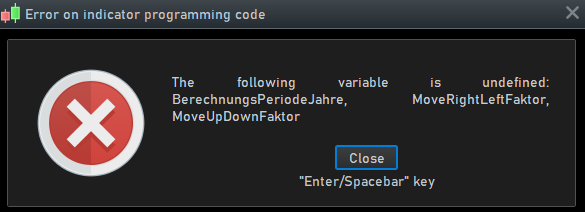

I wonder why my Code is not runnig on a daily chart. Used TF’s are yearly and monthly – to my understandig both multiples of 1 day

I appreciate, if you could check for the reason. Even after hours of testing I was not able to get an idea.

The idea behind is, to perform a performance check on shares and to show the result as text in the chart. The return values are foreseen for usage in a screener.

Only InputValue is “BerechnungsPeriodeJahre” = calculation period in years. Meaning how far the lookback shall be in years.

On yearly basis on a per anno yield is calculated, on monthly basis then other performance values.

defparam DRAWONLASTBARONLY = true

timeframe(yearly)

// Als Startwert für Zuwachs-/PARmax Berechnung wird das höchste historische Close bis zum Beginn der

// Berechnungsperiode gewählt, jedoch max. 5 Jahre zurück

// Dadurch wird ein zu positives Ergebnis wegen eines zwischenzeitlichen, zum Beginn der

// Berechnungsperiode noch nicht beendeten DrawDowns vermieden

lookBack = 5

if islastbarupdate and barindex > lastcalcyearlybarindex then

for y = BerechnungsPeriodeJahre + lookBack downto BerechnungsPeriodeJahre + 1 do

curhighestclose = max(curhighestclose, close[y])

if curhighestclose > prevvalue then

highjahr = year - y

prevvalue = curhighestclose

endif

next

if open[BerechnungsPeriodeJahre] >= curhighestclose then

highjahr = Year[BerechnungsPeriodeJahre]

endif

// Startwerte = Werte am Anfang der Berechnungsperiode

bedopen = open[BerechnungsPeriodeJahre] >= curhighestclose

firstopen = max(open[BerechnungsPeriodeJahre], curhighestclose)

StartJahr = Year[BerechnungsPeriodeJahre]

auswertungszeitraumJ = Year - StartJahr + (days - days[1])/365

lastcalcyearlybarindex = barindex

endif

timeframe(monthly)

BerechnungsPeriodeMonate = round(auswertungszeitraumJ*12)

//// MonatsSchlusskurse speichern

$MClose[barindex] = close

if IsLastBarUpdate then

if barindex > lastcalcmonthlybarindex then

for m = BerechnungsPeriodeMonate downto 0 do

// Datenerfassung für Draw Down Berechnungen

highestOC = max(highestOC, max(close[m], open[m]))

lowestclose = min(close[m], lowestclose)

if (highestOC > prevhighestOC) then

prevhighestOC = highestOC

lowestclose = highestOC

endif

if lowestclose < prevhighestOC then

currDrawDownmax = max(currDrawDownmax, 1 - lowestClose / highestOC)

elsif lowestclose >= prevhighestOC then

GesamtSummeDrawDowns = GesamtSummeDrawDowns + currDrawDownmax

currDrawDownmax = 0

endif

// Datenerfassung für monatliches Verlustrisiko für beendete Monate, zeitliche Gewichtung

// Gewichtungsfaktor: letzter Monat = BerechnungsPeriodeMonate, erster Monat = 1

if m > 0 then

gewichtungsfaktor = BerechnungsPeriodeMonate - m + 1

if close[m] < open[m] then

VerlustMonate = VerlustMonate + 1

sumgewichteterVerlustMonatlich = sumgewichteterVerlustMonatlich + (1 - close[m]/open[m]) * gewichtungsfaktor

sumGewichtungsfaktorVerlust = sumGewichtungsfaktorVerlust + gewichtungsfaktor

endif

else

gewichtungsfaktor = 0

endif

next

//Datenerfassung für variable GewinnKonstanzVarZeitraum

for firstmonth = lastset($MClose) - BerechnungsPeriodeMonate to lastset($MClose) do

for nextmonths = firstmonth + 1 to lastset($MClose) - 1 do

if $MClose[nextmonths] > $MClose[firstmonth] then

GewinnPerioden = GewinnPerioden + 1

endif

AnzahlPerioden = AnzahlPerioden + 1

next

next

// Auf letztem Balken Wert für Summe DD berechnen, auch wenn DD noch nicht beendet ist

if currDrawDownmax > 0 then

GesamtSummeDrawDowns = GesamtSummeDrawDowns + currDrawDownmax

endif

lastcalcmonthlybarindex = barindex

endif //if barindex > lastcalcmonthlybarindex

// VERLUSTRISIKO MONATLICHER ZEITRAUM

// Häufigkeit mit der eine Anlage zu Monatsbeginn mit einer Anlagedauer von 1 Monat im

// Betrachtungszeitraum zu einem negativen Ergebnis geführt hätte

monatlicheVerlustwahrscheinlichkeit = VerlustMonate / BerechnungsPeriodeMonate

gewichteterDurchschnittVerlust = sumgewichteterVerlustMonatlich / sumGewichtungsfaktorVerlust

monatlichesVerlustRatio = monatlicheVerlustwahrscheinlichkeit * gewichteterDurchschnittVerlust

// GEWINNKONSTANZ VARIABLER ZEITRAUM

// Häufigkeit, mit der eine monatliche Anlage mit beliebiger Anlagedauer im

// Betrachtungszeitraum zu einem positives Ergebnis geführt hätte

GewinnKonstanzVarZeitraum = GewinnPerioden/AnzahlPerioden

// WERTZUWACHS

///////////////////////////////////////////////////////////////

highestZuwachs = highestOC/firstopen - 1

currZuwachs = Close/firstopen - 1

// HÖCHSTE PER ANNO RENDITE

// Rendite p.a. = (1 + Wertentwicklung) ^ (365 / Tage) - 1

// PARmax = POW(1 + Zuwachs, potenz) - 1

// y = x ^ p muss wegen PRT Fehler wie folgt codiert werden: y = EXP(p * LOG(x))

///////////////////////////////////////////////////////////////

potenz = 1 / auswertungszeitraumJ

PARmax = exp(potenz * log(1 + highestZuwachs)) - 1

// WAHRSCHEINLICHE PARmax

if (PARmax >= 0) then

WahrscheinlichePARmax = PARmax * GewinnKonstanzVarZeitraum

else

WahrscheinlichePARmax = PARmax / GewinnKonstanzVarZeitraum

endif

// CRV

///////////////////////////////////////////////////////////////

if GesamtSummeDrawDowns > 0 then

CRV = highestZuwachs / GesamtSummeDrawDowns

else

CRV = highestZuwachs

endif

//ALL IN ONE KENNZAHL

RisikoAdjustiertePerformanceKennzahl = WahrscheinlichePARmax * CRV / monatlichesVerlustRatio

// TÄGLICHES HANDELSVOLUMEN IM BETRACHTUNGSZEITRAUM

tagepromonat = 20

avgdailyvolume = summation[BerechnungsPeriodeMonate](volume) / (tagepromonat * BerechnungsPeriodeMonate)

endif // IsLastBarUpdate TF monthly

timeframe(default)

// RUNDUNG FÜR BESSERE DARSTELLUNG

///////////////////////////////////////////////////////////////

currZuwachsvH = round(currZuwachs * 100)

highestZuwachsvH = round(highestZuwachs * 100)

PARmaxvH = round(PARmax * 100)

GewinnKonstanzVarZeitraumrounded = round(GewinnKonstanzVarZeitraum * 100,1)

currDrawDownMaxvH = round(currDrawDownmax * 100)

CRVrounded = round(Max(1, CRV))

WahrscheinlichePARmaxrounded = round(WahrscheinlichePARmax * 100,0)

SummeDrawDownsvH = round(GesamtSummeDrawDowns * 100)

lastcloserounded = round(close * 100) / 100

firstopenrounded = round(firstopen * 100) / 100

highestOCrounded = round(highestOC * 100) / 100

lowestCloserounded = round(lowestClose * 100) / 100

auswertungszeitraumJrounded = round(auswertungszeitraumJ,1)

monatlichesVerlustRatiovH = round(monatlichesVerlustRatio * 100,1)

RisikoAdjustiertePerformanceKennzahlrounded = round(RisikoAdjustiertePerformanceKennzahl/10,1)

avgdailyvolumerounded = round(avgdailyvolume)

// ZUSATZINFORMATIONEN IM INDIKATORCHART ANZEIGEN

///////////////////////////////////////////////////////////////

offsethor = MoveRightLeftFaktor // horizontale Pos. vom Ankerpunkt

offsethorsp2 = offsethor + 175

offsetver = 10 * MoveUpDownFaktor // vertikale Pos. vom Ankerpunkt

step = -22 // Schrittweite vertikale Pos. für verschiedene Zeilen

zeilen = 0

Drawtext("AUSWERTUNGZEITRAUM #auswertungszeitraumJrounded#J ab 01 / #StartJahr#", offsethor+50, offsetver + zeilen * step, SansSerif, Bold, 15) coloured( 72, 118, 255) anchor (left)

zeilen = 1.5 + zeilen

dist = 20

Drawtext("PerformanceKennzahl", offsethor - dist, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(200, 0, 200) anchor (left)

Drawtext("#RisikoAdjustiertePerformanceKennzahlrounded#", offsethorsp2 , offsetver + zeilen * step, SansSerif, Bold, 15) coloured(200, 0, 200) anchor (left)

zeilen = 1.5 + zeilen

Drawtext("PARmax", offsethor - 3 * dist - 10, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(0, 125 ,0) anchor (left)

Drawtext("avg #PARmaxvH# % p.a.", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(0, 125 ,0) anchor (left)

zeilen = 1 + zeilen

Drawtext("GewinnKonstanz langfristig", offsethor - 2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(0, 125 ,0) anchor (left)

Drawtext("#GewinnKonstanzVarZeitraumrounded# %", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(0, 125 ,0) anchor (left)

zeilen = 1 + zeilen

Drawtext("WahrscheinlichePARmax", offsethor - 13, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(0, 125 ,0) anchor (left)

Drawtext("avg #WahrscheinlichePARmaxrounded# % p.a.", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(0, 125 ,0) anchor (left)

zeilen = 1.5 + zeilen

Drawtext("CRV", offsethor - 4 * dist - 4, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(250, 200, 250) anchor (left)

Drawtext("#CRVrounded# ", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(250, 200, 250) anchor (left)

zeilen = 1 + zeilen

Drawtext("VerlustRatio monatl.", offsethor - 1.4 * dist, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(250, 200, 250) anchor (left)

Drawtext("#monatlichesVerlustRatiovH#", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(250, 200, 250) anchor (left)

zeilen = 1.5 + zeilen

Drawtext("last highest Close", offsethor - 1.5 * dist - 6, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(238,59,59) anchor (left)

Drawtext("#highestOCrounded# Pkte", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(238,59,59) anchor (left)

zeilen = 1 + zeilen

Drawtext("last Lowest Close", offsethor - 1.5 * dist - 6, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(238,59,59) anchor (left)

Drawtext("#lowestCloserounded# Pkte", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(238,59,59) anchor (left)

zeilen = 1 + zeilen

Drawtext("curr. DrawDown max.", offsethor - dist - 4, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(238,59,59) anchor (left)

Drawtext("#currDrawDownMaxvH# %", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(238,59,59) anchor (left)

zeilen = 1 + zeilen

Drawtext("Summe DrawDowns", offsethor - dist - 10, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(238,59,59) anchor (left)

Drawtext("#SummeDrawDownsvH# %", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(238,59,59) anchor (left)

zeilen = 1.5 + zeilen

if not bedopen then

Drawtext("First Open = Close #highjahr#", offsethor - 12, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100 , 255) anchor (left)

else

Drawtext("First Open = Open #StartJahr#", offsethor - 12, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100 , 255) anchor (left)

endif

Drawtext("#firstopenrounded# Pkte", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100 , 255) anchor (left)

zeilen = 1 + zeilen

Drawtext("Today Close", offsethor - 2.5 * dist - 7, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100 , 255) anchor (left)

Drawtext("#lastcloserounded# Pkte", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100 , 255) anchor (left)

zeilen = 1 + zeilen

Drawtext("Zuwachs höchster", offsethor - 1.5 * dist - 5, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100, 255) anchor (left)

Drawtext("#highestZuwachsvH# %", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100, 255) anchor (left)

zeilen = 1 + zeilen

Drawtext("Zuwachs akt.", offsethor - 2.5 * dist - 4, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100, 255) anchor (left)

Drawtext("#currZuwachsvH# %", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100, 255) anchor (left)

zeilen = 1 + zeilen

Drawtext("avg. daily Volume", offsethor - 1.5 * dist - 8, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100, 255) anchor (left)

Drawtext("#avgdailyvolumerounded# ", offsethorsp2, offsetver + zeilen * step, SansSerif, Bold, 15) coloured(100, 100, 255) anchor (left)

// AUSGABE DES ERGEBNISSES

///////////////////////////////////////////////////////////////

return RisikoAdjustiertePerformanceKennzahlrounded as "PerformanceKennzahl", highestOC as "highest Close", lowestClose as "lowest Close", close as "last Close", avgdailyvolume as "AVG Daily Volume"