Maz

MazParticipant

Veteran

Hi again,

Found another quirky logic for which I’m not sure on the premise:

For the selling Short (or exiting long) side, we are setting stop losses and targets to stopLossShort and takeProfitShort REGARDLESS of whether we actually took a short trade or not. So in other words we might still be LONG on the market – we tested for contitions to go short but may not have actually placed a short trade – yet nevertheless we reset stop loss and targets to the short set of variables whilst we are still potentially in a long trade.

IF ( s1 AND Time = timeSell ) THEN

// check monthly setup and max position size

IF monthlyMultiplierShort < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(monthlyMultiplierShort))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(monthlyMultiplierShort) CONTRACT AT MARKET

ENDIF

ELSIF monthlyMultiplierShort <> 0 THEN // this will never occur

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeShort THEN

//SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ELSIF monthlyMultiplierShort = 0 THEN

SELL AT MARKET

ENDIF

// ****** THESE GET TRIGGERED REGARDLESS OF WHETHER WE ARE ACTUALLY LONG OR SHORT ON THE MARKET *****

stopLoss = stopLossShort

takeProfit = takeProfitShort

// NOTE: As per above logic we may not have actually gone short

// ************************************* //

ENDIF

CN

CNParticipant

Senior

What is the difference in result?

MazParticipant

Veteran

…and same goes for the long side – long stops and targets are set regardless of whether we actually look a long or not… ie we may actually be short at the time of setting the stops and targets to the long variables. If you stick a “graph countofShortShares” above the two lines that set the stops for the long you’ll see the conditions where we amended stops for the long side but were actually short and vice versa

// for the long side

graph countOfShortShares // should always be 0??

stopLoss = stopLossLong

takeProfit = takeProfitLong

// ...

// and for the short side

graph countOfLongShares // should always be 0?

stopLoss = stopLossShort

takeProfit = takeProfitShort

MazParticipant

Veteran

Obviously the results are very different with any amendments to any line. I’m unsure what the author intended. But obviously optimizations can be applied upon any form of quirk and still be profitable (or even more profitable) perhaps without realizing. But it’s important to understand the underlining premise and see if the conditional logic matches that premise.

CNParticipant

Senior

Thanks @Maz Awesome as usual

@Reiner, what would you say to the discorvery that Maz did?

Hallo Rainer,

da ich neu bin zuerst einmal herzlichen Dank für die genialen Strategien.

Bin gerade dabei Deinen Navigator Dax 4H zu testen … unfassbar …

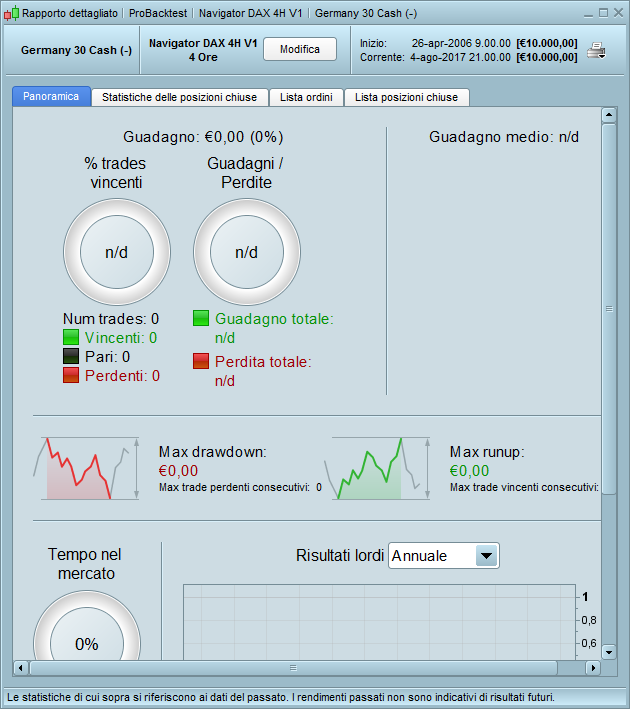

Nur eine wichtige Frage … beim backtest in kleineren Einheiten = 100-1000,

frisst sich die Liquidität auf bzw. hat er extreme Abstürze … bei 200 Einheiten von 80.000€ auf unter 30.000€ … muss ich den SL irgendwie anpassen???

1000 Dank im Voraus

Dominik

Hey Dominik,

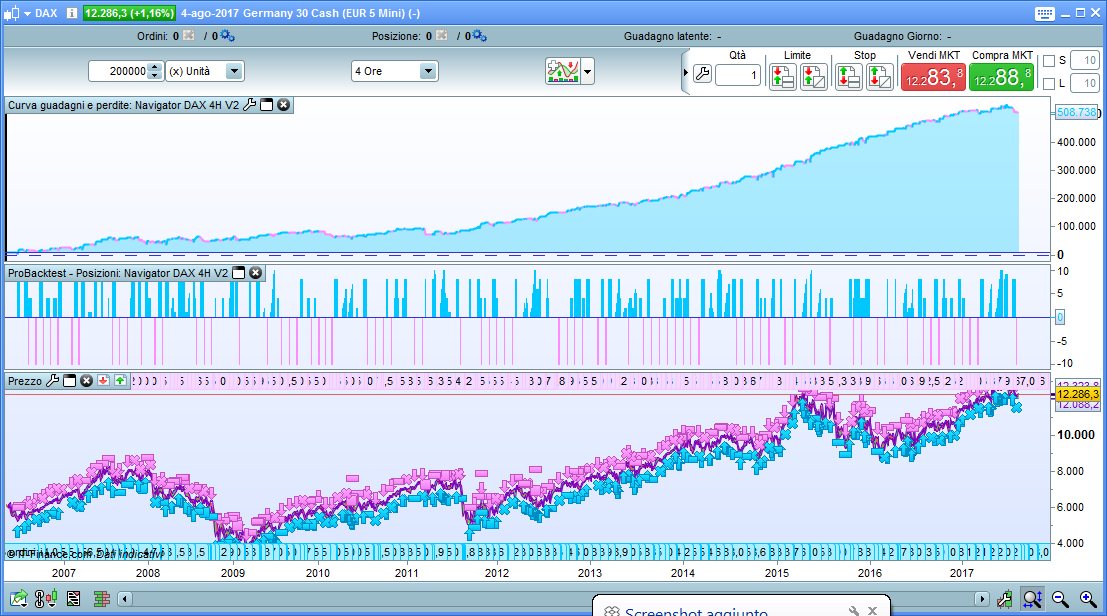

you are using the full Dax CFD Contract. Try the one 1 Euro Mini Contract 😉

Hey flowsen123,

thanxxxs 🙂

Is the a different between Germany 30 Standard and Mini???

It is the same Index??? 😢😊

sunny greeting

dominik

@Dominik

Yes it is the same one, but the Mini is only 1€/point.

Hi team,

I’m just discovering this trading strategy. And I would like to understand if this strategy is running live for someone? (I saw the discussion about backtests showing not so good results..)

I did not understand the last remarks from Maz..Do I need to change the V1 or V2 version before running it in my demo?

Thanks!

I’ve imported the code but it does not seem to work. I do not understand why! Can someone help me?

wp01

wp01Participant

Master

@fepabe,

You should take the mini DAX instead of the normal DAX.

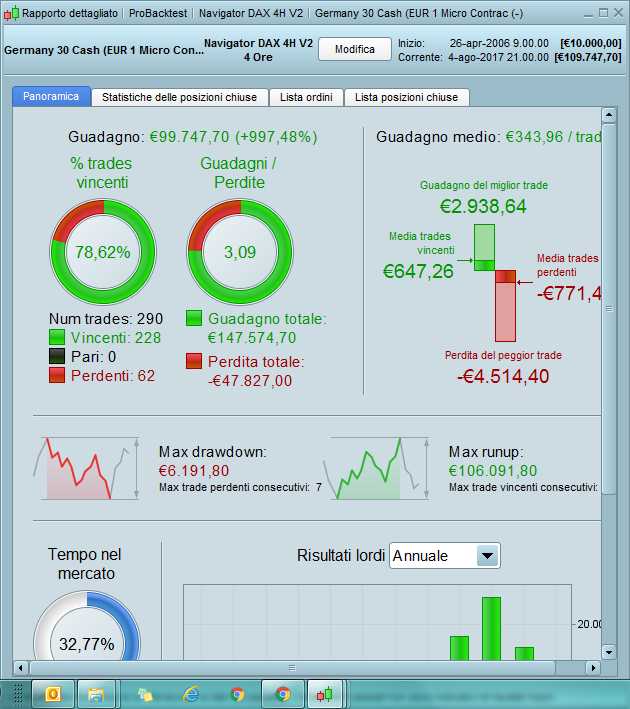

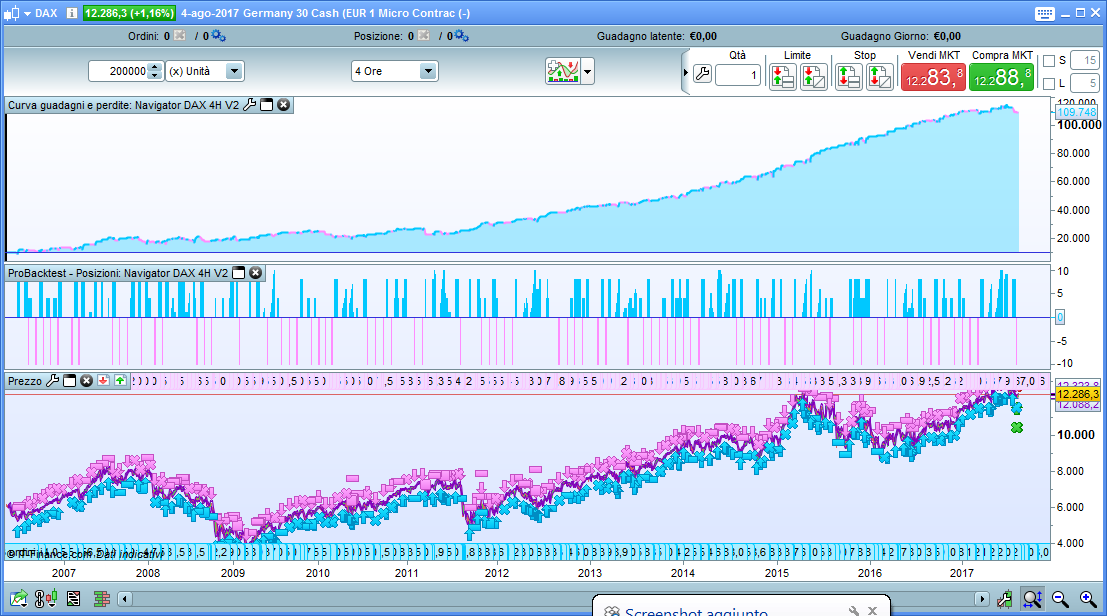

I used the V2 version and it seems to work. The problem is that the results are different from those posted by you. I used the Mini Dax and Micro Dax (5 and 1 euro). I still not understand. The V1 version continues to fail. I find a lot of difference between the “gain of the best trade” and the “loss of worst trade”.

Thanks

Good Morning,

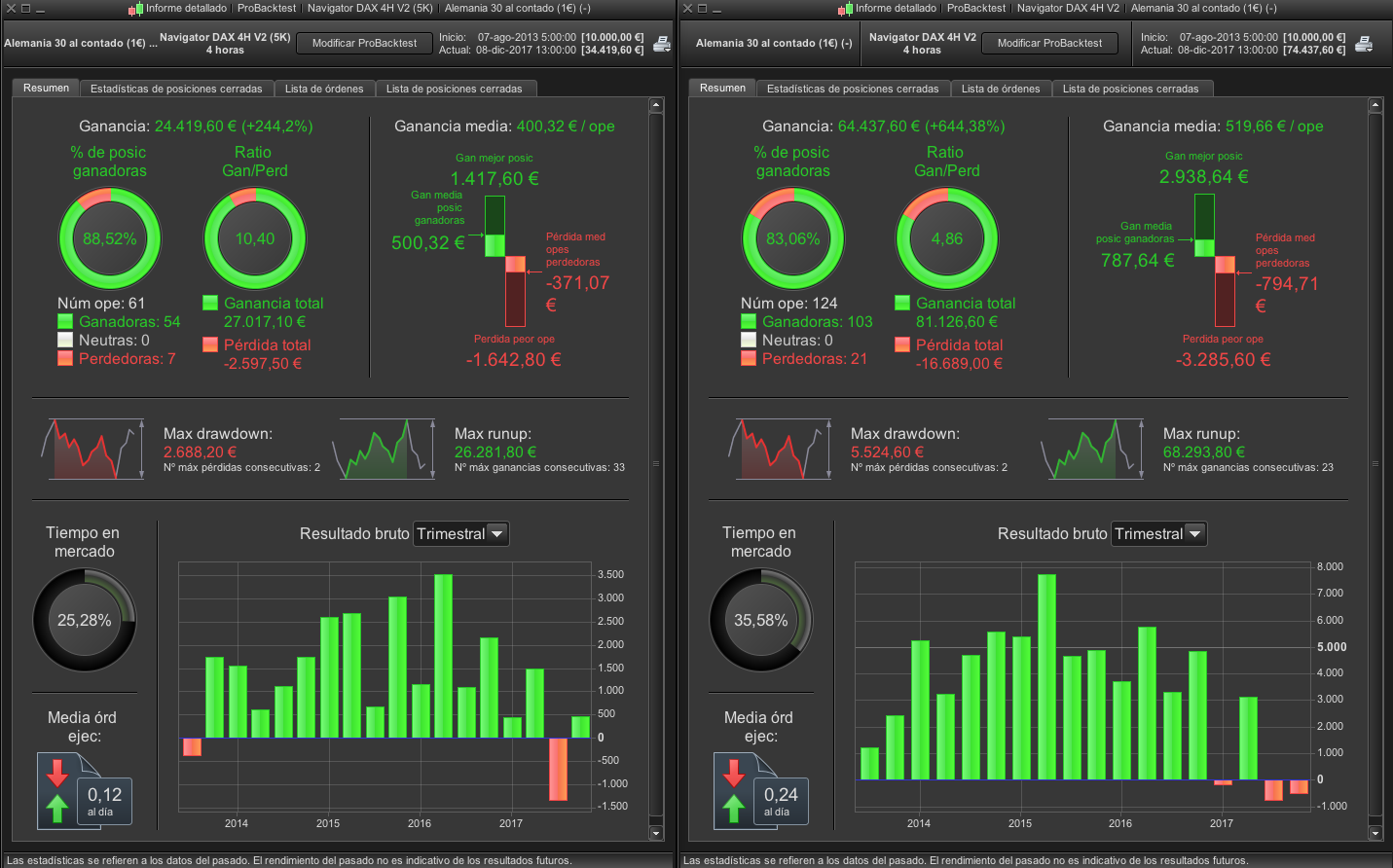

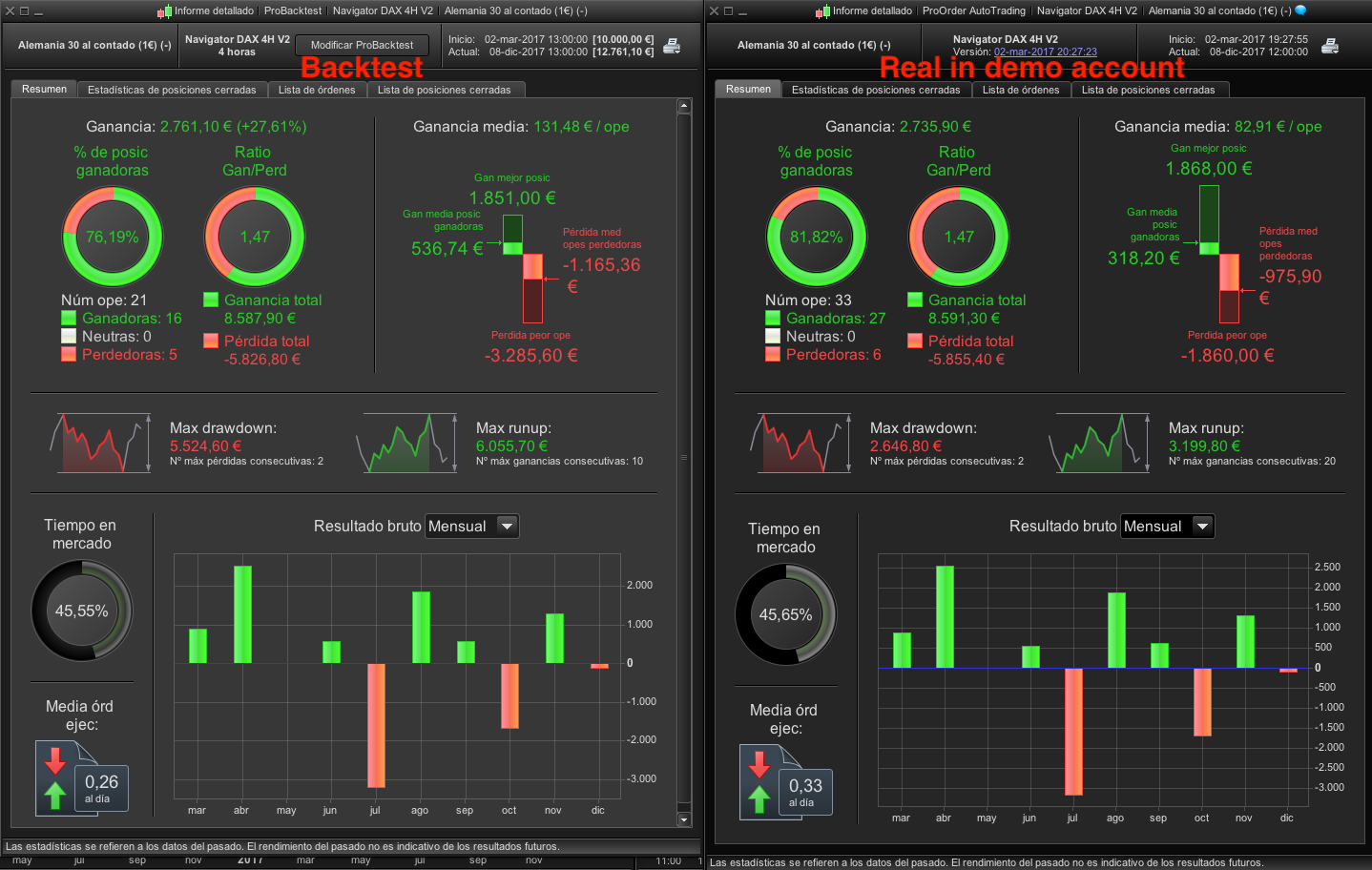

I have been using the V2 version of the Navigator System in the demo account since March and the results do not correspond exactly with the backtest ones. Anyway, the drowndown of V2 is still very high.

I have modified some code parameters to reduce the drowndown and, although it only performs half of operations. I leave the code.

Is someone running it on a real account?

Best regards.

// Navigator DAX 4H V2 (5K)

// Navigator Trading System based on ProRealTime 10.3

// The algo based on the statistical advantage of the TDOM (trading day of the month) idea around the turn of the month

// Version 2

// Instrument: DAX mini 1 EUR, 4H, 9-17 CET, 1 point spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders

// define TDOM days

ONCE tradingDaySell = 20

ONCE tradingDayBuy = 8

// define intraday trading window

ONCE timeSell = 090000

ONCE timeBuy = 170000

// define position and money management parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 4

ONCE maxPositionSizeShort = 4

ONCE minSizeLong = 1

ONCE midSizeLong = 2

ONCE maxSizeLong = 4

ONCE maxSizeShort = -10

ONCE stopLossLong = 8 // in %

ONCE takeProfitLong = 3 // in %

ONCE stopLossShort = 2 // in %

ONCE takeProfitShort = 1.25 // in %

ONCE maxCandlesLongWithProfit = 40

ONCE maxCandlesShortWithProfit = 6

ONCE maxCandlesLongWithoutProfit = 41

ONCE maxCandlesShortWithoutProfit = 13

// define position multiplier for each month (>0 - long / <0 - short / 0 - no trade)

ONCE longJanuary = 0

ONCE shortJanuary = maxSizeShort

ONCE longFebruary = 0

ONCE shortFebruary = maxSizeShort

ONCE longMarch = maxSizeLong

ONCE shortMarch = 0

ONCE longApril = minSizeLong

ONCE shortApril = 0

ONCE longMay = minSizeLong

ONCE shortMay = maxSizeShort

ONCE longJune = minSizeLong

ONCE shortJune = 0

ONCE longJuly = midSizeLong

ONCE shortJuly = maxSizeShort

ONCE longAugust = 0

ONCE shortAugust = maxSizeShort

ONCE longSeptember = 0

ONCE shortSeptember = maxSizeShort

ONCE longOctober = midSizeLong

ONCE shortOctober = maxSizeShort

ONCE longNovember = midSizeLong

ONCE shortNovember = maxSizeShort

ONCE longDecember = midSizeLong

ONCE shortDecember = maxSizeShort

// calculate TDOM

IF Month <> Month[1] THEN

tradingDay = 0

ENDIF

IF Time = 90000 THEN

IF CurrentDayOfWeek > 0 AND CurrentDayOfWeek < 6 THEN

tradingDay = tradingDay + 1

ENDIF

ENDIF

// set montly multiplier

IF CurrentMonth = 1 THEN

monthlyMultiplierLong = longJanuary

monthlyMultiplierShort = shortJanuary

ELSIF CurrentMonth = 2 THEN

monthlyMultiplierLong = longFebruary

monthlyMultiplierShort = shortFebruary

ELSIF CurrentMonth = 3 THEN

monthlyMultiplierLong = longMarch

monthlyMultiplierShort = shortMarch

ELSIF CurrentMonth = 4 THEN

monthlyMultiplierLong = longApril

monthlyMultiplierShort = shortApril

ELSIF CurrentMonth = 5 THEN

monthlyMultiplierLong = longMay

monthlyMultiplierShort = shortMay

ELSIF CurrentMonth = 6 THEN

monthlyMultiplierLong = longJune

monthlyMultiplierShort = shortJune

ELSIF CurrentMonth = 7 THEN

monthlyMultiplierLong = longJuly

monthlyMultiplierShort = shortJuly

ELSIF CurrentMonth = 8 THEN

monthlyMultiplierLong = longAugust

monthlyMultiplierShort = shortAugust

ELSIF CurrentMonth = 9 THEN

monthlyMultiplierLong = longSeptember

monthlyMultiplierShort = shortSeptember

ELSIF CurrentMonth = 10 THEN

monthlyMultiplierLong = longOctober

monthlyMultiplierShort = shortOctober

ELSIF CurrentMonth = 11 THEN

monthlyMultiplierLong = longNovember

monthlyMultiplierShort = shortNovember

ELSIF CurrentMonth = 12 THEN

monthlyMultiplierLong = longDecember

monthlyMultiplierShort = shortDecember

ENDIF

// all in if first day of month is Monday or Thuesday

IF tradingDay = tradingDayBuy AND ( CurrentDayOfWeek = 1 OR CurrentDayOfWeek = 2 ) THEN

monthlyMultiplierLong = maxSizeLong

ENDIF

// caculate current position profit

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

// open long position with order cumulation

l1 = tradingDay = tradingDayBuy

l2 = tradingDay > tradingDayBuy AND posProfit < 0

IF ( (l1 OR l2) AND Time = timeBuy) THEN

// check monthly setup and max position size

IF monthlyMultiplierLong > 0 THEN

IF (COUNTOFPOSITION + (positionSize * monthlyMultiplierLong)) <= maxPositionSizeLong THEN

BUY positionSize * monthlyMultiplierLong CONTRACT AT MARKET

ENDIF

ELSIF monthlyMultiplierLong <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// sell short if valid month or close position only

s1 = tradingDay = tradingDaySell

IF ( s1 AND Time = timeSell ) THEN

// check monthly setup and max position size

IF monthlyMultiplierShort < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(monthlyMultiplierShort))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(monthlyMultiplierShort) CONTRACT AT MARKET

ENDIF

ELSIF monthlyMultiplierShort <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeShort THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ELSIF monthlyMultiplierShort = 0 THEN

SELL AT MARKET

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

numberCandles = (BarIndex - TradeIndex)

m1 = posProfit > 0 AND numberCandles >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND numberCandles >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND numberCandles >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND numberCandles >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit