Hello, jr see that you propose to add a piece of code from Juan in this code proposed by Paul. If you were kind enough to add to Paul’s code. Thank you

N A

startingvalue = 24 //5, 100, 10 boxsize

increment = 3 //5, 20, 10

maxincrement = 3 //5, 10 limit of no of increments either up or down

reps = 3 //1 number of trades to use for analysis //2

maxvalue = 35 //20, 300, 150 //maximum allowed value

minvalue = 20 //5, minimum allowed value

startingvalue2 = 21 //5, 100, 50 stop loss

increment2 = 3 //5, 10

maxincrement2 = 3 //1, 30 limit of no of increments either up/down //4

reps2 = 3 //1, 2 nos of trades to use for analysis //3

maxvalue2 = 35 //20, 300, 200 maximum allowed value

minvalue2 = 20 //5, minimum allowed value

heuristicscyclelimit = 2

once heuristicscycle = 0

once heuristicsalgo1 = 1

once heuristicsalgo2 = 0

if heuristicscycle >= heuristicscyclelimit then

if heuristicsalgo1 = 1 then

heuristicsalgo2 = 1

heuristicsalgo1 = 0

elsif heuristicsalgo2 = 1 then

heuristicsalgo1 = 1

heuristicsalgo2 = 0

endif

heuristicscycle = 0

else

once valuex = startingvalue

once valuey = startingvalue2

endif

if heuristicsalgo1 = 1 then

//heuristics algorithm 1 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise = optimise + 1

endif

once valuex = startingvalue

once pincpos = 1 //positive increment position

once nincpos = 1 //negative increment position

once optimise = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode1 = 1 //switches between negative and positive increments

//once wincountb = 3 //initialize best win count

//graph wincountb coloured (0,0,0) as “wincountb”

//once stratavgb = 4353 //initialize best avg strategy profit

//graph stratavgb coloured (0,0,0) as “stratavgb”

if optimise = reps then

wincounta = 0 //initialize current win count

stratavga = 0 //initialize current avg strategy profit

heuristicscycle = heuristicscycle + 1

for i = 1 to reps do

if positionperf(i) > 0 then

wincounta = wincounta + 1 //increment current wincount

endif

stratavga = stratavga + (((positionperf(i)*countofposition[i]*close)*–1)*–1)

next

stratavga = stratavga/reps //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as “posperf1”

//graph (positionperf(2)*countofposition[2]*100000)*-1 as “posperf2”

//graph stratavga*-1 as “stratavga”

//once besta = 300

//graph besta coloured (0,0,0) as “besta”

if stratavga >= stratavgb then

stratavgb = stratavga //update best strategy profit

besta = valuex

endif

//once bestb = 300

//graph bestb coloured (0,0,0) as “bestb”

if wincounta >= wincountb then

wincountb = wincounta //update best win count

bestb = valuex

endif

if wincounta > wincountb and stratavga > stratavgb then

mode1 = 0

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 1 then

valuex = valuex – (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 1 then

valuex = valuex + (increment*pincpos)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 2 then

valuex = valuex + (increment*pincpos)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 2 then

valuex = valuex – (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

endif

if nincpos > maxincrement or pincpos > maxincrement then

if besta = bestb then

valuex = besta

else

if reps >= 10 then

weightedscore = 10

else

weightedscore = round((reps/100)*100)

endif

valuex = round(((besta*(20–weightedscore)) + (bestb*weightedscore))/20) //lower reps = less weight assigned to win%

endif

nincpos = 1

pincpos = 1

elsif valuex > maxvalue then

valuex = maxvalue

elsif valuex < minvalue then

valuex = minvalue

endif

optimise = 0

endif

// heuristics algorithm 1 end

elsif heuristicsalgo2 = 1 then

// heuristics algorithm 2 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise2 = optimise2 + 1

endif

once valuey = startingvalue2

once pincpos2 = 1 //positive increment position

once nincpos2 = 1 //negative increment position

once optimise2 = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode2 = 1 //switches between negative and positive increments

//once wincountb2 = 3 //initialize best win count

//graph wincountb2 coloured (0,0,0) as “wincountb2”

//once stratavgb2 = 4353 //initialize best avg strategy profit

//graph stratavgb2 coloured (0,0,0) as “stratavgb2”

if optimise2 = reps2 then

wincounta2 = 0 //initialize current win count

stratavga2 = 0 //initialize current avg strategy profit

heuristicscycle = heuristicscycle + 1

for i2 = 1 to reps2 do

if positionperf(i2) > 0 then

wincounta2 = wincounta2 + 1 //increment current wincount

endif

stratavga2 = stratavga2 + (((positionperf(i2)*countofposition[i2]*close)*–1)*–1)

next

stratavga2 = stratavga2/reps2 //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as “posperf1-2”

//graph (positionperf(2)*countofposition[2]*100000)*-1 as “posperf2-2”

//graph stratavga2*-1 as “stratavga2”

//once besta2 = 300

//graph besta2 coloured (0,0,0) as “besta2”

if stratavga2 >= stratavgb2 then

stratavgb2 = stratavga2 //update best strategy profit

besta2 = valuey

endif

//once bestb2 = 300

//graph bestb2 coloured (0,0,0) as “bestb2”

if wincounta2 >= wincountb2 then

wincountb2 = wincounta2 //update best win count

bestb2 = valuey

endif

if wincounta2 > wincountb2 and stratavga2 > stratavgb2 then

mode2 = 0

elsif wincounta2 < wincountb2 and stratavga2 < stratavgb2 and mode2 = 1 then

valuey = valuey – (increment2*nincpos2)

nincpos2 = nincpos2 + 1

mode2 = 2

elsif wincounta2 >= wincountb2 or stratavga2 >= stratavgb2 and mode2 = 1 then

valuey = valuey + (increment2*pincpos2)

pincpos2 = pincpos2 + 1

mode2 = 1

elsif wincounta2 < wincountb2 and stratavga2 < stratavgb2 and mode2 = 2 then

valuey = valuey + (increment2*pincpos2)

pincpos2 = pincpos2 + 1

mode2 = 1

elsif wincounta2 >= wincountb2 or stratavga2 >= stratavgb2 and mode2 = 2 then

valuey = valuey – (increment2*nincpos2)

nincpos2 = nincpos2 + 1

mode2 = 2

endif

if nincpos2 > maxincrement2 or pincpos2 > maxincrement2 then

if besta2 = bestb2 then

valuey = besta2

else

if reps2 >= 10 then

weightedscore2 = 10

else

weightedscore2 = round((reps2/100)*100)

endif

valuey = round(((besta2*(20–weightedscore2)) + (bestb2*weightedscore2))/20) //lower reps = less weight assigned to win%

endif

nincpos2 = 1

pincpos2 = 1

elsif valuey > maxvalue2 then

valuey = maxvalue2

elsif valuey < minvalue2 then

valuey = minvalue2

endif

optimise2 = 0

endif

// heuristics algorithm 2 end

endif

//

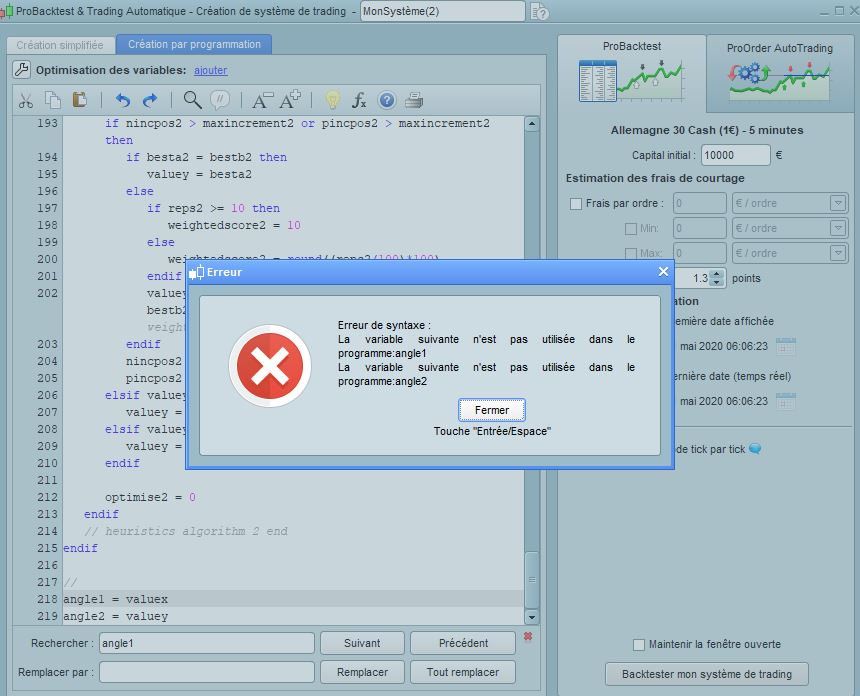

angle1 = valuex

angle2 = valuey