Pieropadova: This is wrong thread, those are the normal Pathfinder, not Swing. But to answer your question you can change the amount of contracts like I show below.

ONCE January1 = 0 //0 ok 1

ONCE January2 = 1 //2 chance

ONCE February1 = 1 //1 ok

ONCE February2 = 0 //0 ok

ONCE March1 = 1 //0 risk(2)

ONCE March2 = 1 //2 chance

ONCE April1 = 1 //3 ok

ONCE April2 = 1 //3 ok

ONCE May1 = 0 //3 ok

ONCE May2 = 0 //0 ok

ONCE June1 = 1 //0 risk(3)

ONCE June2 = 1 //0 risk(2)

ONCE July1 = 1 //1 chance

ONCE July2 = 0 //1 ok

ONCE August1 = 0 // ok

ONCE August2 = 0 // ok

ONCE September1 = 1 //0 risk(3)

ONCE September2 = 1 //0 risk(3)

ONCE October1 = 0 //0 ok

ONCE October2 = 1 //3 ok

ONCE November1 = 1 //0 chance

ONCE November2 = 1 //3 ok

ONCE December1 = 1 //3 ok

ONCE December2 = 1 //2 ok

wp01: Ok, I haven’t tried to optimize with it yet.

wp01

wp01Participant

Master

@CaptainNemo,

The codes you show in your picture are from PF Trading System.

Pathfinder Trading System

But besides that: are you aware of the potential risk you have when all are triggered? The DAX isn’t even a mini but a midi of € 5. To run this you should have at least 100K in your account.

What Despair already said: all contracts are 1 in ProOrder. To run them properly, you should put in 10 or 15 per algo.

Kind regards,

@wp01

Yes, it was supposed to be the 10 future, not 50. For some reason this did not show when I was doing the optimisation.

Yes, it is probably a good idea to start with v3 instead. I guess I need to set all other periods to 0 and start over. It was just easier to continue with v2 🙂

wp01Participant

Master

@dajvop,

It took me already a couple of hours to understand the changes in V3. But that’s fine. Part of a learning proces.

I still have a couple of questions. Still don’t understand the “tradeInPeriod”. When you for example optimize january you see results from other months also popping up when i “comment” this

periods. I guess this should not be happening.

I couldn’t figure it out with the 1 and the 0. So i added at all periods this line and set everything to zero and that also works. Probably not how it is meant by Reiner, but i do not understand

why this line is in January and not in the rest of the months. And if you change line 24 it either works or not.

I also do not understand between what the defaultPeriodMA should be optimized. I try to keep as close to 13. I optimize it somewhere between 2 and 15. I assume 13 was not just for the DAX example,

but for all indices/commodities.

Same is for the signalline. When you have no trades it is at 2 but where should it be between? I used somewhere 20 but i’m not sure if that what it supposed to be.

Regarding maximum candles i try to be as close as the default setting. Longer in a position does not give you always a better result.

And you should keep a close eye on the DD. If you have every period a DD of 1K, you can imagine what it will be multiplied by 24. Not working i guess.

I’m not sure if there is a quick way to optimize, but per instrument it takes a couple of hours for the whole year. But you have to do it only once……until V4, V5 -:)

@wp01

I have moved the code around a bit to make it easier to optimise our 2 week periods.

As I understand it, TradeInPeriod = 0 prevents positions being opened for that period.

defaultPeriodMA is our old PeriodMA which is usually a number between 1-100 and signalline is PeriodThirdMa which as you know is usually 1-10.

Here are PL and S optimised for v3. Please notice that I have moved the original code around a bit to make it easier for us.

wp01Participant

Master

@dajvop,

You’re quick with the adaptions. You seems to be right about the signal line and the periodthirdMA. Weird that i didn’t see the connection. Thanks.

Your PL V2 and V3 on the $10 mini have different results because you used different parameters.

I miei ringraziamenti a tutti gli amici che mi hanno risposto.

Ho scoperto perché i miei pathfinder sono rimasti addormentati per un mese: li ho programmati tutti per il Daily e non per 4H!

Infatti testati per 4H hanno dato dei risultati, anche se non sempre buoni. Ad esempio molto male su FTSE e scarsi su MIB. Il Dax è a circa il 60% di OK, non brillante.

Forse sono da riottimizzare, ma sono talmente tanti i parametri interessati che è ben difficile indovinare quelli giusti.

Per quanto riguarda il rischio, non mi sembra averne, visto che sto testando i sistemi in Paper Trading, quindi con soldi virtuali.

Chi mi spiega la differenza tra un Pathf. Swing e un Path. normale? e dove vanno applicati rispettivamente al meglio?

Siete molto più avanti di me. Bravi.

Grazie a tutti. CptNemo

@CapitanNemo

The difference between Pathfinder Swing and Pathfinder 4h is that here we optimise an instrument for a 2 week period and for commodities and indices. The different Pathfinder 4h algos are already optimised to run all year for different indices, for example DAX, STXE and DOW.

@Patrick

Yes, the results are different, but they are different with the same numbers also. So I have to optimise the v2 algos to fit v3.

Best regards, David

Hello Dajvop,

TX TX TX for the code, i’ll study it. The TS’s seem to do 1 operation each year. It’s correct? They are working daily, before Pathf. worked 4H candles. Did you test others minor times? I’m 73 years old … and I can’t wait 1 year for each transaction! Don’t worry now! I’m touching … wood. I Italy we say someting different.. Bye.

@pieropadova

Yes, the Pathfinder Swing TS are optimised for a 2 week period a time. Yes, they are running on the daily time frame instead of 4h as the original Pathfinder Trading System.

The next period being optimised is for the second half of October. So you will not need to wait 1 year for the next period.

Search this thread for the older algos for the previous periods this year.

Best regards, David

SB and W v3. There is something with the validMaxCandles that prevents the same numbers being applied from v2 to v3… Didn’t even get close to the same results for Wheat…

Hey Guys,

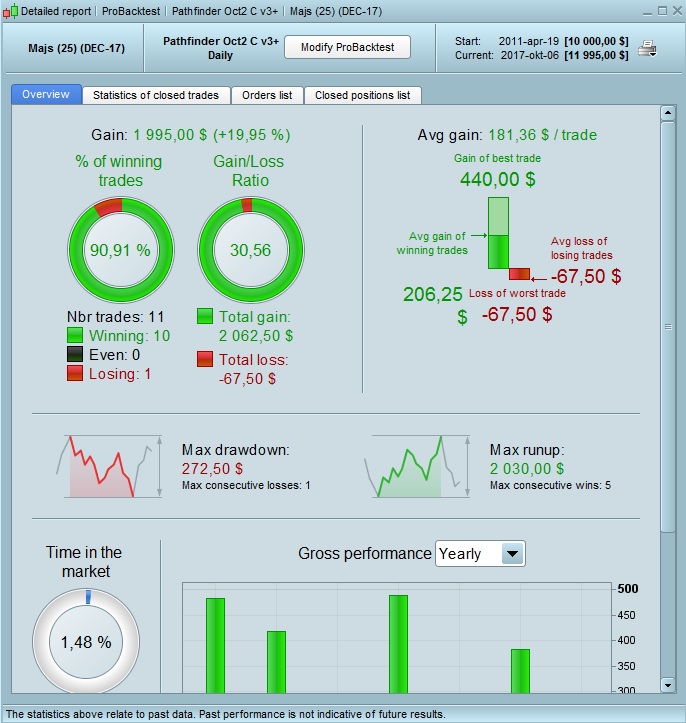

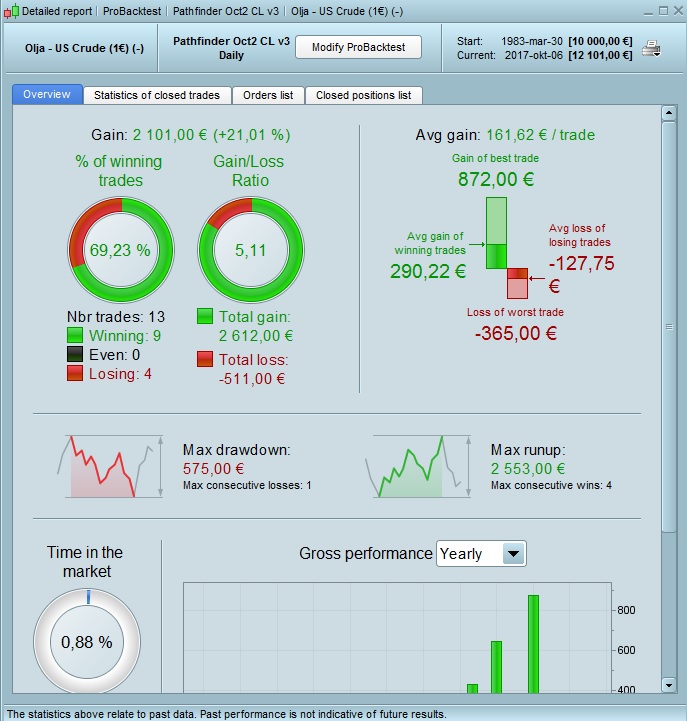

Here my contribution for commodities for Oct2.

I rather stick to the version 2 for now as it seems version 3 is only more suitable for the Full year approach.

CC Short, Gold Short, (Very likely that I wont trade these algos this period)

Crude Long, Copper Short

Best Regards