As #Peter points out again, the solution to a problem can be a very long path, especially when you have to get others to walk it.

Hi druby – thank you for again a thoughtful post.

It is difficult to respond to the individual questions, because it seems that most take the standpoint that the data can be found somewhere, and thus we can reconstruct from there.

So let me try to explain what goes on (as how it all comes to me !) and what we have.

First of all it is good to look at PRT as a large spreadsheet (think literal here, as in a spreadsheet being able to sum things from adjacent cells and all).

This spreadsheet is fed with data, and the data never originates from PRT itself, unless it is user dedicated data such as your (set) time zone and more of this stuff.

The data is always fed by the broker. Be that IB or be that IG (or Saxo and possibly more). Always. Thus whatever it is we see, it originates at the broker, and is presented by PRT through its own “filters”. Daily profit is taken from the broker (enormously complex in itself, as touched in my previous post) and this is done in time intervals (like once per 10 minutes or whatever). After that, it is the internal spreadsheet doing the work. If you have Tesla in your portfolio, then PRT knows what to accumulate from where, in order to arrive at the daily profit, or even portfolio amount. Until the data is re-obtained from the broker (and all should match 100% for a fraction of a second) after which the self-accumulating restarts. And so on.

The statistics are NOT obtained from the broker. They are self-generated but with detail data from the broker.

The list of orders, ditto.

Commission is NOT obtained from the broker. And, I take IB as the example, because there Commission is in order. It is not obtained from the broker – IB – because it is not provided in their API.

The profit we see on a chart, is a strange mix of what the broker tells and what PRT can add herself to it, throughout the day, and which is always without commission. Daily profit is a mess (per chart already) because of the settlement times – daily profit starts at the last settlement, like DAX last 17:30 (16:30 your time) if only the DAX was open at that time (like Good Friday it may not – whatever). An effect of this, is that if I gained 2000 yesterday (Friday) this profit will be shown still at Sunday’s (/Monday’s) opening of USA Futures, and the 2K gain will be incorporated in the daily profit. Until the DAX opens (01:15 my time these days) then suddenly that 2K is deducted.

This is just what happens Live and in real life, and this is sufficiently obfuscating already. 🙂

The list of orders is thus also a spreadsheet. These days it can contain 1000 orders (recently upgraded from 500) and it is a FiFo list (first in first out).

You can add filters to the columns (one field which acts upon all the columns) and it will (very) nicely give you the orders of e.g. one Autotrading System (but have the column with the system name in there). All from Nasdaq ? just enter that as (part of the) instrument name and done. I use it quite some times per day, it works really great.

But only on these last 1000 orders, and as you may have seen by now, in my case the first orders of the day may have “FiFo”d out in the afternoon already (maybe not today’s but surely yesterday’s).

Thus such a list just contains 1000 lines (the spreadsheet is not larger) and it always contains everything of all instruments and systems. So no filter will help you to make it more.

The Statistics are based on the very same thing. An internal list which was upgraded to 10000 full trades (from 1500 which it was until a year or so ago), which this can show your financials only from the last 10000 trades. One could attest that you should not perform so many trades, but here the children’s garten phenomenon comes into play, right ?

So here too, no filter helps ? … wait … here it does ! (unless something changed when this was upgraded from 1500 to 10000).

So Yes, you could pull a statistic for each of the … what ? … instruments ? equities ? … and have them all on screen. Eh … ALL ? (max is 10 anyway)

What is ALL then ?

You won’t get far because you won’t know them. Too many things going on, already for Autotrading, let alone the sauce of manual trading which you also apply (I’d say). And mind you, all is about the performance of your Systems, right ?

The point remains : when something goes wrong with one of your systems, the statistics for that is destroyed, thus also the higher level for it (the instrument) is destroyed, and the highest level (your portfolio) is also destroyed.

So what happens is that one way or another, you won’t get there. This is not only related to the 10000 max, but also to the individuals not “working” any more.

And the data is nowhere else to be found.

I was once told “then go to IB to sort things out !”. No, at IB’s this is not there either, unless you know their data(base) and are able to make queries for it. But this is quite undoable because what to do with real time queries which don’t exist. And fun : from of V12 we can look at the statistics in real time (per checkbox for it – updated each 1 minute or so) Yea, until something goes wrong and the statistic is worthless forever.

This feels like GraHal’s first post : does PRT even know what they are making which for ? (my translation of it)

But can you tell again what you would want this all for ? … let me get your start(l)ed :

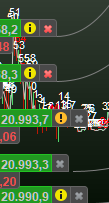

What you see below is a test run of one day. Statistic contains all (as far as I can tell) so nothing wrong there. What we sadly don’t see incorporated in the Commission. Yea, that one again. Well, it is sort of easy to see for the one system which ran there : 134 times 4.40 (2.20 per side as it still was the beginning of November – today it is 2.25). So instead of 1K profit it was 5K loss.

So what to do with this again ?

I can tell you, when this is observed live, you won’t have a clue of the outcome. We win some, we lose some (look at the start of it) and while we obviously know about the commission, you hope for the better. Until one massive DD occurs again and the testing is over (I did not show that, but envision that 1087.50 vaporized). Then you can cozily count your losses and arrive at 7K.

And so as long as the commission is not incorporated, it is quite useless to be able to provide a better complete picture (which this example was to begin with).

And oh, needless to say that this hidden loss of 6K is also (hidden) in the aggregated statistics. I-just-have-no-clue of performance results. All I can relatively reliably see is the portfolio amount. Which is, remember, obtained from the broker.

Do notice please, that with PRT-IG is is a sort of other way around;

There we have the PRT statistics quite fine (if we for now skip the errors which make the statistics fail), but appears your portfolio $ to be half of what the statistics tell you. Eh …

Maybe we recall from a year or so ago (was it two ?) that I called IG to have their annual report explained, which they actually could not do well apart from guessing. “Part A will be about interest and Part B will probably be about Spread – not sure !”. And their report really contains such a Part A and part B – the spread already incorporated in your trades hence PRT statistics.

In the end I could derive that the missing link was about interest indeed, which with IG is relatively high. But also : with IB we can see this deducted each day. With IG we don’t see this anywhere (or maybe things have changed ?). But anyway, this is a normal thing. It belongs.

Interest is there for IB as well ? maybe not because not for (the real) Futures. So the interest would only be for equities (Tesla and such) and Forex. With IG it is also for the CFD derivatives. And this is painful. How painful ? well, if PRT statistics show 20K profit, reality will be maybe 12K or so. Of course this depends on overnight positions, but I have those and thus this is real life for me.

This latter part is off topic of course, if we only recognize that with IG the “insight” is not really much better than with IB. But it depends on your trading fashion. Thus, have one trade per day and you won’t notice a thing regarding the offset between PRT statistics and your IB portfolio $. And the other way around : have 1000 trades per day with IG and you again won’t notice a difference between PRT statistics and portfolio $. Not even because of interest in that case (you probably wont be in overnight).

Hopefully this helps some ?