wp01

wp01Participant

Master

Oskar,

If you want to run them all than 20K is not enough. Actually due to the leverage you only pay partly of the nominal value. Underlying value is much higher

and can easily be between 200K or 400K when you have 15+ systems running. You can find the underlying value on your daily statement. So what happens if

the market is against you and you have several days of huge losses? You blow-up your account.

The BT always start with a starting capital of 10K, AUS$15K or HK$100K. If you want to be relatively safe, take that amount per instrument.

You have to calculate for yourself what you can bear and what won’t keep you awake at night.

wp01: Yes, I think I understood how that works. A DD of 1000 EU would blow up a 10k account, right? Because of the “säkerhetskrav” (margin?) of about 10x…

HG and RB. The latter with high dd.

wp01Participant

Master

@Oskar,

Sorry for the late reply….

I don’t think it is the best way to look at the DD and find out if you are overleveraged. A drawdown says only something of the past and nothing about the future. The DD can be

very low in the BT but can easily twice or tripple the amount of the coming trade.

I’ve also checked the directions in the book from IG what you received when you opened an account. If you look at the part risk- and capitalmanagement (page 17, Dutch version),

you find out that it is recommended by IG to have a maximum leverage of 10:1. This means that you need to have for every €10K of positions €1K of capital.

How will you get the nominal value of your positions? If you check your daily statement of IG you see in the upper left corner the summary of the long and short positions. These positions

are converted to your local currency. You see there that they substracting long and short positions. I would say that you add both long and short positions together to get to your

total exposure. If your total exposure is for example €150K, you need to have at least € 15K of capital if you follow the recommendations of IG.

But this is afterwards of course. Once your positions are opened it is not easy to reduce them without stopping the code. You also do not know how many trades will open until the next period.

But if you want to do it right and keep track of it you need to create an Excel sheet. You fill in the codes you want to activate and what the exposure will be when they all open a position.

The hard part is when will they accumulate? So if you want to play around with €4K you should not activate more codes than the nominal value of € 40K. Or you take a small buffer of one or two

codes because i haven’t had a month that they all opened a position. You have to do what feels right for you of course and where you can live with.

Kind regards,

Patrick

Thanks Patrick! Not sure where the daily statement is but I’ll check. With 5k I should probably have max 2-3 positions up and only 1 contract for each, but ofc depends on which one.

I did it wrong before with to high risk. Corn has 2 positions up already…. Luckily it’s + and I’ve put manual stops for them so I don’t blow up the account.

wp01Participant

Master

I get the statement mailed between 23.00 and 00.00 hours every evening on a workingday. Maybe it is a setting. Can’t remember anymore.

You can view your statement at any time by going in the platform from IG to the right upper corner to “my account”.

Then history followed by statements. There you can choose between current or select a date.

Hi all,

I follow this thread since last march and I also tried some algos. I have a question to ask.

In the beginning the Swing was born to run yearly in different month and only with long trades.

Why don’t we continue to perform a yearly swing that open both short and long trades?

The algo will be more complex but should work every year in both ways.

Is it possible?

Kind regards,

Potto.

wp01Participant

Master

@Potto,

This should be answered by Reiner i think. But V2 can not be used for long and short in the same robot. See his explanation when he released V2 on

page 61 of this forum.

What i can tell you is that there are 24 optimizations per instrument. If you optimize an instrument for one year you have the best result for the whole year.

This does not specific say anything about for example Apr2 or Aug1 or Dec2. All these 24 periods have there own optimization.

I do not know if it is possible to put that in one code. Therefore my knowledge is too little. What i do know is that in the code there are 6 variables and

an addition of the accumulation on/off and a number of contracts (1-3) in the specific period. Beside that there should also be a long and short version.

First there should be 24 optimizations available. We have at least several months to go. After that we have to decide which are good for trading and which not.

If it is technical possible to put that in one code it should be calling in Jan1 the optimizations of that period, in Jan2 the optimizations of that period and that 24 times.

If you name all variables of the same period for example “a” following by “b”. It is going to be a long list and if it works…i have no idea. This can only be answered by

someone with coding-experience.

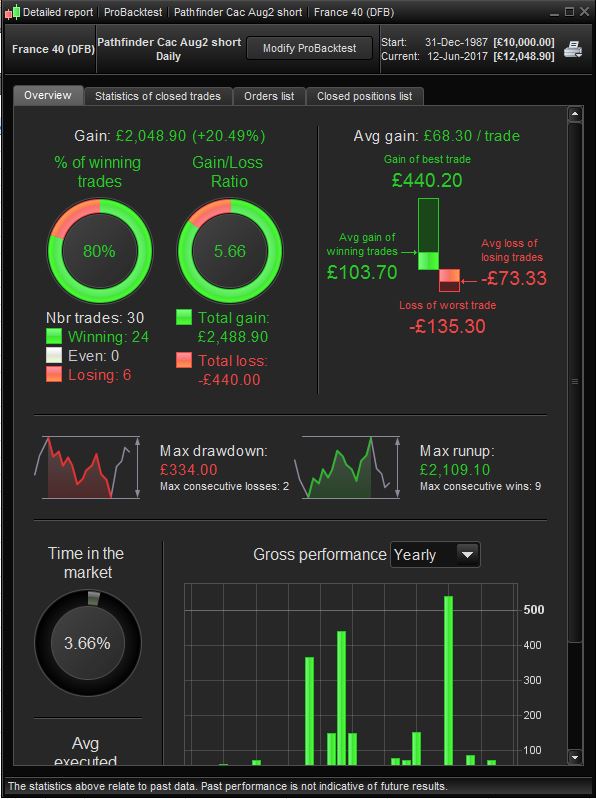

Potto: I think that’s the purpose of the 4h pathfinder algos 🙂

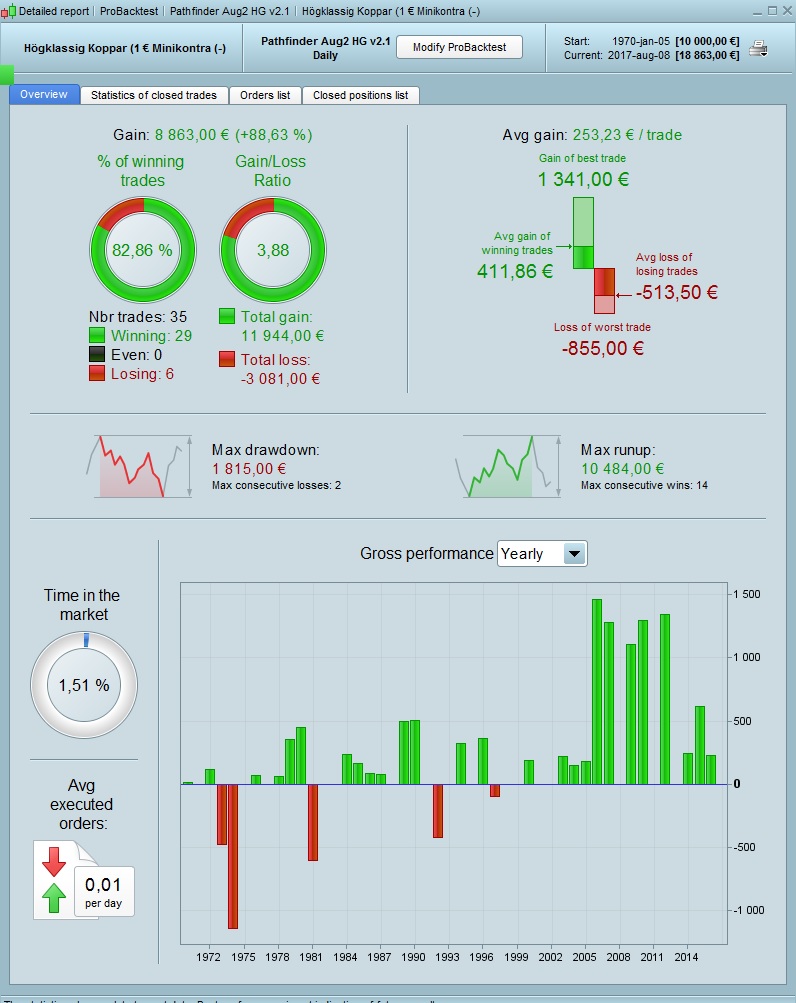

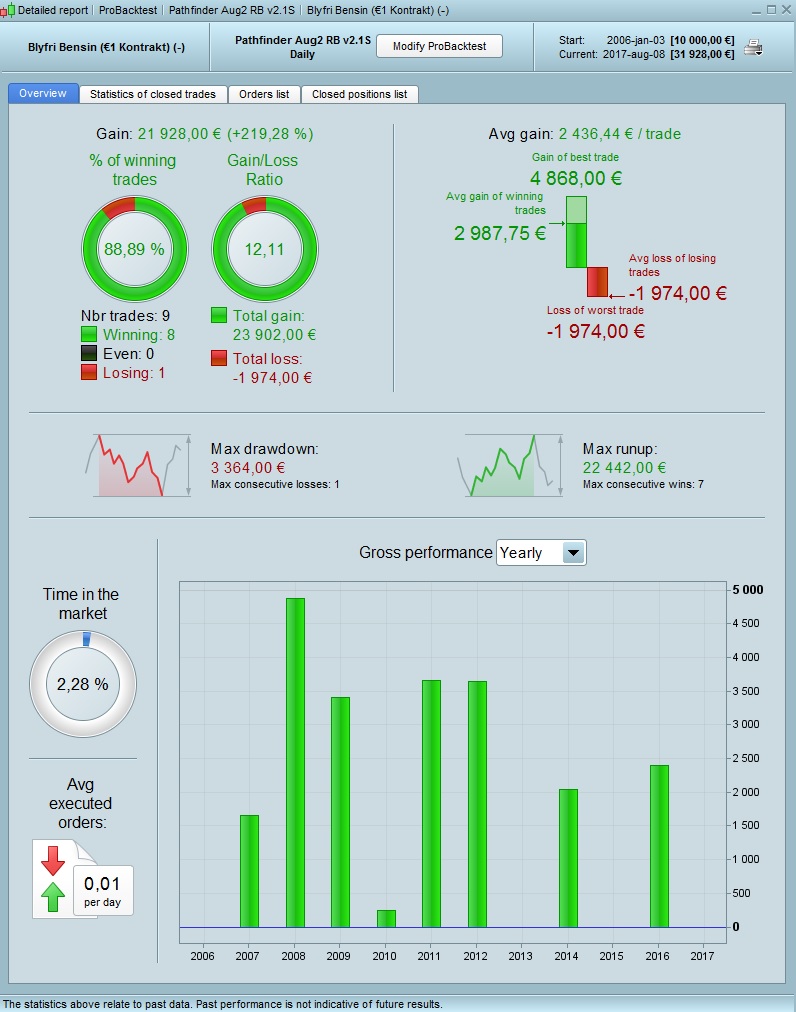

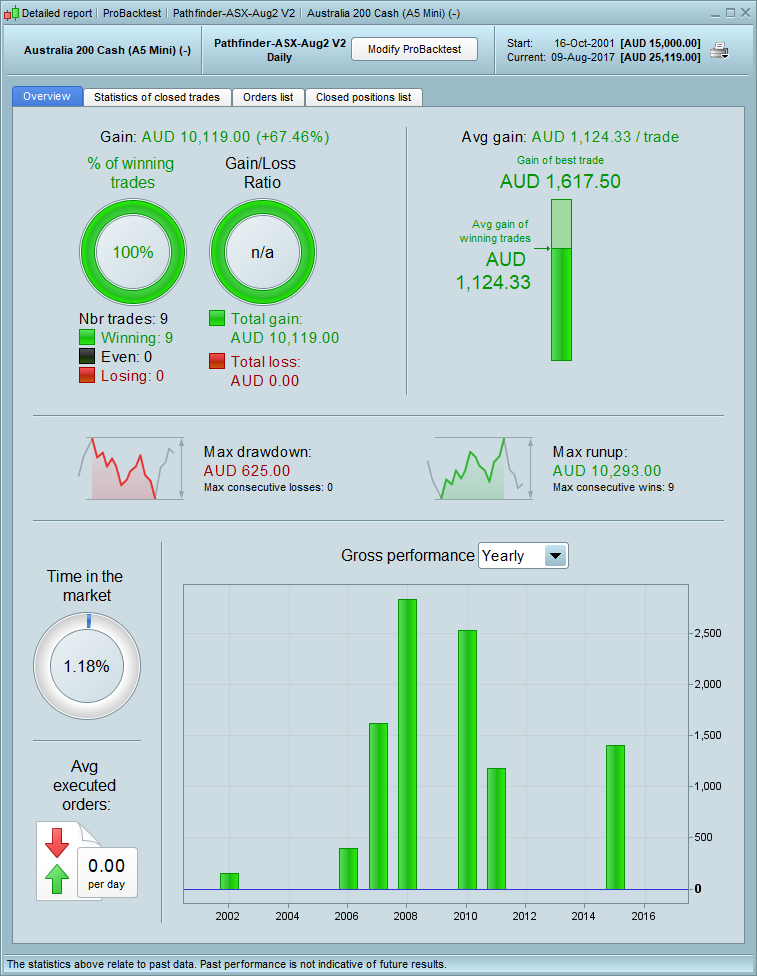

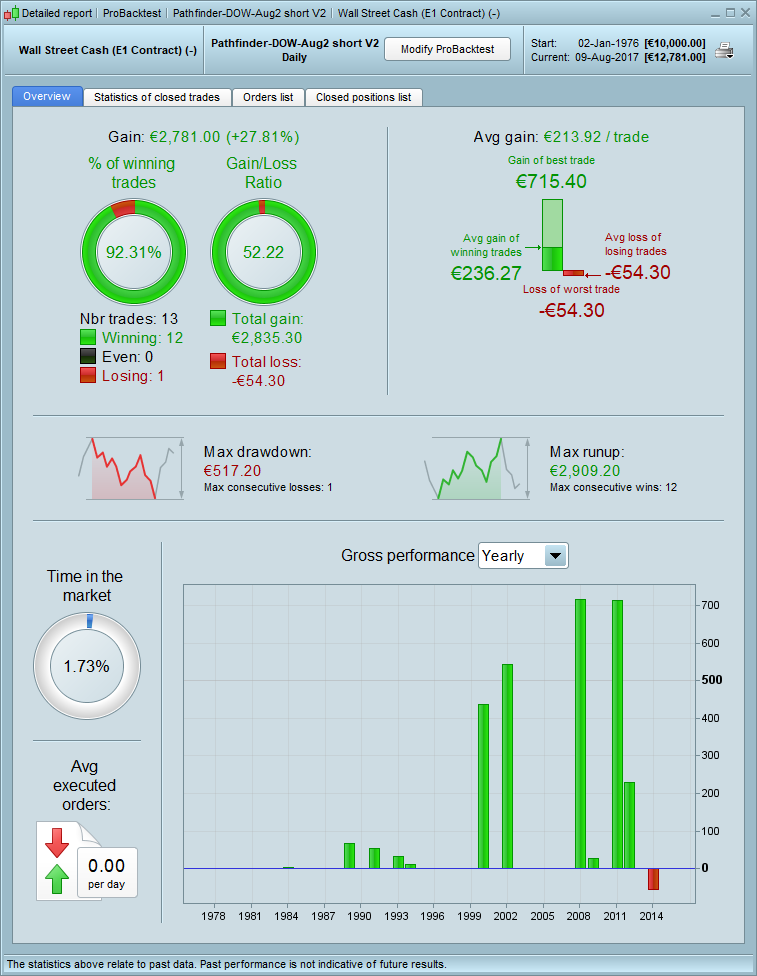

wp01Participant

Master

ASX Aug2; changed 1st. and 2nd. MA.

Dow Aug2 short:

wp01: The “underlying value” of the positions of corn I have active is about 1800 eu. If 10x that is recommended I should have 18000 EU on my account to be relatively safe. Have I understood this correctly? 🙂

I tried add manual stops in PRT by rightclick and “sell stop”. Didn’t work, it instead took two new short positions. Luckily I get mail for new positions so I closed them right away. Could change the stops by changing the orders instead….

wp01Participant

Master

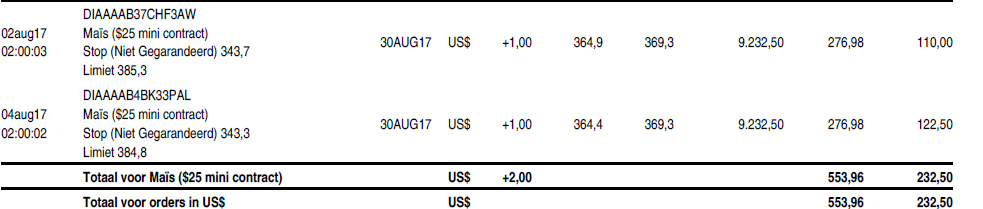

Hi Oskar,

Uh no the other way around.

See attached picture of todays statement.

The underlaying value is that 2 times $ 9.232,50 = $ 18.465,00. If you follow the recommendations of IG (1:10) you should have

$ 18.465,00 devided by 10 = $ 1.846,50 in cash in your account.

Indead when you open a position from PRT it opens a new one instead of closing the old one. I thought it was possible to do that by open it in the left corner the red or green arrow.

Not sure, but this can be found somewhere. Once a code is running you can not change anything. When you try this it closes the position. You can hedge your position, but is

also not recommended because if the position closes at night, your hedge is still running while you are asleep. Not sure if you are asleep at night 🙂

wp01: Ah I understand, thanks 🙂

Strange is the system stopped when I changed the stops, but it didn’t close the positions. They are up with the same limits but changed stops.

wp01Participant

Master

Ok, that is than different. When i tried to change anything it immediately closed the position and stopped it in ProOrder.

But that at least half a year ago, maybe it is changed or i didn’t understand it at that time.

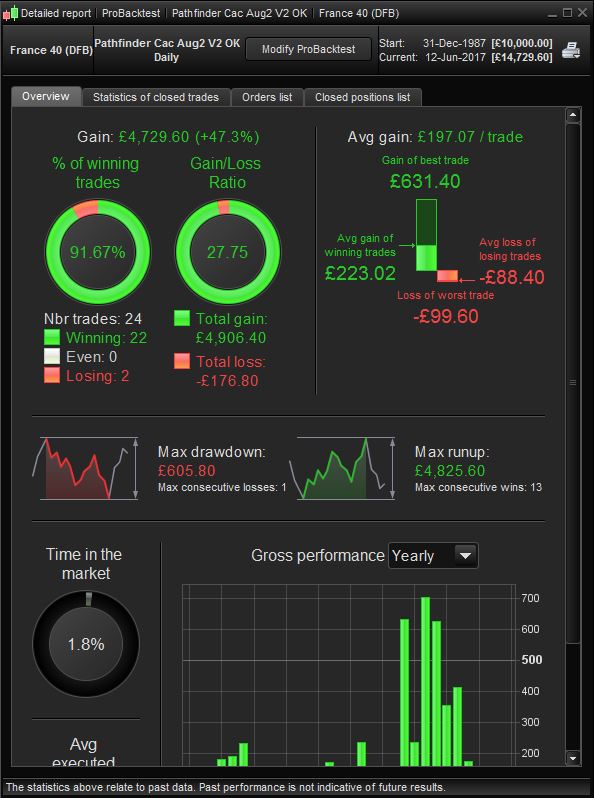

Hello Guys, here my contribution.

Cac short and long