Hi Grahal, sounds great with coffee and toast 🙂

yes the drag and drop of PRC only exports 1000 rows, even if the backtest has more. Perhaps it not really important if there was 1500 trades over 3 years. But let say DAX from 1992 until now, I had a code that produced 10200 trades. I solved it by chunking the backtest up and exported a 1000 trades at a time, until I reached today date. I was merely just an observation I did.

Cheers Kasper

Bard

BardParticipant

Master

Hi,

Thanks for the great info on this thread.

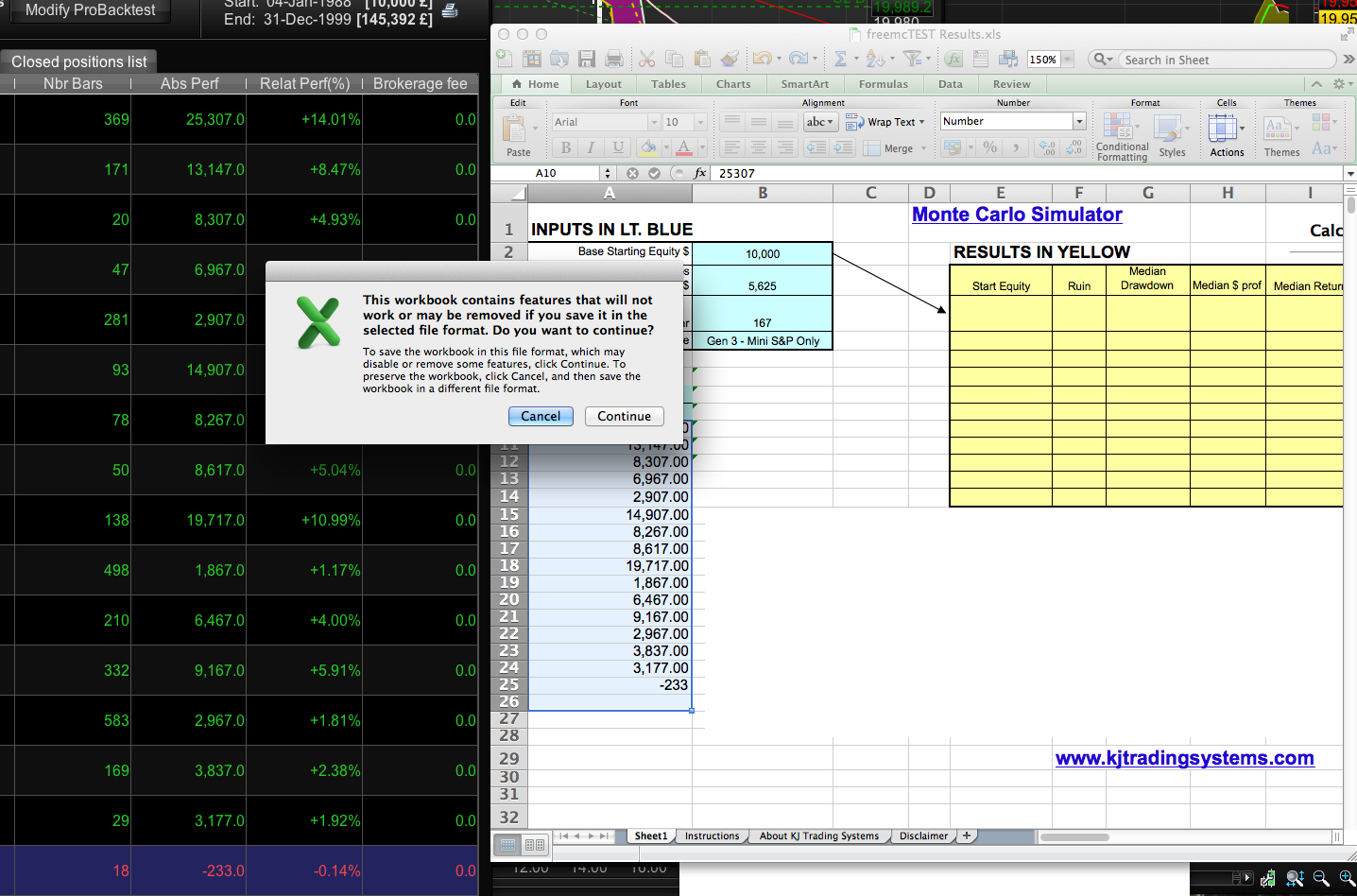

Does anyone know how to get the freeMC Excel sheet to work, i.e. calculate the MC? I hit the yellow calculate button and it freezes? I’ve enabled macros but now it’s asking me to save it as a different file format? Any ideas? Not an Excel fan..

Cheers

Brad

p.s. Not sure how to edit and delete the first image, it’s the second one with 16 trades (it wasn’t the 167 trades that was causing it to freeze)

Hi Bard

Maybe you are trying to save in a different file format than it is already in when you downloaded it. It’s not that you are trying to save it … but maybe you are saving in another version of excel??

Your version is in excel 97-2003 (*.xls) and you may be trying to save in the latest version (*.xlsx)? scroll down until you find 97-2003 in the list of file types. Change the filename when you save anyway then you will still have the old / original version. Hope this helps, if not just say.

Cheers

GraHal

Above is re the error messages not the freezing btw. GraHal

BardParticipant

Master

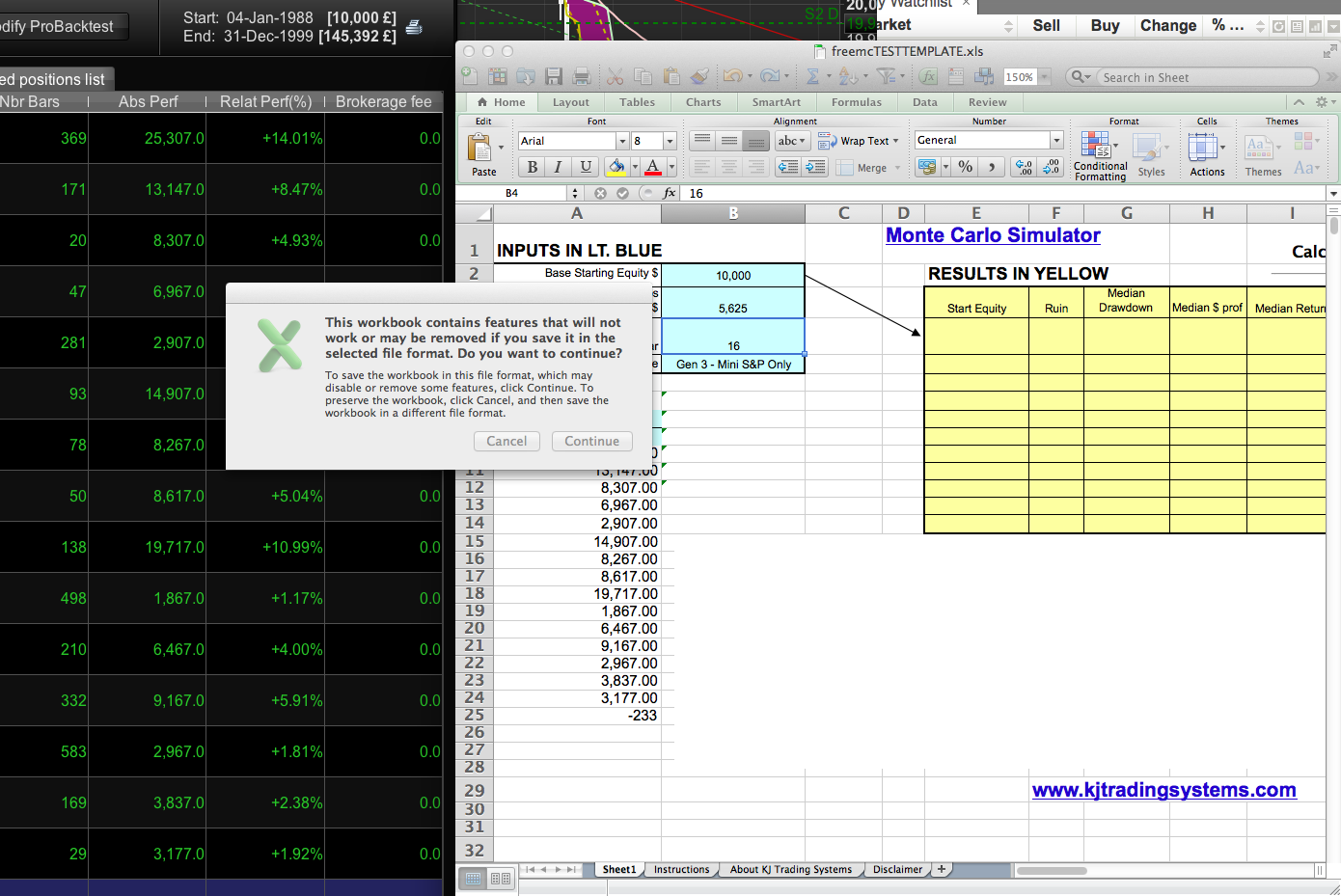

Hi Grahal, thanks for the suggestion. I’m using 2011. I ran a compatibility check and its say there’s no issues? Ha!

It appears to already be default to the 97-2004 version when I click cancel and then go to file/save as?

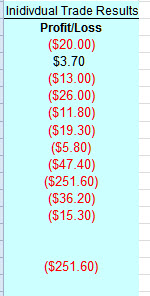

Ive not used it for ages but my results are in the format attached. I notice you have a ‘minus’ in yuors but I cant remember what the format should be 🙂 but I just pressed calculate on mine and it worked / calculated okay. Off to bed now catch you tomorrow if you dont get it sorted?

BardParticipant

Master

Minus signs are okay. It was “hanging” because I didn’t think it would need long with 15 trades. The save issue seems to have resolved to, don’t know why.

The other thing I notice about these results (pls see screenshot) is that the simple system – Ehler Universal Supersmoother Oscillator/bandedge 100 and buy at crossover of -0.8 and sell at a cross under of 0.8 – had a drawdown of 51.4 % although the very first trade taken in the in sample test took the account from £10k to £900 before going on into profit? I lightly optimised the system on 12 years of daily Dow data and the “set it loose” on the £/$ to give these unusual results.

I should point out it didn’t work on the next 12 years (out of sample £/$, even though the 12 years test on the £/$ could be considered as “out of sample”) but it did with alterations to the buy/sell thresholds. Also even on the MC it only gives a median of nearly 30% (with £10k capital)?

I was wondering also do you ever get PRT backtests that show zero drawdown even though the equity curve shows otherwise – again pls see screen?

Glad you got sorted Bard.

Re PRT backtests that show zero drawdown even though the equity curve shows otherwise … yes happens to me all the time. Odd thing is, if you leave the screen sitting there then sometimes the drawdown figure gets populated. Also if you look at the max consecutive losses (in your screen shot it says 1) then there must be a drawdown it just not populated. If after say 2 – 3 mins the download doesnt not get populated I put it down to Server timeout??

Cheers

GraHal

I just want to add some info on monte carlo analysis. A mistake I often see people making is using insample trades for the monte carlo simulation. This is not the way to go and gives overly optimistic results. It is important to only use the OOS-trades of a WFA for the monte carlo.

Another thing to keep in mind when using KJ’s MC simulator is that it also is important to adapt the quantity of when to stop trading correctly. I saw here in the thread a picture where somebody set the amount to when stop trading to 6 USD. This will not yield reasonable results. The absolute lowest value reasonable to have for when to stop trading is the margin requirement of the asset in the test.

Or maybe even more easy to understand.

Running a MC with the results of an old fashioned backtest (no WFA) that is optimized over all history is rather pointless because also the results of a MC done with curve fitted trades will also only show some fantasy results.

I get the zero drawdown thing all the time. Just click on the spanner on the equity line chart and click detailed report and suddenly you get the correct information. Frustrating but I’ve done it so often now it feels like the normal way to get results now!

Hi!

Any sweet soul that known where i can buy or download a good MC with graphs and all simulation values? KJ´s is the best ive found but im missing some graphs and resultvalues.

Best Regards and thank you in advance!

Henrik

Jan

JanParticipant

Veteran

Hallo Grahal and others,

The Monte Carlo Excel simulation, provided by Kevin Davey of kjtradingsystems.com, used VBA poorly, was slow. . . . I made a fast version.

Please find attached the updated fast version. (Advice: save the Excel-file as an Excel macro enabled workbook, for use in the latest Excel version, to let the macros work and save file space. I had to use the Excel 97-2003 XLS format to attach the file, XLSM format not allowed)

The spreadsheet speaks for itself, the blue cells are to be filled with data, or could be modified, you can press the button ” Calculate !” as many times as you like, you will get slightly different results each time. I advise to use 5.000 iterations.

New is also that all iterations are stored and can be seen at column Q till column CO. The more iterations, the more data-rows will be shown at those columns. The previous data will be overwritten by every new simulation.

For a further explanation of the spreadsheet, look at the second worksheet “Instructions”

Enjoy !

Jan vd Wind

JanParticipant

Veteran

Dear Grahal and others,

in addition to my previous reply including the fast Monte Carlo spreadsheet, some additional explanation: (not sure if this is already known)

In the spreadsheet, The Ruin % (column F) and the Median profitability, the Median Return, the Return/DD and the Probability Results > 0 (columns H until K) are based upon :

the number of trades in 1 full year (cell B4) multiplied by the number of contracts (cell O7)

===> The used variables for the possible outcomes are however based upon all Individual Trade Results ( the complete IS and OOS results from PRT backtest), filled in in colomn A from row 10 downwards. For example if you trade only 2 trades in one full year, and from the backtest, the most negative outcomes from several years are -/-500 and -/-499, the change of Ruin is 0% if the initial capital is more then 1.000 (cell B2) and the Stop trading (cell B3) would be 0

===> The more contracts traded, the more risk on ruin, but also the better Return/DD numbers

Given the above information, be aware to fill cell B4 # Trades in 1 Year and to fill the number of contracts (cell O7)

Kind regards,

Jan

Hi all, i use tickquest monte carlo, free software so why not.. I export all my trades from PRT to excel, i use ctrl+F to change all the ” . ” into ” , ” and this fixes the issue with € infront that fucks it all up. Once that is done i copy-paste all the trades into notebook (txt file) just as pure numbers:

-70

60

40

-90

etc etc etc

and i run the TickQuest monte carlo on that, works fine for me!