Good evening everyone,

i’m testing a strategy based on the sector rotation, so i’ve put together a watchlist with several sector ETFs from the S&P500. The strategy consists in trading just the top 3 ETFs ranked by the strength of their trend.

How to measure the strenght of the trend? I’ve read many articles and someone made an expression to calculate it.

This is the expression:

TrendStrength=(2*close/close(63))+(close/close(126))+(close/close(189))+(close/close(252))

where close(63) is the closing price of 63 days ago and so on.

The screener should rank the titles in the watchlist by this value.

Can someone help me with this?

Also, any other ideas on this topic or other ways to calculate this value are well accepted.

Thank you and have a nice evening.

F

You can use the Relative Strength Rank Indicator in order to make the screener.

Good morning Nicolas, thanks for the feedback.

Well I saw that post before but first I don’t really know how to make a screener out of that code (my bad, I have to learn) and second it doesn’t really look like the one I described above. Isn’t it?

Not the same as your formula indeed, so according to it you could try the simple screener below:

TrendStrength=(2*close/close(63))+(close/close(126))+(close/close(189))+(close/close(252))

screener(TrendStrength)

All the shares of the list(s) will be automatically sorted with the “trendstrength” calculation result.

Thank you Nicolas, i didn’t know it was that easy.

I’ll try to make also the screener based on the indicator you mentioned above.

Have a nice day!

F

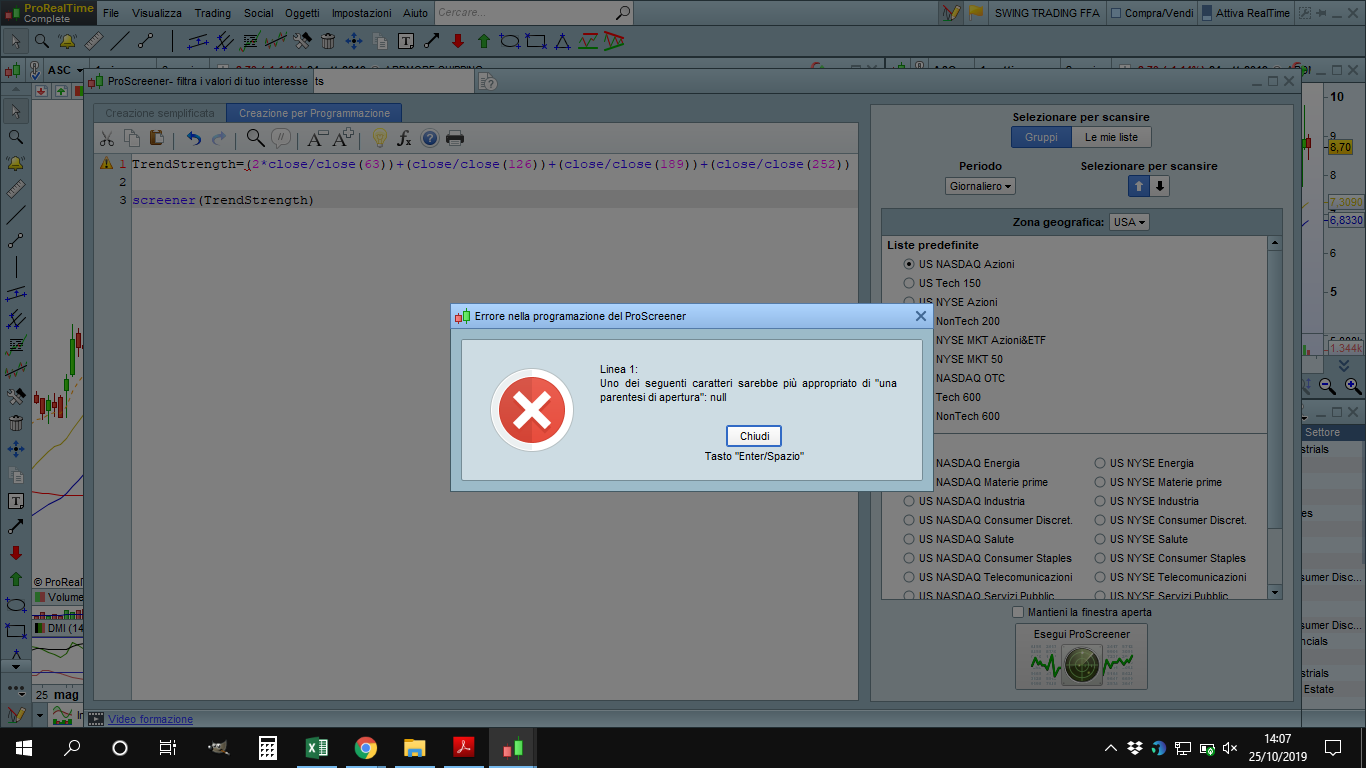

Sorry to bother you again, but the code gives me an error, please see attached picture for reference.

Thank you

Sorry, my mistake, Close offset should be in brackets, not parenthesis 🙂

TrendStrength=(2*close/close[63])+(close/close[126])+(close/close[189])+(close/close[252])

screener(TrendStrength)

Thanks a lot, now it works!

You can use the Relative Strength Rank Indicator in order to make the screener.

Good evening Nicolas,

i’ve followed your advice and used your Relative Strength Rank Indicator to make a screener. I’m using it to rank a group of sector ETFs in order to trade the top three.

I’ve read somewhere that some traders are using a similar indicator with more than two timeframes, so i modified the code as follows:

//PRC_Relative Strength Rank | indicator

//08.07.2019

//Nicolas @ www.prorealcode.com

//Sharing ProRealTime knowledge

// --- settings

RsrShortPeriod = 63

RsrMedShort = 126

RsrMedLong = 189

RsrLongPeriod = 252

RsrMaMode = 0 //MA type

AtrPeriod = 10

// --- end of settings

RsrPrice = customclose

price = average[1](RsrPrice)

mas = average[RsrShortPeriod,RsrMaMode](RsrPrice)

mams = average[RsrMedShort,RsrMaMode](RsrPrice)

maml = average[RsrMedLong,RsrMaMode](RsrPrice)

mal = average[RsrLongPeriod,RsrMaMode](RsrPrice)

atr = averagetruerange[AtrPeriod]

if (atr<>0) then

rsr = (price-mas+price-mams+price-maml+price-mal)/(2.0*atr)

else

rsr = 0

endif

screener (rsr)

In your opinion, does it make any sense to involve two more timeframes in the calculation?

Considering such long timeframes, the value of ATR (now set at 10) should be increased?

Thank you for your time and help.

Bos.

Bos.Participant

Veteran

Here is a version I made that’s slightly different. It screens for stocks with relative strength above 80% that are also above the 200ma

indicator1 = Average[200](close)

c4 = (close > indicator1)

RS = 2*close/close[63] + close/close[126] + close/close[189] + close/close[252]

Var1 = 8

RelativeStrength = RS > Var1 AND c4

SCREENER[RelativeStrength] (RelativeStrength AS "RS > 80%")

Thank you for your contribution Bos. Interesting point of view!

I’ll be really glad to hear Nicolas’ opinion on the code i posted above 🙂

What you have done is not a multiple timeframe analysis, but a single one with longest period. What you read about comparing multiple relative strength rank across multiple timeframes could be assimilated as a dual/triple momentum ranking.

For instance, a dual momentum analysis is built upon the fact that a stock in a strong uptrend period (high strength) should have some small periods of calm (low strength) and that’s when you should consider invest in them, you can use this technique when re-balancing a portfolio.

Thank you very much. I’ll discard the code i wrote then.

Any advice on how to code a double/triple momentum screener? i’ve searched the forum but got nothing about it.

Or it’s better to just use the screener i made out of with your RSR Indicator?

Yes but with conditions based on 2 timeframe for instance. Use the TIMEFRAME instruction for ProScreener in order to achieve the dual momentum conditions.