dopo vari mesi di prove… su conto demo tutti i sistemi provati danno esito negativo…. anche quelli con i risultati della simulazioni migliori … fanno tutti la stessa fine … ora mi chiedo … ma qualcuno che ha un sistema che gira in reale e che guadagna esiste con questa versione 10.2 ….

in attesa che esca la nuova versione…

grazie a chi vorrà rispondere …

saluti

Max

ALE

ALEModerator

Master

Ciao Max

Hai provato Il sistema QU dax, QU ftse, Pathfinder V6?

ciao Ale,

no ancora no.. proverò anche questi..

il qu dax ho visto che ci sono 4 file da scaricare cosa li differenzia uno dall’altro … qu sell, qu buy, qu turbo,univ qu dax.. poi una versiona ottimizzata da miguel .. da quale devo partire …

grazie

ALEModerator

Master

Ciao

scarica

Qu buy / Qu sell/ Qu turbo

Miguel ha ottimizzato la la versione, su uno storico di 100.000 barre io l’ho costruita su 200.000 barre.

decidi tu quale usare.

ALEModerator

Master

Scusa dimenticavo anche il 4′ file univ

la strategia e Qu turbo, gli altri 3 file sono gli indicatori per far funzionare la strategia

perfetto grazie … adesso li carico in piattaforma…se ho bisogno ti disturbo …

la Pathfinder V 6 invece non l’ho trovata… ho trovato la versione fino V 3 se puoi indicarmi il link.

grazie ancora …

Max..

opss… ho visto che da oggi c’è la versione 10.3 cambia qualcosa per questi codici oppure si possono caricare e funzionano senza problemi …

grazie..

ALEModerator

Master

Ciao

io ho sempre la 10.2, potresti inviarmi copia del probacktest cosi che guardo?

grazie

Ale

ALEModerator

Master

Pathfinder v6 4h

//Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 6

// Instrument: DAX mini 4H, 9-21 CET, 2 points spread, account size 10.000 Euro, from August 2010

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 90000

ONCE endTime = 210000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3

// define filter parameter

ONCE periodLongMA = 300

ONCE periodShortMA = 50

// define position and money management parameter

ONCE positionSize = 1

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

ONCE stopLossLong = 5.5 // in %

ONCE stopLossShort = 3.25 // in %

ONCE takeProfitLong = 3.25 // in %

ONCE takeProfitShort = 3.25 // in %

maxPositionSizeLong = MAX(45, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(45, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

ONCE trailingStartLong = 2 // in %

ONCE trailingStartShort = 0.75 // in %

ONCE trailingStepLong = 0.2 // in %

ONCE trailingStepShort = 0.4 // in %

ONCE maxCandlesLongWithProfit = 16 // take long profit latest after 16 candles

ONCE maxCandlesShortWithProfit = 15 // take short profit latest after 15 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 12 // limit short loss latest after 12 candles

// define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

ONCE January1 = 3

ONCE January2 = 0

ONCE February1 = 3

ONCE February2 = 3

ONCE March1 = 3

ONCE March2 = 2

ONCE April1 = 3

ONCE April2 = 3

ONCE May1 = 1

ONCE May2 = 1

ONCE June1 = 2

ONCE June2 = 2

ONCE July1 = 3

ONCE July2 = 1

ONCE August1 = 1

ONCE August2 = 1

ONCE September1 = 3

ONCE September2 = 0

ONCE October1 = 3

ONCE October2 = 2

ONCE November1 = 2

ONCE November2 = 3

ONCE December1 = 3

ONCE December2 = 2

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month[1] <> Month[2] then

//If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal multiplier

currentDayOfTheMonth = Date - ((CurrentYear * 10000) + CurrentMonth * 100)

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2)) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry without order cumulation

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

numberCandles = (BarIndex - TradeIndex)

m1 = posProfit > 0 AND numberCandles >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND numberCandles >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND numberCandles >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND numberCandles >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function (convert % to pips)

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

stopLoss = stopLossLong * 0.1

takeProfit = takeProfitLong * 2

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

IF LONGONMARKET THEN

SELL AT newSL STOP

ENDIF

IF SHORTONMARKET THEN

EXITSHORT AT newSL STOP

ENDIF

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

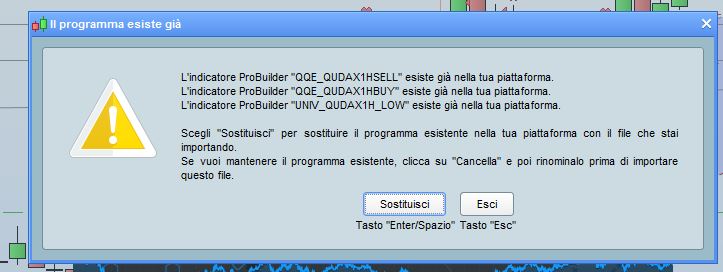

ciao, ho caricato i 3 file descritti quando metto il 4 mi dice gia esistente … inoltre li mette tra gli indicatori e non tra i sistemi ..

cosa posso fare..

grazie ..

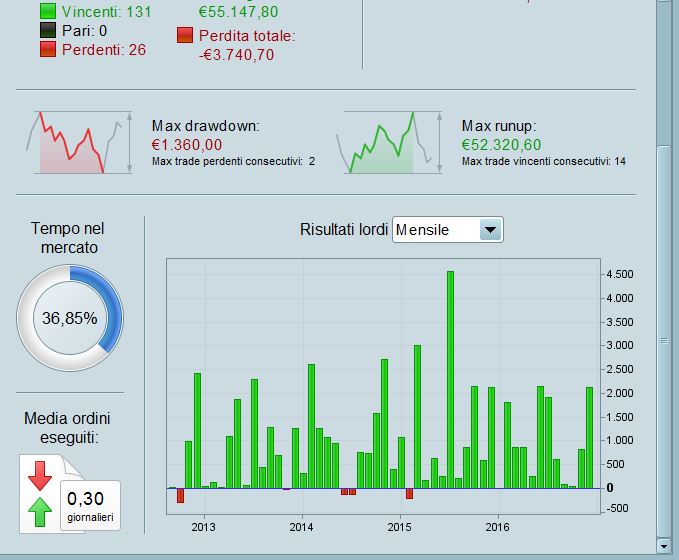

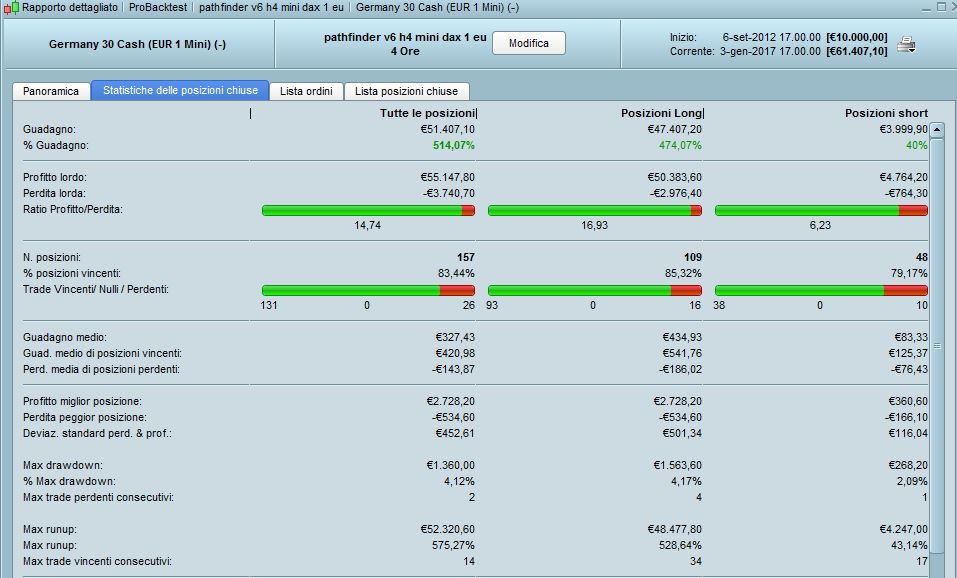

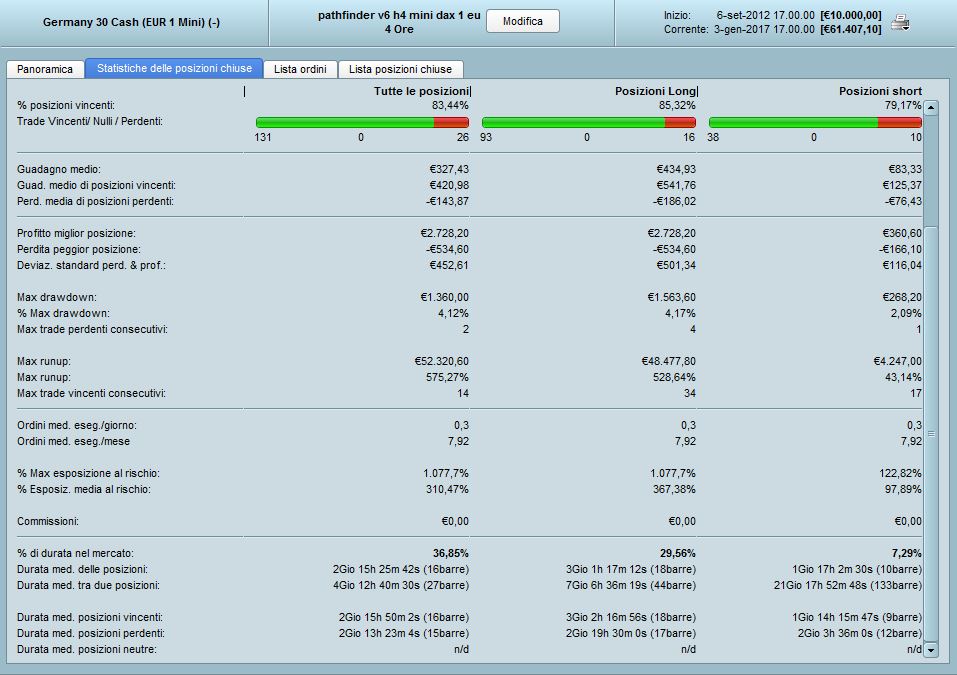

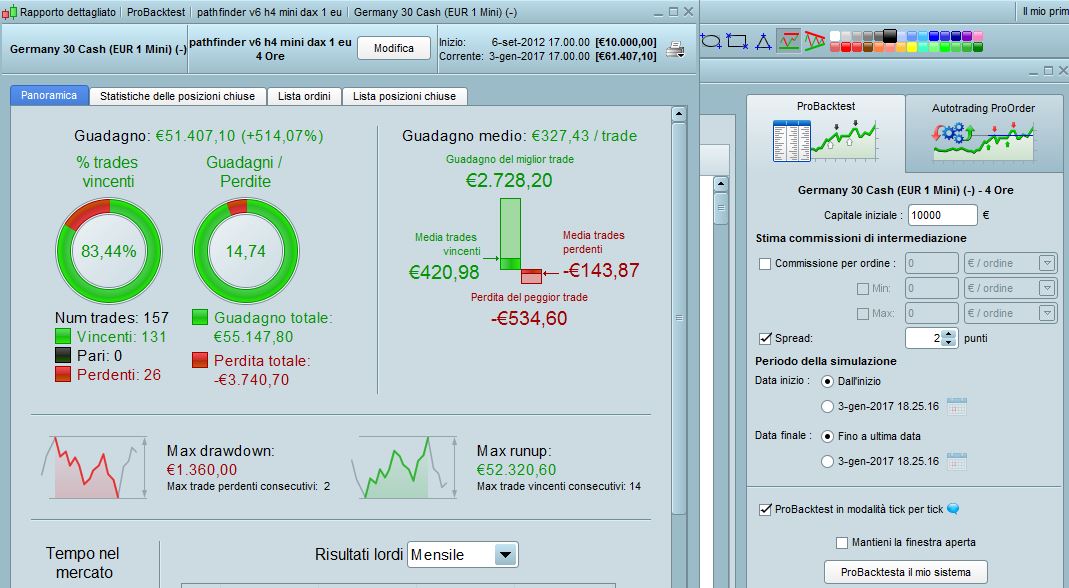

questo è il report del pathfinder 6v ho usato dax mini 1 euro

se ti serve altro dimmi pure ..

ALEModerator

Master

Ciao

OK gli indicatori sono presenti, ora dovresti trovare la strategia nel menu, ed avviarla. QU_DAX_TURBO, time frame 1h, DAX 1€ CFD INDICE

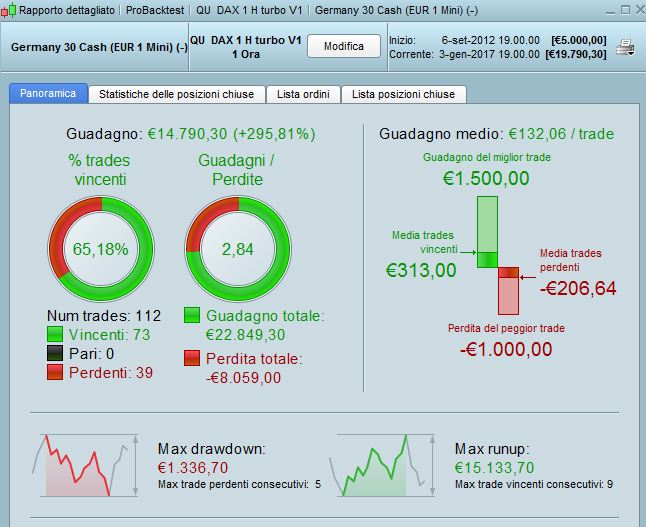

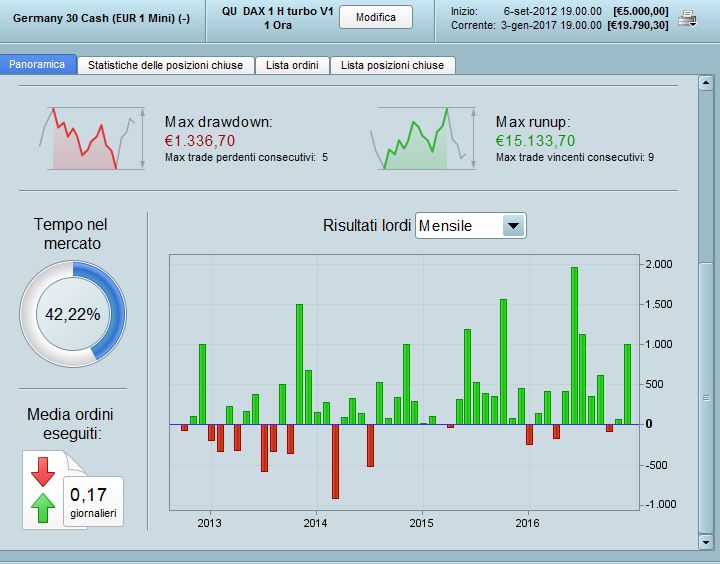

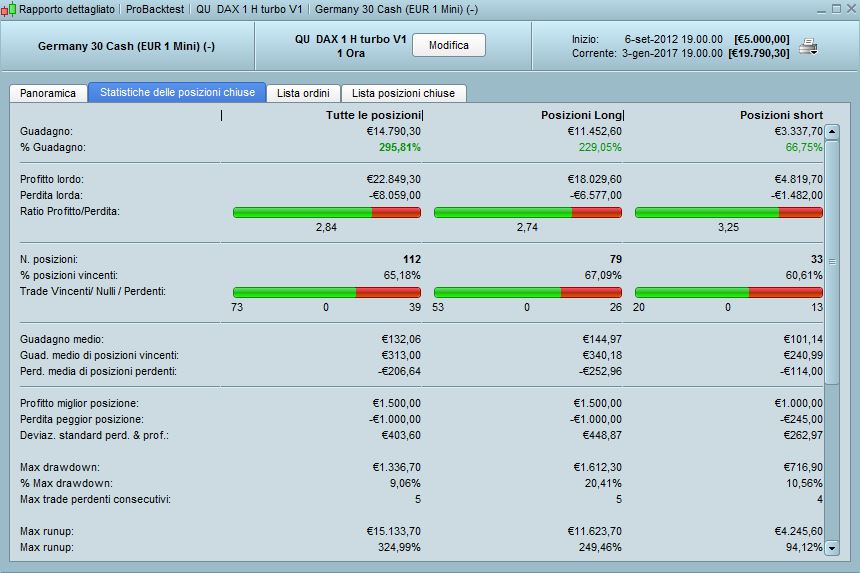

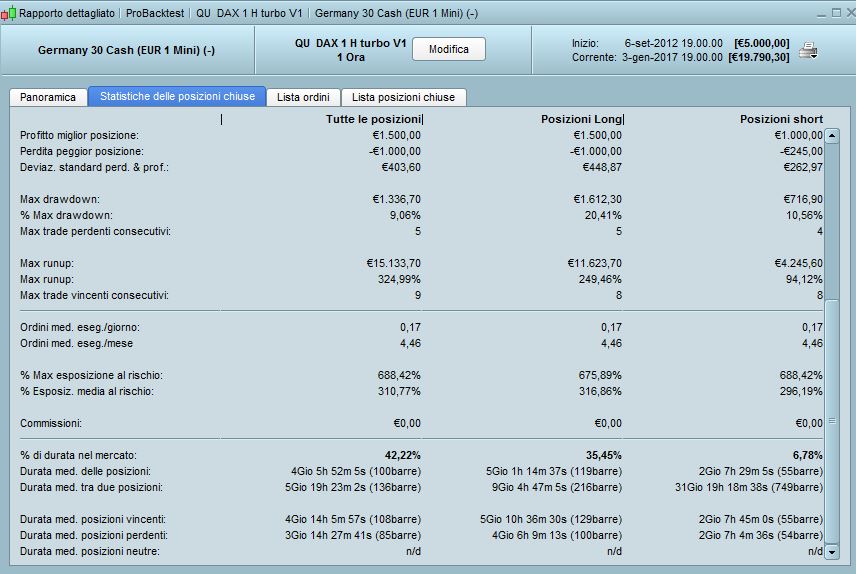

ok fatto .. ho provato a caricarlo sopra … quando mi chiede se voglio sostituire ho detto si .. ed ha funzionato è stato istallato …

controlla se ho fatto bene … questi sono i report

spread 2

invio anche una copia delle ultime operazioni ..

ALEModerator

Master

Ciao

si è corretto, la strategia è molto semplice, ti è chiaro il funzionamento? osservando la posizione degli indicatori saprai quando il sistema entrerà a mercato all’apertura della candela successiva, ovviamente lavora su periodi piuttosto lunghi, per cui è overnight.