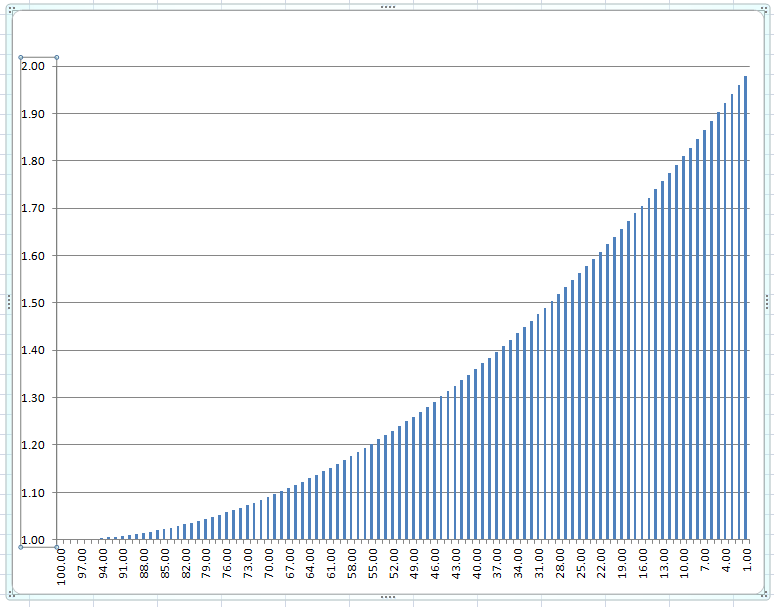

When using an RSI value as a condition to enter a trade it can often be seen that there is a direct correlation between the value of RSI at the time of entry and the probability of a trade being profitable and the amount of gain per trade. In something like the popular long only RSI[2] mean reversal strategy this correlation could be used for varying our position sizing. We stake more if the value of RSI is low and less if it it is high. Unfortunately the correlation does not seem to be a straight line from 0 to 100 so our position sizing would benefit from a calculation that produces a curved line between 0 and 100 that more closely represents the true probability.

I have come up with this calculation that produces a nice curved position size line but I wondered if any of the much better mathematicians out there had a better calculation.

minpossize = 1

positionsize = (((((100 - RSI[2]) * (100 - RSI[2])) / 100) / 100) + 1) * minpossize

[attachment file=80617]