDIF //*************************************************************************// //Algorithm Robustness-Test // //*************************************************************************// StartDate = 20000101 // Parameter Qty = 5 // Parameter Rndom = 3 // Parameter once j = 0 once flag = 1 IF RobustnessTest = 1 THEN if flag = 1 then j = j + 1 if j > qty then flag = -1 j = j - 1 endif endif if flag = -1 then j = j - 1 if j = 0 then j = j + rndom flag = 1 endif endif if opendate >= startdate AND (barindex mod qty = 0 or barindex mod qty = j) then tradeon = 1 ELSIF opendate >= startdate AND NOT (barindex mod qty = 0 or barindex mod qty = j) then tradeon = 0 endif ENDIF //*************************************************************************// //Strategy-Stop-Code, Money Management/ReInvest // //*************************************************************************// barsbeforenextcheck = 30 // number of bars between performance checks drawdownquitting = 1 // drawdown quitting on or off (on=1 off=0) winratequit = 50 // minimum win rate in % allowed before quitting (0 = off) tradesbeforewrquit = 50 // number of trades required before a win rate stop of strategy is allowed to happen increase = 1 // position size increasing on or off (on=1 off=0) decrease = 1 // position size decreasing on or off (on=1 off=0) capital = StartingCapital // starting capital minpossize = 1 // minimum position size allowed gaintoinc = 5 // % profit rise needed before an increase in position size is made losstodec = 5 // % loss needed before a decrease in position size is made maxdrawdown = 50 // maximum % draw down allowed from highest ever equity before stopping strategy maxcapitaldrop = 50 // maximum % starting capital lost before stopping strategy ONCE highestprofit = 0 ONCE count = 0 ONCE win = 0 ONCE winrate = 0 ONCE MMpositionsize = 1 ONCE psperc = (MMpositionsize*startingsize) / (capital/100) ONCE equity = StartingCapital ONCE Profit1 = 0 IF SSC = 1 THEN if strategyprofit < strategyprofit[1] then Profit1 = highestprofit - (strategyprofit[1] - strategyprofit) highestprofit = highestprofit - Profit1 Profit1 = 0 ELSIF strategyprofit > strategyprofit[1] then Profit1 = (strategyprofit - strategyprofit[1])*0.7 highestprofit = highestprofit + Profit1 Profit1 = 0 if count < tradesbeforewrquit OR winrate > winratequit/100 then count = count + 1 if strategyprofit > strategyprofit[1] then win = win + 1 endif ENDIF winrate = win/count ENDIF if count >= tradesbeforewrquit AND winrate < winratequit/100 then quit endif if barindex mod barsbeforenextcheck = 0 AND drawdownquitting AND highestprofit <> 0 then if (capital + strategyprofit) <= (capital + highestprofit) - ((capital + highestprofit)*(maxdrawdown/100)) then quit endif endif if count >= tradesbeforewrquit AND highestprofit = 0 then if (capital + strategyprofit) <= capital - (capital * (maxcapitaldrop/100)) then quit endif ENDIF IF SSC = 2 THEN MMpositionsize = max(((equity)/startingcapital),minpossize) ENDIF ENDIF //*******************************************************************************************// //Position Size,Monthly,Weekly,Daily,Intra,Trend,Reversal Modifiers (optional) // //*******************************************************************************************// //Berechnung am Schluss löschen ( auf 1 setzen) für Löschen des Modifikators ONCE PSizeL = startingsize ONCE PSizeS = startingsize ONCE MonthSizeL = 0 ONCE MonthSizeS = 0 ONCE WeekSizeL = 0 ONCE WeekSizeS = 0 ONCE DaySizeL = 0 ONCE DaySizeS = 0 ONCE Monatsanfang = 0 ONCE Monatsende = 0 ONCE IntraSizeL = 0 ONCE IntraSizeS = 0 ONCE GapCloseup = 0 ONCE GapClosedown = 0 ONCE VBaisse = 0 ONCE VHausse = 0 ONCE SentimentSizeL = 0 ONCE SentimentSizeS = 0 ONCE MidMonthSizeL = 0 IF Modifiers = 1 THEN IF MarketFlag = 1 THEN IF XetraClose > XetraCloseOld THEN VHausse = VHausse +1 VBaisse = 0 ELSIF XetraClose < XetraCloseOld THEN VHausse = 0 VBaisse = VBaisse +1 ENDIF IF VHausse > 5 THEN SentimentSizeS = 0.5 ELSIF VBaisse > 5 THEN SentimentSizeL = 0.5 ENDIF IF Day > 8 AND Day < 12 THEN MidMonthSizeL = 0.5 ELSE MidMonthSizeL = 0 ENDIF IF CurrentMonth = 1 THEN MonthSizeS = 0.25 MonthSizeL = 0 ELSIF CurrentMonth >= 2 AND CurrentMonth >= 3 THEN MonthSizeS = 0 MonthSizeL = 0.25 ELSIF CurrentMonth = 4 THEN MonthSizeS = 0 PMonthSizeL = 0.5 ELSIF CurrentMonth = 5 THEN MonthSizeS = 0 MonthSizeL = 0 ELSIF CurrentMonth = 6 THEN MonthSizeS = 0.25 MonthSizeL = 0 ELSIF CurrentMonth = 7 THEN MonthSizeS = 0 MonthSizeL = 0.25 ELSIF CurrentMonth >= 8 AND CurrentMonth <= 9 THEN MonthSizeS = 0.25 MonthSizeL = 0 ELSIF CurrentMonth >= 10 AND CurrentMonth <= 12 THEN MonthSizeS = 0 MonthSizeL = 0.5 ENDIF IF Time = Opening THEN If Day >= 01 AND Day <= 08 THEN Monatsanfang = 1 ELSIF Day >= 25 AND Day <= 31 THEN Monatsende = 1 ENDIF ENDIF IF Monatsanfang = 1 THEN IF CurrentMonth >= 1 AND CurrentMonth <= 7 THEN WeekSizeL = 0.25 WeekSizeS = 0 ELSIF CurrentMonth >= 8 AND CurrentMonth <= 9 THEN WeeksizeL = 0 WeekSizeS = 0.25 ELSIF CurrentMonth = 10 THEN WeeksizeL = 0 WeekSizeS = 0 ELSIF CurrentMonth >= 11 AND CurrentMonth <= 12 THEN WeekSizeL = 0.25 WeekSizeS = 0 ENDIF ENDIF IF Monatsende = 1 THEN IF CurrentMonth = 1 THEN WeekSizeL = 0.25 WeekSizeS = 0 ELSIF CurrentMonth = 2 THEN WeekSizeL = 0 WeekSizeS = 0 ELSIF CurrentMonth >= 3 AND CurrentMonth <= 6 THEN WeeksizeL = 0.25 WeekSizeS = 0 ELSIF CurrentMonth = 7 THEN WeekSizeL = 0 WeekSizeS = 0 ELSIF CurrentMonth >= 8 AND CurrentMonth <= 9 THEN WeekSizeL = 0 WeekSizeS = 0.5 ELSIF CurrentMonth >= 10 AND CurrentMonth <= 12 THEN WeeksizeL = 0.5 WeekSizeS = 0 ENDIF ENDIF IF OpenDayofWeek = 1 THEN DaySizeL = 0.25 DaySizeS = 0 ELSIF OpenDayofWeek = 5 Then DaySizeL = 0 DaySizeS = 0.25 ELSIF OpenDayofWeek <1 OR (OpenDayofWeek >= 2 AND OpenDayOfWeek <= 4) OR OpenDayofWeek = 6 THEN DaySizeL = 0 DaySizeS = 0 ENDIF IF Close < DLow(1) AND DaySLFlag = 1 THEN IntraSizeL = 0.25 IntraSizeS = 0 ELSIF Close > DHigh(1) AND DaySLFlag = 1 THEN IntraSizeL = 0 IntraSizeS = 0.25 ELSIF DaySLFlag = 0 THEN IntraSizeL = 0 IntraSizeS = 0 ENDIF IF Time >= Opening AND Time <= Closing THEN IF Close > ResR2 THEN IDReversalL = 0.25 ELSIF Close > ResR3 THEN IDReversalL = 0.5 ELSIF Close < SupS2 AND Close > SupS3 THEN IDReversalS = 0.25 ELSIF Close < SupS3 THEN IDReversalS = 0.5 ELSIF Close < ResR2 AND Close > SupS2 THEN IDReversalL = 0 IDReversalS = 0 ENDIF ENDIF IF Time = Closing THEN TrendUp = 0 TrendDown = 0 ENDIF IF Time = Opening THEN IF DHigh(1) > DHigh(2) AND DLow(1) > DLow(2) THEN TrendUp = 0.25 TrendDown = 0 ELSIF DHigh(1) < DHigh(2) AND DLow(1) < DLow(2) THEN TrendUp = 0 TrendDown = 0.25 ENDIF ENDIF IF Time = Opening AND XetraCloseOld > XetraClose AND Close < XetraClose-10 THEN GapCloseup = 0.5 GapClosedown = 0 ELSIF Time = Opening AND XetraCloseOld < XetraClose AND Close > XetraClose+10 THEN GapCloseup = 0 GapClosedown = 0.5 ENDIF ELSIF MarketFlag = 2 THEN IF CurrentMonth = 1 THEN MonthSizeS = 0.25 MonthSizeL = 0 ELSIF CurrentMonth = 3 OR CurrentMonth = 4 OR CurrentMonth = 5 THEN MonthSizeS = 0 PMonthSizeL = 0.25 ELSIF CurrentMonth = 6 THEN MonthSizeS = 0.25 MonthSizeL = 0 ELSIF CurrentMonth = 7 OR CurrentMonth = 8 THEN MonthSizeS = 0 MonthSizeL = 0 ELSIF CurrentMonth = 9 THEN MonthSizeS = 0.25 MonthSizeL = 0 ELSIF CurrentMonth >= 10 AND CurrentMonth <= 12 THEN MonthSizeS = 0 MonthSizeL = 0.5 ENDIF ENDIF ENDIF //Einzelne Komponenten können nach belieben hier gelöscht werden, um die Modifikationen an eigene Vorstellungen anzupassen IF Reinvest = 1 THEN PositionSizeLong = (PSizeL*(PSizeL+TrendUp+IDReversalL+IntraSizeL+DaySizeL+WeekSizeL+MonthSizeL+GapCloseup+SentimentSizeL+MidMonthSizeL)*Min(maxsize,(1+(strategyprofit/startingcapital)*Reinvestvalue))*MMpositionsize) PositionSizeShort = (PSizeS*(PSizeS+TrendDown+IDReversalS+IntraSizeS+DaySizeS+WeekSizeL+MonthSizeS+GapClosedown+SentimentSizeS)*Min(maxsize,(1+(strategyprofit/startingcapital)*Reinvestvalue))*MMpositionsize) ELSIF Reinvest = 0 THEN PositionSizeLong = Min(maxsize,(PSizeL*(PSizeL+TrendUp+IDReversalL+IntraSizeL+DaySizeL+WeekSizeL+MonthSizeL+GapCloseup+SentimentSizeL+MidMonthSizeL))*MMpositionsize) PositionSizeShort = Min(maxsize,(PSizeS*(PSizeS+TrendDown+IDReversalS+IntraSizeS+DaySizeS+WeekSizeL+MonthSizeS+GapClosedown+SentimentSizeS))*MMpositionsize) ELSIF Modifiers = 0 THEN PositionSizeLong = Min(maxsize,(PSizeL*MMpositionsize)) PositionSizeShort = Min(maxsize,(PSizeS*MMpositionsize)) ENDIF //*************************************************************************// //Xetra-Korrektur High Low Close, Pivot, Resistance, Support , Flags // //*************************************************************************// ONCE DayClose = 14536 // last numbers before start of algorithm ONCE DayHigh = 14586 ONCE DayLow = 14389 ONCE XetraClose = 14523 ONCE XetraCloseOld = 14423 ONCE ReachedXetra = 1 ONCE ReachedDayClose = 1 ONCE Reachedboth = 1 ONCE ClosetryCount = 0 IF Time = 060000 THEN ReachedXetra = 0 ReachedDayClose = 0 Reachedboth = 0 ClosetryCount = 0 ENDIF IF Time >= 070000 AND Time <= 113000 THEN IF Close >= XetraClose-15 AND Close <= XetraClose+12 THEN ReachedXetra = 1 ENDIF IF Close >= DayClose-10 AND Close <= DayClose+12 THEN ReachedDayClose = 1 ENDIF IF (ReachedXetra = 1) AND (ReachedDayClose = 1) THEN Reachedboth = 1 ENDIF ENDIF Overboth = (Close-5 > XetraClose AND XetraClose > DayClose) OR (Close-5 > DayClose AND DayClose > XetraClose) Underboth = (Close+5 < XetraClose AND XetraClose < DayClose) OR (Close+5 < DayClose AND DayClose < XetraClose) AmplitudeMin = 10 hi = Highest[15](close[1]) lo = Lowest[15](close[1]) IF Time = 174400 AND OPENDAYOFWEEK <6 AND OPENDAYOFWEEK >0 AND Tradeday THEN IF (Close < XetraClose AND (Highest[585] < XetraClose-5)) OR ((Close > XetraClose) AND Lowest[585] > XetraClose+5) THEN XetraCloseOld = XetraClose ENDIF ENDIF IF TIME = 174500 AND OPENDAYOFWEEK <6 AND OPENDAYOFWEEK >0 AND Tradeday THEN XetraClose = Close[0] ENDIF IF Time = 220000 AND OPENDAYOFWEEK <6 AND OPENDAYOFWEEK >0 AND Tradeday then DayClose = Close[0] DayHigh = Highest[(840/TF)](close[0]) DayLow = Lowest[(840/TF)](close[0]) ENDIF if Time = 220000 AND OPENDAYOFWEEK <6 AND OPENDAYOFWEEK >0 AND Tradeday then Pivot = (DayHigh + DayLow + DayClose) / 3 ResR1 = Pivot + (Pivot - DayLow) ResR2 = Pivot + (Dayhigh - Daylow) ResR3 = Dayhigh + (2 * (Pivot - Daylow)) SupS1 = Pivot - (Dayhigh - Pivot) SupS2 = Pivot - (Dayhigh - Daylow) SupS3 = Daylow - (2 * (Dayhigh - Pivot)) ENDIF //*************************************************************************// //Moving-Average-Clustering-FilterCode (optional) // //*************************************************************************// xx = 15*pipsize //20-pip range xy = 15*pipsize //20-pip range ma4500 = Average[4500,0](close) ma2500 = Average[2500,0](close) ma1000 = average[1000,0](close) ma50 = average[50,0](close) ma100 = average[100,0](close) ma200 = average[200,0](close) MaxMA = max(ma1000,max(ma2500,max(ma100,ma200))) MinMA = min(ma1000,min(ma2500,min(ma100,ma200))) IF ClusterSave = 1 OR ClusterSave = 3 THEN IF (MaxMA - MinMA) <= xx THEN Tradeon = 0 ELSIF (MaxMA - MinMA) > xx THEN IF RobustnessTest = 0 THEN Tradeon = 1 ELSIF opendate >= startdate AND NOT (barindex mod qty = 0 or barindex mod qty = j) THEN Tradeon = 0 ENDIF ENDIF ENDIF IF ClusterSave >= 2 THEN IF (max(ma4500,ma2500)-min(ma4500,ma2500) < xy) OR (max(ma4500,ma1000)-min(ma4500,ma1000) < xy) OR (max(ma2500,ma1000)-min(ma2500,ma1000) < xy) THEN Tradeon = 0 ENDIF ENDIF //*************************************************************************// //R2-Long/S2-Short Filter (optional) // //*************************************************************************// ONCE ForbiddenLong = 0 ONCE ForbiddenShort = 0 IF ForbiddenLSFlag = 1 THEN ForbiddenLong = Close < SupS2 ForbiddenShort = Close > ResR2 ELSIF ForbiddenLSFlag = 2 THEN ForbiddenLong = Close > ResR2 ForbiddenShort = Close < SupS2 ELSIF ForbiddenLSFlag = 3 THEN ForbiddenLong = Close < SupS1 ForbiddenShort = Close > ResR1 ELSIF ForbiddenLSFlag = 4 THEN ForbiddenLong = Close > ResR1 ForbiddenShort = Close < SupS1 ELSIF ForbiddenLSFlag = 0 THEN ForbiddenLong = 0 ForbiddenShort = 0 ENDIF //*************************************************************************// //MA20/MA50- MA30/50- MA100/200- Cross-Flag // //*************************************************************************// MA20 = Average[20](close) MA30 = Average[30](close) MA50 = Average[50](close) MA100 = Average[100](close) MA200 = Average[200](close) MA20over = (MA20 crosses over MA50) MA20under = (MA20 crosses under MA50) MA30over = (MA30 crosses over MA50) MA30under = (MA30 crosses under MA50) MA100over = (MA100 > MA200) MA100under = (MA100 < MA200) //*************************************************************************// //HexenSabbat-Filter // //*************************************************************************// IF HexSabFilter = 1 THEN IF (CurrentMonth = 3 OR CurrentMonth = 6 OR CurrentMonth = 9 OR CurrentMonth = 12) AND OpenDayofWeek = 5 AND Day >= 15 AND Day <= 21 THEN TradeDay = 0 ELSIF RobustnessTest = 0 AND Opening AND Tradeday THEN TradeOn = 1 ELSE TradeON = 0 ENDIF ELSIF RobustnessTest = 0 AND Opening AND Tradeday THEN TradeON = 1 ELSE TradeON = 0 ENDIF //*************************************************************************// //Daytrend-Flag // //*************************************************************************// ONCE TrendFlag = 0 IF Time = Opening THEN IF DHigh(1) > DHigh(2) AND DLow(1) > DLow(2) THEN TrendFlag = 1 ELSIF DHigh(1) < DHigh(2) AND DLow(1) < DLow(2) THEN TrendFlag = -1 ELSIF NOT (DHigh(1) > DHigh(2) AND DLow(1) > DLow(2)) AND NOT (DHigh(1) < DHigh(2) AND DLow(1) < DLow(2)) THEN TrendFlag = 0 ENDIF ENDIF TrendUp = (TrendFlag = 1) TrendDown = (TrendFlag = -1) //*************************************************************************// //trailing stop function Risk, Long, Short // //*************************************************************************// //wenn gewünscht die Parameter ändern oder die SET STOP-CODES löschen // TrailingFlag = 0 Special (Code im Modul) // TrailingFlag = 1 Normal // TrailingFlag = 2 Risk trailingstartL = 35*FaktorTS*Faktor1 //LONG trailing will start @trailinstart points profit, TrailingFlag = 0 trailingstartS = 35*FaktorTS*Faktor1 //SHORT trailing will start @trailinstart points profit, TrailingFlag = 0 trailingL = 13*FaktorTS*Faktor1 //trailing to move the "stoploss" trailingS= 13*FaktorTS*Faktor1 //trailing to move the "stoploss" trailingR= 11*FaktorTS*Faktor1 //trailing start+to move the "stoploss" for risky positions, TrailingFlag = 2 SaveDistanceL = 16*Faktor1 //Minimum Stop-Abstand 10 lt IG SaveDistanceS = 16*Faktor1 //Minimum Stop-Abstand 10 lt IG SaveDistanceR = 16*Faktor1 //Minimum Stop-Abstand 10 lt IG MinimumPlus = SpreadGeb //Anzahl Pips zum Breakeven inkl. Spread+Gebühren ONCE TrailingFlag = 0 ONCE newSL = 0 //reset the stoploss value IF NOT ONMARKET THEN TrailingFlag = 0 newSL = 0 ENDIF //************************// //manage long positions // //***********************// IF LOngONMarket AND TrailingFlag = 1 THEN newSL = tradeprice-(trailingstartL*pipsize) ENDIF //breakeven IF LOngONMarket AND (close-tradeprice) >= ((SaveDistanceL+MinimumPlus)*pipsize) AND TrailingFlag = 1 THEN newSL = Close-((SaveDistanceL)*pipsize) TrailingFlag = 3 ENDIF IF LOngONMarket AND (close-newSL) >= ((trailingL)*pipsize) AND TrailingFlag = 3 THEN newSL = close-(trailingL*pipsize) ENDIF IF LongOnMarket AND TrailingFlag = 2 THEN newSL = Close-(trailingR*pipsize) ENDIF //breakeven IF LongOnMarket AND (close-tradeprice) >= ((MinimumPlus+SaveDistanceL)) THEN newSL = Close-(SaveDistanceL) TrailingFlag = 4 ENDIF IF LongOnMarket AND (close-newSL) > (trailingL) AND TrailingFlag = 4 THEN newSL = newSL+(close-trailingL) ENDIF //************************// //manage Short positions // //************************// IF ShortONMarket AND TrailingFlag = 1 THEN newSL = tradeprice+(trailingstartS*pipsize) ENDIF //breakeven IF ShortOnMarket AND (tradeprice-close) >= ((SaveDistanceS+MinimumPlus)*pipsize) AND TrailingFlag = 1 THEN TrailingFlag = 3 newSL = Close+((SaveDistanceS)*pipsize) ENDIF IF ShortOnMarket AND (newSL-close) >= (trailingS*pipsize) AND TrailingFlag = 3 THEN newSL = close+(trailingS*pipsize) ENDIF IF ShortOnMarket AND TrailingFlag = 2 THEN newSL = Close+(trailingR*pipsize) ENDIF //breakeven IF ShortOnMarket AND (tradeprice-close) >= ((MinimumPlus+SaveDistanceS)) THEN newSL = Close-(SaveDistanceS) TrailingFlag = 4 ENDIF IF ShortOnMarket AND (newSL-close) => (trailingS) AND TrailingFlag = 4 THEN newSL = close+((trailingS)) ENDIF //**********************************// //stop order to exit the positions // //*********************************// IF LONGONMARKET AND Close <= Lowest[1440] AND newSL > 0 THEN SELL AT MARKET TrailingFlag = 0 ELSIF ShortOnMarket AND Close >= Highest[1440] AND NewSL > 0 THEN EXITSHORT AT MARKET TrailingFlag = 0 ENDIF IF LongonMarket AND newSL > 0 AND close < newSL THEN SELL AT MARKET ELSIF ShortOnMarket AND newSL > 0 AND close > newSL THEN EXITSHORT AT MARKET ENDIF IF LONGOnMarket AND newSL > 0 AND ((Close < newSL) OR (Average[20] crosses under Average[30] AND Average[30] < Average[50] AND Close < Average[2000] AND Close < Average[100] AND Average[100] < Average[200]) AND Close < Close[1] AND Close < tradeprice-100) THEN SELL AT MARKET TrailingFlag = 0 ELSIF ShortOnMarket AND newSL > 0 AND ((Close => newSL) OR (Average[20] > Average[30] AND Average[30] > Average[50] AND Close > Average[2000] AND Close > Average[100] AND Average[100] > Average[200]) AND Close > Close[1] AND Close > tradeprice+100 ) THEN EXITSHORT AT MARKET TrailingFlag = 0 ENDIF IF Time = 220000 THEN IF LongOnMarket THEN newSL = newSL +2 ELSIF ShortOnMarket THEN newSL = newSL -2 ENDIF ENDIF //stop order to exit the positions if price went high/low enough IF LongonMarket AND (Close - TradePrice) > 250 THEN SELL AT MARKET newSL = 0 TrailingFlag = 0 ELSIF ShortonMarket AND (TradePrice - Close) > 250 THEN EXITSHORT AT MARKET newSL = 0 TrailingFlag = 0 ENDIF //stop order to exit the positions if marketClose and price went high/low enough IF LongonMarket AND (Time >= 220000 OR Time <= 070000) AND (Close - TradePrice) > MinimumPlus THEN SELL AT MARKET TrailingFlag = 0 newSL = 0 ELSIF ShortonMarket AND (Time >= 220000 OR Time <= 070000) AND (TradePrice - Close) > MinimumPlus THEN EXITSHORT AT MARKET TrailingFlag = 0 newSL = 0 ENDIF //*************************************************************************// //Dayly-Gap-Strategy // //*************************************************************************// IF ClosetryCount < 10 THEN IF ((TIME = 065900)) AND TradeON AND TradeDay AND NOT OnMarket THEN IF NOT Forbiddenshort AND Close > Pivot+8 AND Close < Pivot+100 AND Aroondown > 5 AND RSI < 75 AND NOT Trendup AND Close < Average[10000] AND Close < Supertrend THEN Sellshort PositionSizeShort Contracts AT MARKET SET TARGET pProfit (Close-Pivot)-5 SET STOP pLOSS 50*Faktor1 ClosetryCount = ClosetryCount +1 ENDIF IF Not Forbiddenlong AND Close < Pivot-8 AND Close > Pivot-55 AND Aroonup > 0 AND RSI > 20 AND NOT Trenddown AND Close = Highest[30] THEN Buy PositionSizeLong Contracts AT MARKET SET TARGET pProfit (Pivot-Close)-5 SET STOP pLOSS 50*Faktor1 ClosetryCount = ClosetryCount +1 ENDIF ENDIF IF ((TIME = 075900)) AND NOT Reachedboth AND TradeON AND TradeDay AND NOT OnMarket THEN IF NOT Forbiddenshort AND Close > Pivot+8 AND Close < Pivot+100 AND Aroondown > 5 AND RSI < 75 AND MACD < 2 AND NOT Trendup AND Close < Average[10000] AND Close < Supertrend THEN Sellshort PositionSizeShort Contracts AT MARKET SET TARGET pProfit (Close-Pivot)-5 SET STOP pLOSS 50*Faktor1 ClosetryCount = ClosetryCount +1 ENDIF IF Not Forbiddenlong AND Close < Pivot-8 AND Close > Pivot-55 AND Aroonup > 0 AND RSI > 20 AND MACD > -1 AND NOT Trenddown AND Close = Highest[30] THEN Buy PositionSizeLong Contracts AT MARKET SET TARGET pProfit (Pivot-Close)-5 SET STOP pLOSS 50*Faktor1 ClosetryCount = ClosetryCount +1 ENDIF ENDIF IF ((TIME >= 085400) AND (TIME <= 085500)) AND TradeON AND TradeDay THEN IF NOT Forbiddenshort AND NOT OnMarket AND Close > Pivot+8 AND Close < Pivot+100 AND Aroondown > 10 AND RSI < 75 AND MACD < 2 AND Close < Average[200] AND Close < Average[10] AND NOT Trendup AND Close < Supertrend THEN Sellshort PositionSizeShort Contracts AT MARKET SET TARGET pProfit (Close-Pivot)-5 SET STOP pLOSS 50*Faktor1 ClosetryCount = ClosetryCount +1 ENDIF IF Not Forbiddenlong AND NOT OnMarket AND Close < Pivot+8 AND Close > Pivot-55 AND Aroonup > 10 AND RSI > 20 AND MACD > -1 AND Close > Average[200] AND CLose > Average[1000] THEN Buy PositionSizeLong Contracts AT MARKET SET TARGET pProfit (Pivot-Close)-5 SET STOP pLOSS 50*Faktor1 ClosetryCount = ClosetryCount +1 ENDIF ENDIF IF ((TIME >= 092500) AND (TIME <= 093500)) AND TradeON AND TradeDay THEN IF NOT Forbiddenshort AND NOT OnMarket AND Close > Pivot+8 AND Close < Pivot+100 AND Aroondown > 20 AND RSI < 70 AND MACD < 1 AND Close < Average[200] AND Average[50] < Average[100] AND Average[100] < Average[200] AND Close < Average[10000] AND Overboth AND Close = Lowest[90] THEN Sellshort PositionSizeShort Contracts AT MARKET SET TARGET pProfit (Close-Pivot)-5 SET STOP pTrailing 100*Faktor1 ClosetryCount = ClosetryCount +1 ENDIF IF Not Forbiddenlong AND NOT Onmarket AND Close < Pivot+8 AND Close > Pivot-100 AND Aroonup > 20 AND RSI > 25 AND MACD > 0 AND Close > Average[200] AND Average[50] > Average[200] AND Average[100] > Average[200] AND Close < XetraClose AND Underboth AND Close = Highest[90] THEN Buy PositionSizeLong Contracts AT MARKET SET TARGET pProfit (Pivot-Close)-5 SET STOP pTrailing 100*Faktor1 ClosetryCount = ClosetryCount +1 ENDIF ENDIF IF (TIME >= 080000 AND TIME <= 113000) AND Tradeon AND Tradeday THEN IF NOT ForbiddenShort AND Not Onmarket AND Overboth AND Reachedboth = 0 AND (Close > Average[4500]) AND (Close > Average[100]) AND (Close > Average[1000]) AND ((Average[2500] > Average[1000]) OR (Average[4500] > Average[2500]) OR (Average[4500] > Average[1000])) AND Aroondown > 5 AND RSI < 75 AND MACD < 2 AND Close < Highest[600] AND Close < Close[1] AND Close < Supertrend THEN Sellshort PositionSizeShort Contracts AT MARKET ClosetryCount = ClosetryCount +1 IF Close > DayClose+10 AND DayClose > (max(Pivot,XetraClose)) THEN SET TARGET pProfit (Close - DayClose)-5 ELSE SET TARGET pProfit (Close-min(min(DayClose,XetraClose),Pivot))-5 ENDIF SET STOP pTrailing 220*Faktor1 ELSIF NOT ForbiddenShort AND Not Onmarket AND Reachedboth = 0 AND (Close > Average[100]) AND (Close < Average[1000]) AND (Average[2500] < Average[1000]-15) AND (Average[4500] < Average[2500]) AND Aroondown > 5 AND RSI < 75 AND MACD < 2 AND Close < Highest[600] AND NOT Trendup AND Close < Close[1] AND Close < Supertrend THEN Sellshort PositionSizeShort Contracts AT MARKET ClosetryCount = ClosetryCount +1 IF Close > DayClose+10 AND DayClose > (max(Pivot,XetraClose)) THEN SET TARGET pProfit (Close - DayClose)-5 ELSE SET TARGET pProfit (Close-max(max(DayClose,XetraClose),Pivot))-5 ENDIF SET STOP pTrailing 170*Faktor1 ELSIF NOT ForbiddenLong AND NOT OnMarket AND Underboth AND Reachedboth = 0 AND ((Close < Average[4500]) AND Close < Average[100]) AND ((Average[2500] < Average[1000]) OR (Average[4500] < Average[2500]) OR (Average[4500] < Average[1000])) AND Aroonup > 15 AND RSI > 20 AND RSI < 75 AND Close > Close[1] AND Close > Supertrend THEN Buy PositionSizeLong Contracts AT MARKET ClosetryCount = ClosetryCount +1 IF Close < DayClose-10 AND DayClose < (min(XetraClose,Pivot)) THEN SET TARGET pProfit (DayClose-Close)-5 ELSE SET TARGET pProfit (max(max(DayClose,XetraClose),Pivot)-Close)-5 ENDIF SET STOP pTrailing 170*Faktor1 ELSIF NOT ForbiddenLOng AND NOT OnMarket AND Underboth AND Reachedboth = 0 AND ((Close > Average[4500]) AND Close > Average[100]) AND ((Average[2500] > Average[1000]) AND (Average[4500] < Average[2500]) AND (Average[4500] < Average[1000])) AND Aroonup > 5 AND RSI > 20 AND MACD > -5 AND NOT Trenddown AND RSI < 75 AND Close > Close[1] AND Close > Supertrend THEN Buy PositionSizeLong Contracts AT MARKET ClosetryCount = ClosetryCount +1 IF Close < DayClose-10 AND DayClose < (min(XetraClose,Pivot)) THEN SET TARGET pProfit (DayClose-Close)-5 ELSE SET TARGET pProfit (max(XetraClose,Pivot)-Close)-5 ENDIF SET STOP pTrailing 170*Faktor1 ELSIF NOT ForbiddenLong AND NOT OnMarket AND Underboth AND Reachedboth = 0 AND ((Average[2500] > Average[1000]) OR (Average[4500] > Average[2500]) OR (Average[4500] > Average[1000])) AND Close > Average[100] AND Average[200] > Average[1000] AND Aroonup > 5 AND RSI > 20 AND MACD > -5 AND NOT Trenddown AND RSI < 75 AND Close > Close[1] AND Close > Supertrend THEN Buy PositionSizeLong Contracts AT MARKET ClosetryCount = ClosetryCount +1 IF Close < DayClose-10 AND DayClose < (min(XetraClose,Pivot)) THEN SET TARGET pProfit (DayClose-Close)-5 ELSE SET TARGET pProfit (max(XetraClose,Pivot)-Close)-5 ENDIF SET STOP pTrailing 170*Faktor1 ELSIF NOT ForbiddenLong AND NOT OnMarket AND Underboth AND Reachedboth = 0 AND ((Average[2500] > Average[1000]) AND (Average[4500] > Average[2500]) AND (Average[1000] > Average[200]) AND Average[200] > Average[100]) AND Close > Average[100] AND Aroonup > 5 AND RSI > 20 AND MACD > -2 AND RSI < 75 AND Close > Close[1] AND Close > Supertrend THEN Buy PositionSizeLong Contracts AT MARKET ClosetryCount = ClosetryCount +1 IF Close < DayClose-10 AND DayClose < (min(XetraClose,Pivot)) THEN SET TARGET pProfit (DayClose-Close)-5 ELSE SET TARGET pProfit (max(XetraClose,Pivot)-Close)-5 ENDIF SET STOP pTrailing 200*Faktor1 ENDIF ENDIF ENDIF //*************************************************************************// //Tagesschluss Rallye und Down M/W/D: o/o/o // //*************************************************************************// //up IF Time >= 164500 AND Time <= 173000 AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenLong AND Close => hi THEN IF Close > (Pivot) THEN IF RSI > 20 AND MACD > -2 AND Close > Average[100] AND AroonUp > 5 AND MA20over AND Close < Highest[840] THEN BUY PositionsizeLong CONTRACTS AT MARKET SET STOP pLOSS 60*Faktor1 ENDIF ELSIF Close < Pivot AND RSI > 20 AND MACD > -2 AND Close > Average[100] AND AroonUp > 0 AND MA20over AND Average[50] > Average[100] THEN BUY PositionsizeLong CONTRACTS AT MARKET SET STOP pLOSS 60*Faktor1 ENDIF ENDIF IF Time >= 175000 AND Time <= 210000 AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenLong AND Close => hi THEN IF Close < (Pivot) THEN IF RSI > 20 AND MACD > -2 AND Close > Average[100] AND Average[100] > Average[200] AND Average[200] < Average[1000] AND Average[1000] < Average[2500] AND Average[2500] < Average[4500] AND AroonUp > 0 AND MA20over THEN BUY PositionsizeLong CONTRACTS AT MARKET SET STOP pLOSS 60*Faktor1 ENDIF ENDIF ENDIF //down IF (Time >= 164500 AND Time <= 173000) AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenShort AND Close <= lo THEN IF Close < (Pivot) THEN IF RSI < 85 AND MACD < 2 AND Close < Average[50] AND AroonDown > 5 AND MA20under THEN SellShort PositionsizeShort CONTRACTS AT MARKET SET STOP pLOSS 60*Faktor1 ENDIF ENDIF ENDIF IF Opendayofweek = 5 AND (Time >= 175000 AND Time <= 184500) AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenShort AND Close <= lo THEN IF Close > Pivot AND RSI < 25 AND MACD < -2 AND Close < Average[20] AND Close < Average[50] AND AroonDown > 5 AND Close < Average[100] THEN SellShort PositionsizeShort CONTRACTS AT MARKET SET STOP pLOSS 60*Faktor1 ENDIF ENDIF IF (Time >= 180000 AND Time <= 190000) AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenShort AND Close <= lo THEN IF Close > Pivot AND NOT ReachedXetra AND RSI < 75 AND MACD < 2 AND Close < Average[50] AND AroonDown > 5 AND MA20under AND Average[100] < Average[200] THEN SellShort PositionsizeShort CONTRACTS AT MARKET SET STOP pLOSS 60*Faktor1 ENDIF ENDIF IF Time >= 180000 AND Time <= 200000 AND TradeDay AND TRADEON AND (hi - lo) > AmplitudeMin AND NOT ONMARKET AND NOT ForbiddenShort AND Close <= lo THEN IF Close > (Pivot) THEN IF RSI < 75 AND MACD < 2 AND Close < Average[100] AND Average[100] < Average[200] AND Average[100] > Average[1000]+25 AND Average[1000] > Average[2500] AND AroonDown > 0 AND MA20under THEN Sellshort PositionsizeShort CONTRACTS AT MARKET SET STOP pLOSS 60*Faktor1 ENDIF ENDIF ENDIF IF Time >= 190000 AND Time <= 215900 AND TradeDay AND TRADEON THEN IF Close > ResR1 AND NOT ONMARKET AND NOT ForbiddenShort AND Close <= lo THEN IF RSI < 75 AND MACD < 2 AND Close < Average[10] AND Average[10] < Average[30] AND Average[100] < Average[200] AND Average[200] > Average[1000] AND MA30under AND AroonDown > 0 THEN Sellshort PositionsizeShort CONTRACTS AT MARKET SET STOP pLOSS 60*Faktor1 ENDIF ELSIF Close < SupS1 AND NOT ONMARKET AND NOT ForbiddenLong AND Close >= hi THEN IF RSI > 25 AND MACD > -2 AND Close > Average[10] AND Average[10] < Average[30] AND MA30over AND Average[100] > Average[200] AND Average[200] < Average[1000] AND AroonUp > 0 THEN Buy PositionsizeLong CONTRACTS AT MARKET SET STOP pLOSS 60*Faktor1 ENDIF ENDIF ENDIF // JahresendRallye IF Time >= 143000 AND Time <= 171500 AND Close > Average[10000] AND Tradeday AND TradeON AND NOT ForbiddenLong AND NOT Trenddown AND NOT ONMARKET AND Close > Close[1] AND RSI > 25 AND RSI < 85 AND Close > Average[10] AND Average[20] > Average[30] AND AroonUp > 5 AND Close = Highest[60] AND Close < ResR3 AND (Close MOD 100) > 20 AND MACDLine < 10 AND Close > Average[1000] THEN BUY PositionSizeLong CONTRACTS AT MARKET SET STOP pTrailing 100*Faktor1 ENDIF // Nachmittagsanstieg IF Time >= 143000 AND Time <= 200000 AND NOT Reachedboth AND Tradeday AND TradeON AND NOT ForbiddenLong AND Trendup AND CurrentMonth < 10 AND NOT ONMARKET AND Close > Close[1] AND RSI > 25 AND RSI < 85 AND Close > Average[10] AND Average[20] > Average[30] AND AroonUp > 5 AND Close = Highest[60] AND (Close MOD 100) > 20 AND MACDLine < 10 AND Close > Average[1000] THEN BUY PositionSizeLong CONTRACTS AT MARKET SET STOP pTrailing 100*Faktor1 ENDIFf1_maik, robertogozzi, Chrisinobi and plbourse thanked this postWow!

pableitor and Stefan Sticker thanked this postSuper…Haben Sie etwas doc darüber?

Stefan Sticker thanked this postJein. Der Code ist Stück für Stück aus Recherche im Forum (Codeschnipsel für Trailing-Stops, MA-Filter etc) gewachsen und bei neuen Erkenntnissen erweitert worden.

Er ist recht modular gehalten und kann mit den Flags am Anfang des Codes zB auf einen gewünschten Zielmarkt gestellt und mit gewünschten Parametern gefüttert werden.

Die einzige Dokumentation dazu ist in den Kommentarzeilen im Code selbst.bertrandpinoy thanked this postMoin, da hast du dir super viel Mühe gemacht. Kannst du in wenigen Worten zusammen fassen was der Code genau machen soll?

Stefan Sticker and Inertia thanked this postDanke, dass du deinen Job teilst Stefan Sticker 🙂

Es wird für viele Leute interessant sein!

Stefan Sticker thanked this postDer Code besteht aus mehreren Modulen, die im Kopf aktiviert/deaktiviert/eingestellt werden können.

Ziel war es, ein modulares, auf unterschiedliche Märkte anpassbares System aus den (meiner Meinung nach) besten Bestandteilen an nützlichen Codesnippets des Forums zusammenzustellen.

er enthält

– einen Header mit den wichtigsten Parametern zu den weiteren Modulen

– eine verbesserte Variante eines Seasonality-Codes (vorbereitet für DJI und DAX) inklusive Jahres-/Monats-/Wochentags/Trend-Anpassung

– einen Strategy-Stop- und Money-Management-Code, der Verluste eindämmt

– einen Robustness-Test-Code für Testzwecke im Backtest

– einen anpassbaren Trailing-Stop-Code mit verschiedenen Parametern

– einen Hexensabbat-Filter, der den Handel an Hexensabbat-Tagen verhindert

– Einen Code, der täglich die Werte für Day-High/Low/Close, XetraClose und letztes offenes XetraClose (XetraCloseOld), Pivot/R1/R2/R3/S1/S2/S3 ermittelt (kann dann im Handelscode verwendet werden)

– ein Code, der anhand der Vortages-Closes einen TrendUp oder Trenddown als Flag ausgibt

– einen Moving-Average-Cluster-FilterCode, der bei Clusterbildung von MAs den Handel verbietet

– einen Code, der Moving-Average-Crossing in Flags ausgibt (nutzbar im Handelscode)

– einen Long/Short-S2/R2-Break-Filter, der den Handel bei Bruch von S2/R2 verbietet oder alternativ erst dann in Gegenrichtung erlaubtnach dem Trailing-Stop-Code folgt der eigentliche Handelscode, der natürlich individuell ausfallen kann.

Die Module können wie schon geschrieben einzeln an/ausgeschaltet werden, so daß der Hauptblock (ohne den Handelscode) praktisch nur kopiert werden muss, dann entsprechend eingestellt auf den Markt, in dem man den (darauf programmierten) Handelscode laufen lassen möchte.

Man muss nicht jedes mal für jeden Markt das Rad neu erfinden, sondern hat die wichtigsten/nützlichsten Codes IMMER direkt am Start bei der Entwicklung.plbourse thanked this postHier steckt verdammt viel Arbeit drin. Und wie ist die Leistung? Hast du Backtestergebnisse? Für meinen Geschmack sind das sehr viele Filter.

Stefan Sticker thanked this postJa, da ist insgesamt etwas mehr als 1 Jahr Recherche, Backtest, Umprogrammierung und Optimierung hineingeflossen. ^^

Ich habe Backtestergebnisse seit Februar 2022.

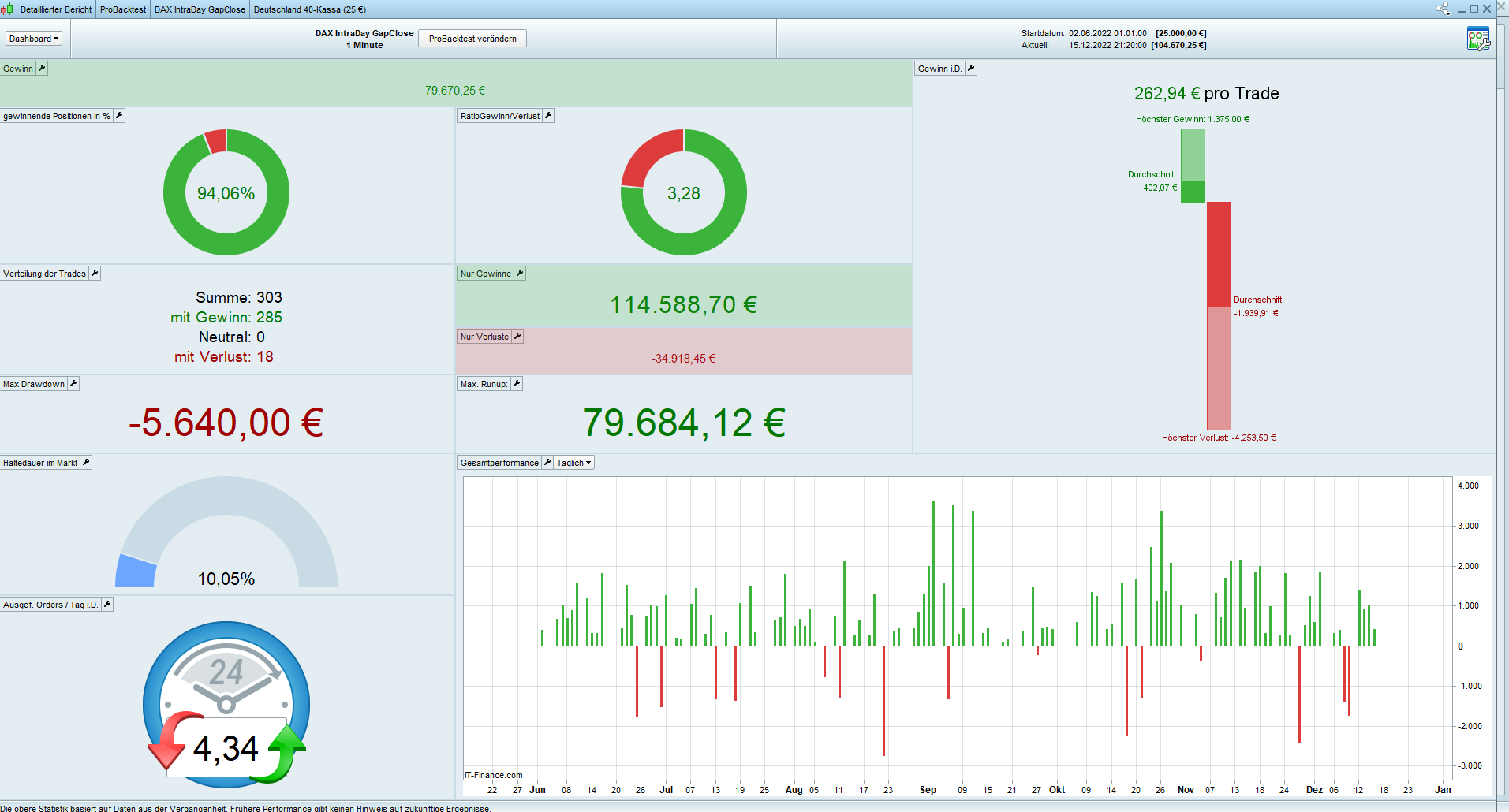

Mein ursprüngliches Mindestziel waren 60% Gewinntrades bei (optimal) Faktor 2/1 Gewinn/Verlust.

Aktuell habe ich konstante 90-95% Gewinn bei Faktor 3-4/1 (je nachdem, ob zB Seasonality-Modifier und/oder Reinvestition von Gewinnen aktiviert werden.

90% hält er sowohl im Rallye-Phasen wie auch im Bärenmarkt.Die Filter im Handelscode sind von mir Stück für Stück bewusst inkludiert, da ein Buy oder Sell nur unter bestimmten Bedingungen stattfinden soll.

Bei 220-240 Trades im Backtest (200.000 Einheiten im Minutenchart) habe ich seitdem so etwa 10-15 Verlusttrades.

Realchart-Läufe sind nicht exakt identisch. Die Ausführung der Orders erfolgt wohl etwas zeitverzögert und verändert dadurch die Ergebnisse.

Auch ist mir aufgefallen, daß Realtrades häufiger in den StopLoss laufen, als im Backtest (Stichwort Spikes/Slipping!).

Ebenfalls kritisch ist zu bemerken, daß ich noch keine sinnvollen Filter für zB Spikes/Downer in hochvolatilem Umfeld (wie aktuell im DJI + DAX zB dank FED/EZB finden konnte.

Ich schätze daher die echte Real-Performance deutlich niedriger und VIELLEICHT so etwa an meiner Zielmarke von 60% / 1,5.Addendum:

die 220-240 Trades beziehen sich jeweils auf den Backtest-Zeitraum von 200.000 Ticks/Minuten (ca 5,5 Monate).

Eine kleine aktuelle Code-Ergänzung im Handelscode:

IF ((TIME >= 092000) AND (TIME <= 100000)) AND TradeON AND TradeDay THEN IF NOT Forbiddenshort AND NOT OnMarket AND Aroondown > 10 AND RSI < 70 AND MACD < 0 AND Close < Average[100] AND Close < Average[50] AND Average[50] < Average[100] AND Average[100] < Average[200] AND Close < Average[10000] AND Close = Lowest[90] THEN

Sellshort PositionSizeShort Contracts AT MARKET

SET STOP pTrailing 100*Faktor1

ENDIF

IF Not Forbiddenlong AND NOT Onmarket AND Aroonup > 10 AND RSI > 25 AND MACD > 0 AND Close > Average[100] AND Close > Average[50] AND Average[50] > Average[200] AND Average[100] > Average[200] AND Close > Average[10000] AND Close = Highest[90] THEN

Buy PositionSizeLong Contracts AT MARKET

SET STOP pTrailing 100*Faktor1

ENDIF

ENDIFDie Ergebnisse im Backtest bei 200.000 Ticks im 1m DAX sind dem angehängten Bild zu entnehmen.

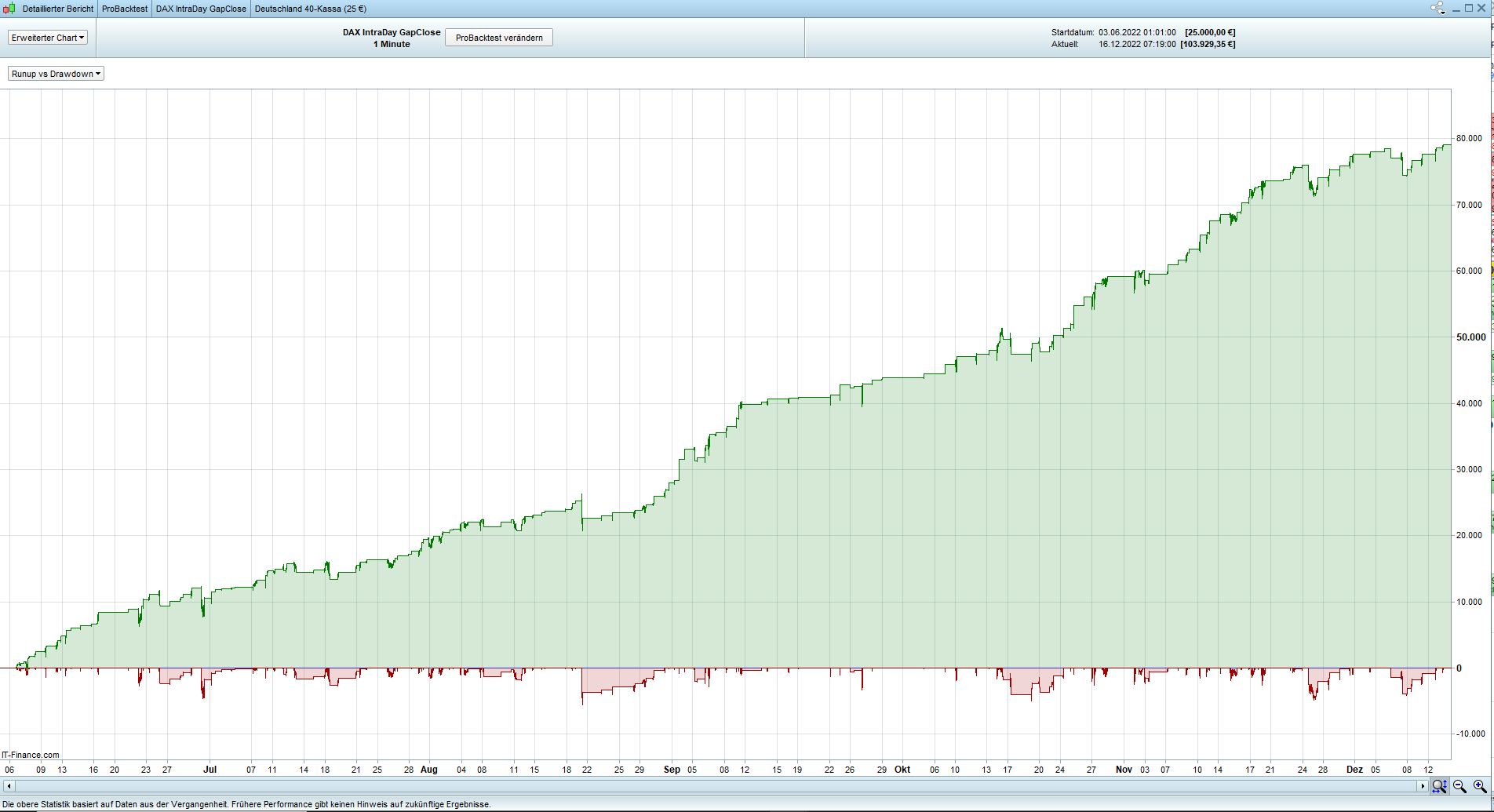

Hast du auch eine Kurve dazu? Mir scheint, der SL ist riesig.

Stefan Sticker thanked this postBitteschön.

Die SL sind vergleichweise weit gewählt und im Trailing-Stop-Code eine Breakeven-Sicherung eingebaut, da der Broker IG, über den ich “fahre” ERKENNBAR UND DEFINITIV versucht, zu eng gesetzte Stops abzufischen. Teilweise absurd starke abrupte Spikes in die Gegenrichtung einer starken Bewegung GENAU IM MOMENT der Plazierung. Ein weiter entfernter Stop macht ihn etwas unerreichbarer (weil dann ja der restliche Markt seinen “Willen” hat!!) und sorgt dafür, daß NUR DIE wirklich ins Minus laufen, die auch wirklich “schlecht” sind. Im Gegenzug ist dieses Minus halt höher, ja.

Ich habe versucht, einen für mich akzeptablen Wert zu finden. Für Dich und Deinen Handelscode kannst Du ja auch andere Stops nehmen.

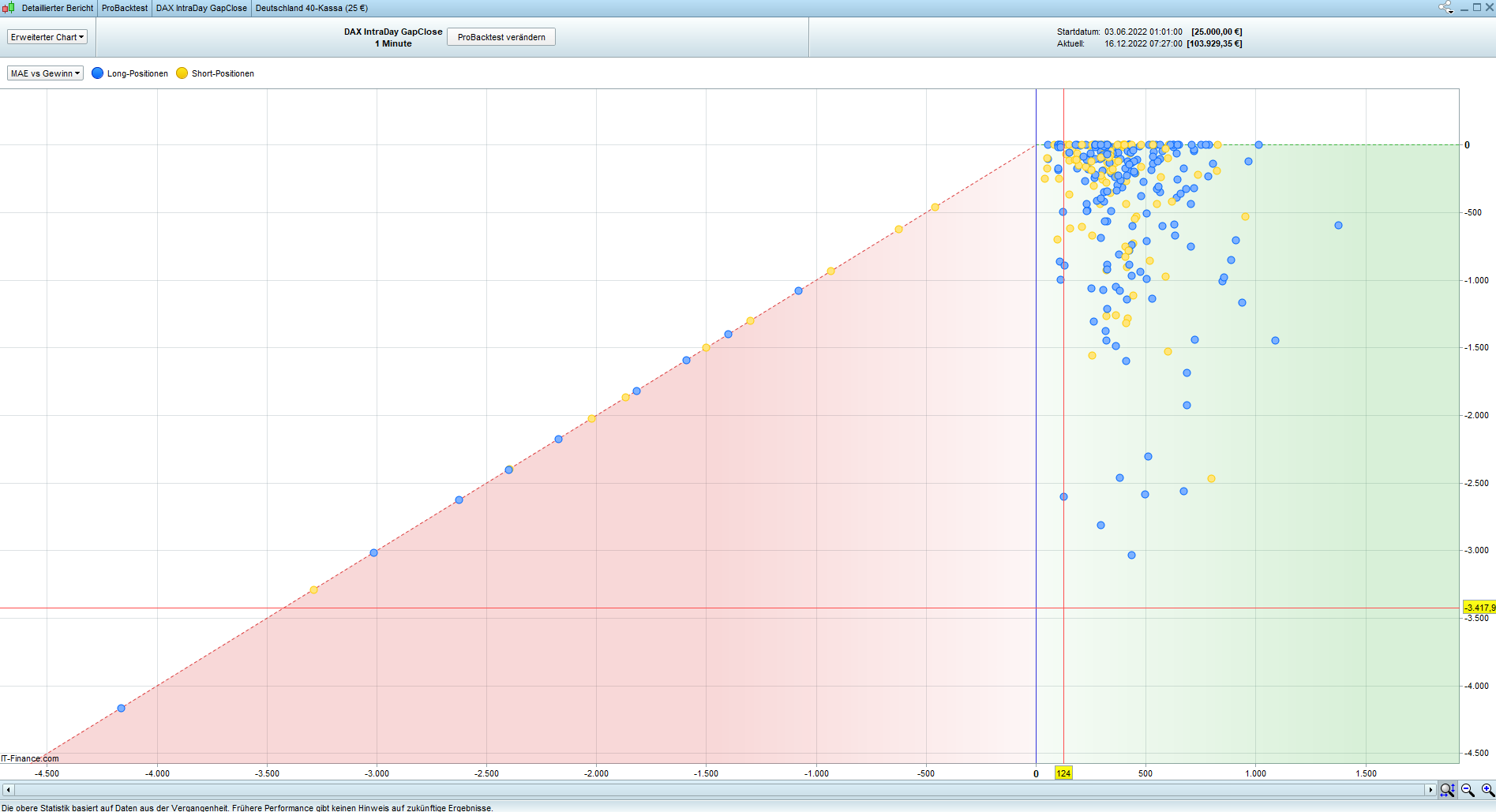

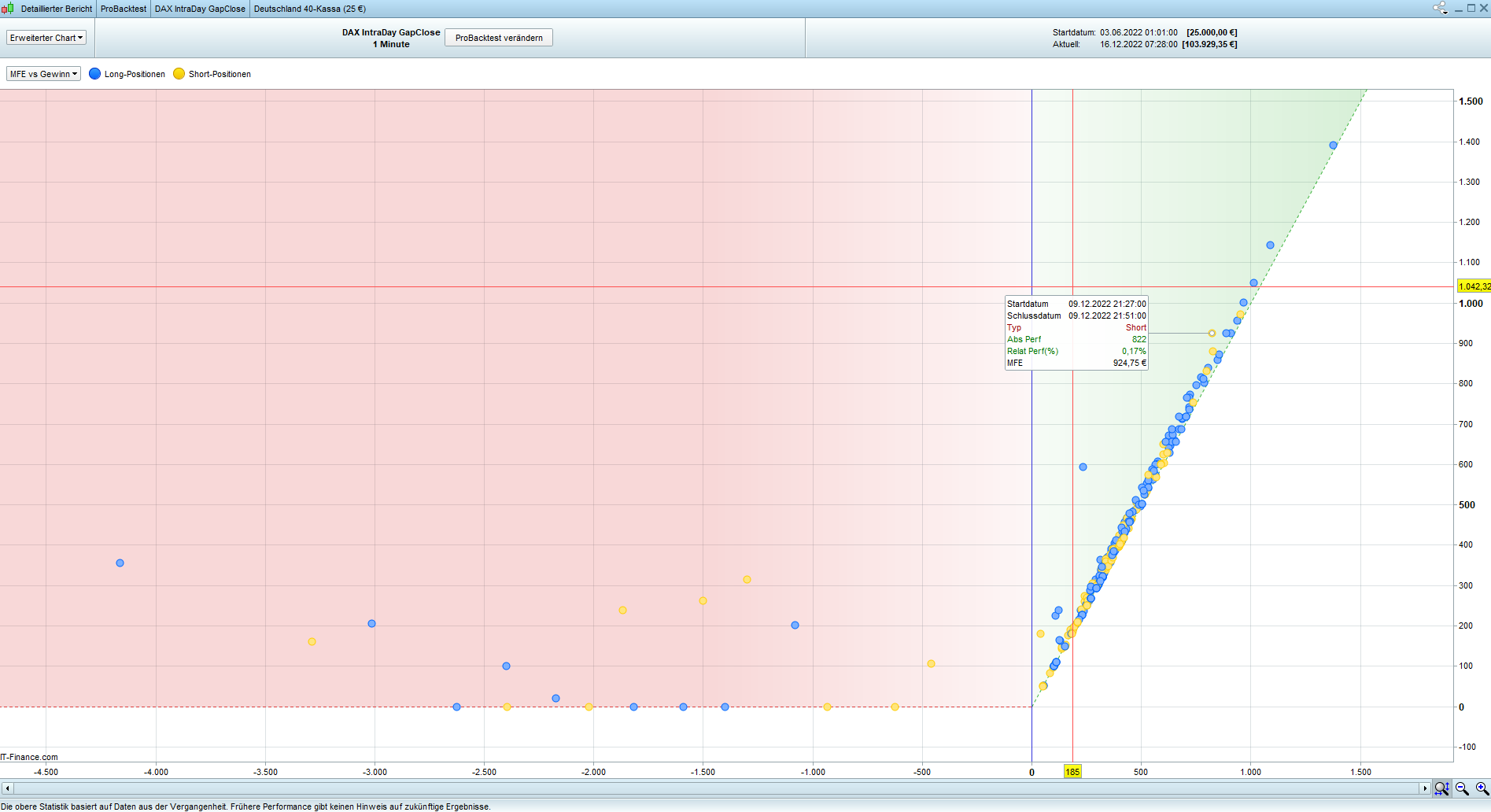

plbourse thanked this postHier noch die MAE und MFE-Tabellen

JohnScher and killerplatuze thanked this post -

AuthorPosts

- You must be logged in to reply to this topic.

Modular Algo System V2.0 inkl. DAX Intraday 1m System

ProOrder: Automatischer Handel & Backtesting

Author

Summary

This topic contains 35 replies,

has 12 voices, and was last updated by ![]() VinzentVega

VinzentVega

1 year, 5 months ago.

Topic Details

| Forum: | ProOrder: Automatischer Handel & Backtesting |

| Language: | German |

| Started: | 12/13/2022 |

| Status: | Active |

| Attachments: | 10 files |

About personal data collected