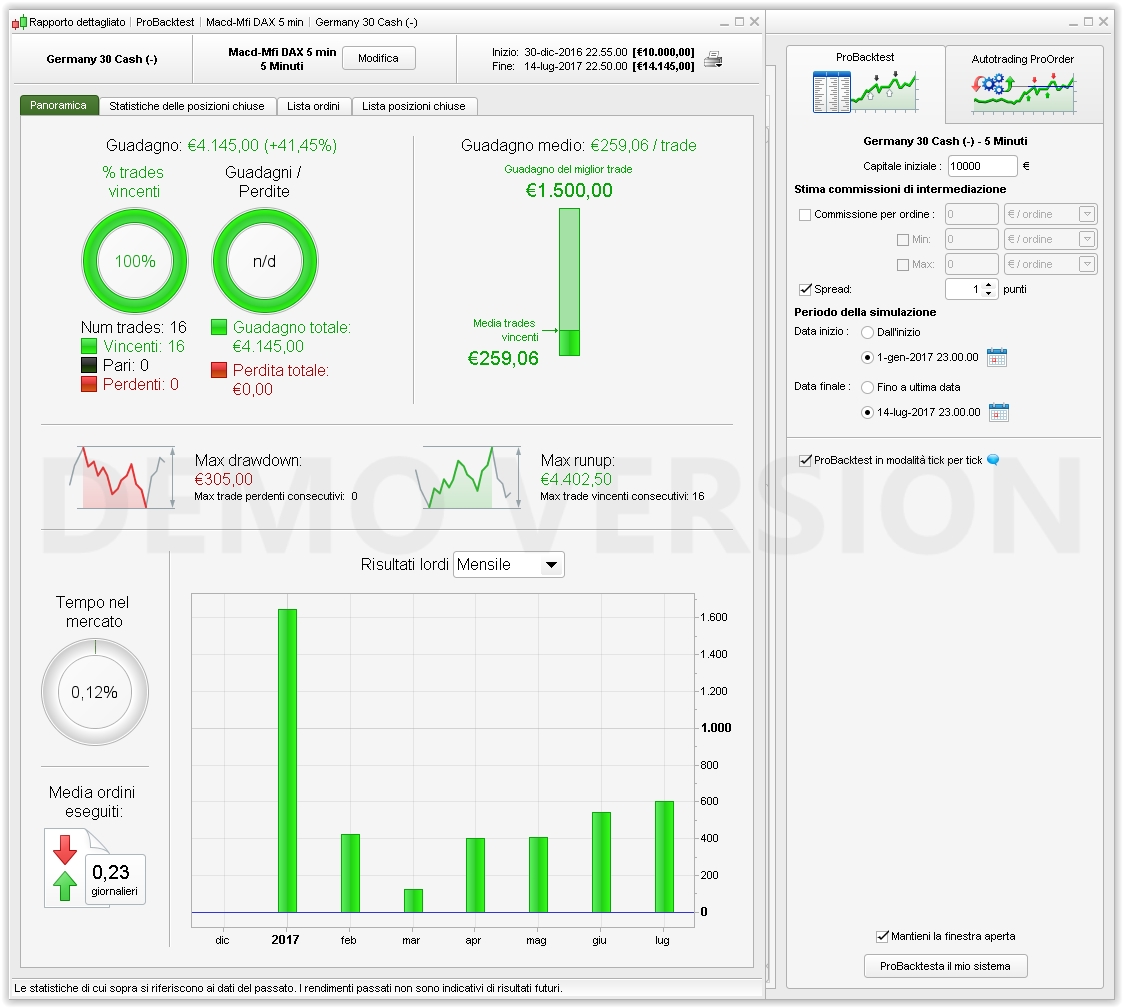

[attachment file=”41061″]

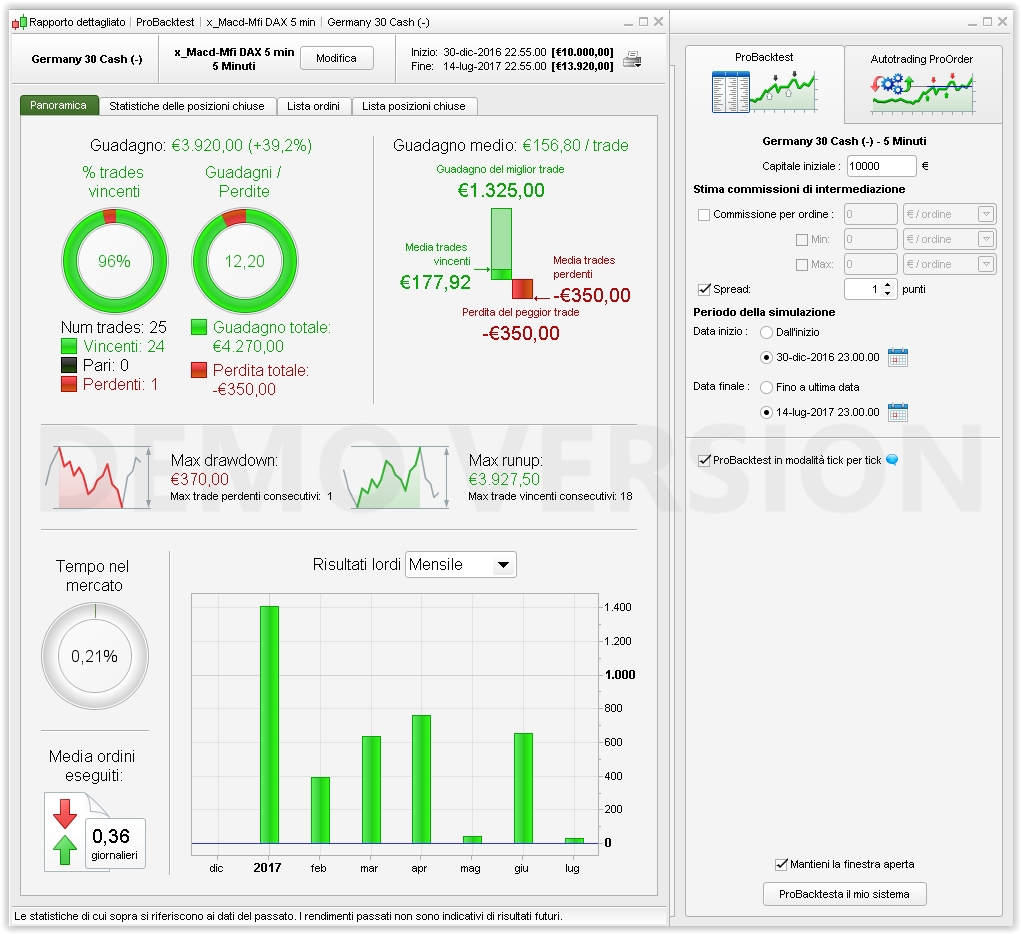

Hi @GraHal, I modified the code replacing the built-in MFI with the oscillator you suggested, it seems to work correctly. We’ll see tonight what’s gonna happen after DAX closes!

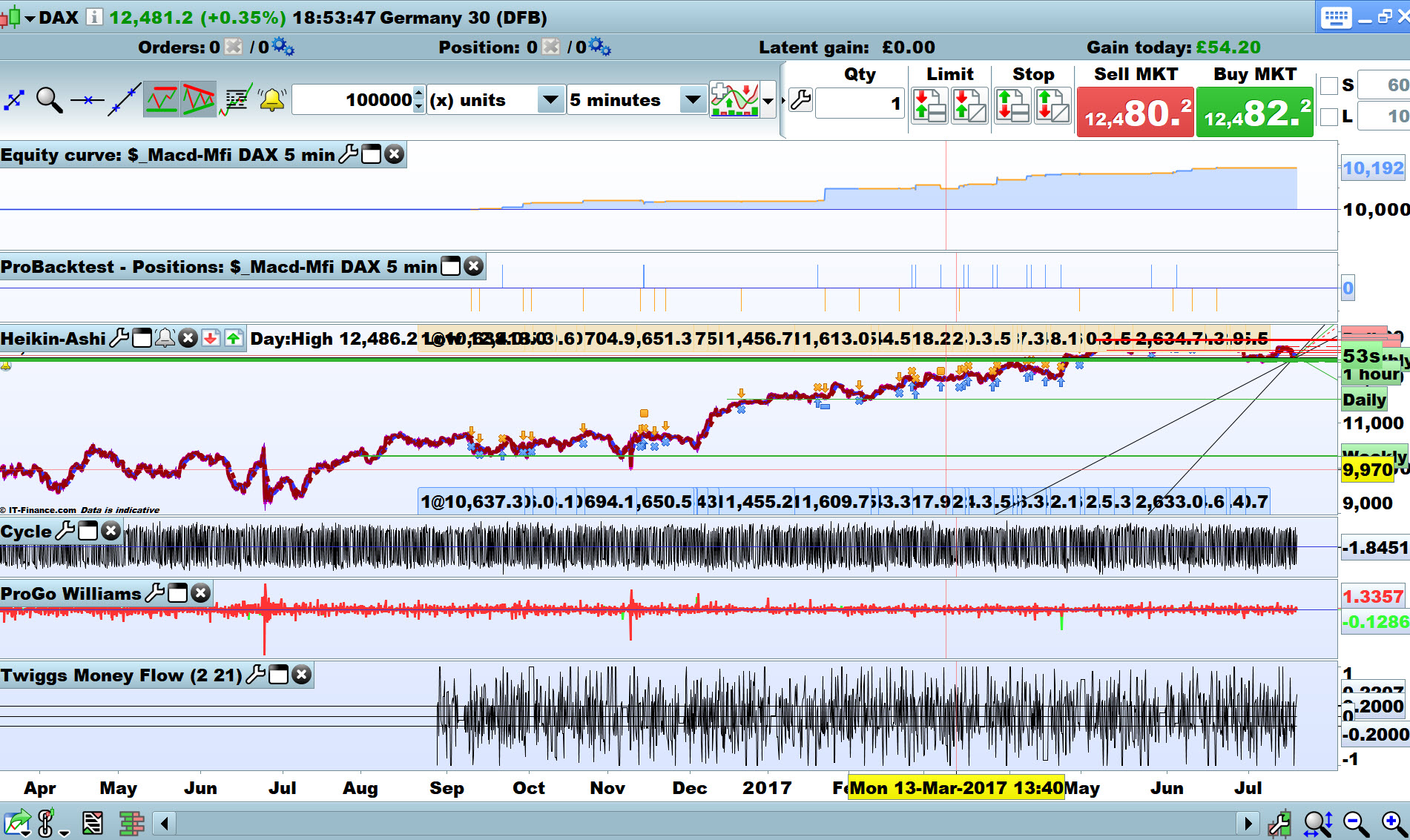

Here’s the code for the strategy:

//-----------------------------------------------------------------------------------------

// Jul 19, 2017 Macd-Mfi DAX 5 min

//

// Version 2: modified to replace built-in MFI (Money Flow Index) with

// external Twiggs Money Flow

// (link https://www.prorealcode.com/prorealtime-indicators/twiggs-money-flow/)

//-----------------------------------------------------------------------------------------

DEFPARAM CumulateOrders = False

DEFPARAM FlatBefore = 090000 //no trades before 09:00:00

DEFPARAM FlatAfter = 213000 //no trades after 21:30:00

ONCE nLots = 1 //number of LOTs traded

ONCE TP = 53 //53 pips Take Profit

ONCE SL = 14 //14 pips Stop Loss

ONCE Macd1 = 22 //22

ONCE Macd2 = 32 //32

ONCE Macd3 = 9 //9

MacdVal = MACD[Macd1,Macd2,Macd3](close)

MacdSignal = MACDline[Macd1,Macd2,Macd3](close)

//MfiVal = MoneyFlow[9](close) //9

//ONCE MfiLimitBuy = 3200 //3200

//ONCE MfiLimitSell = -MfiLimitBuy

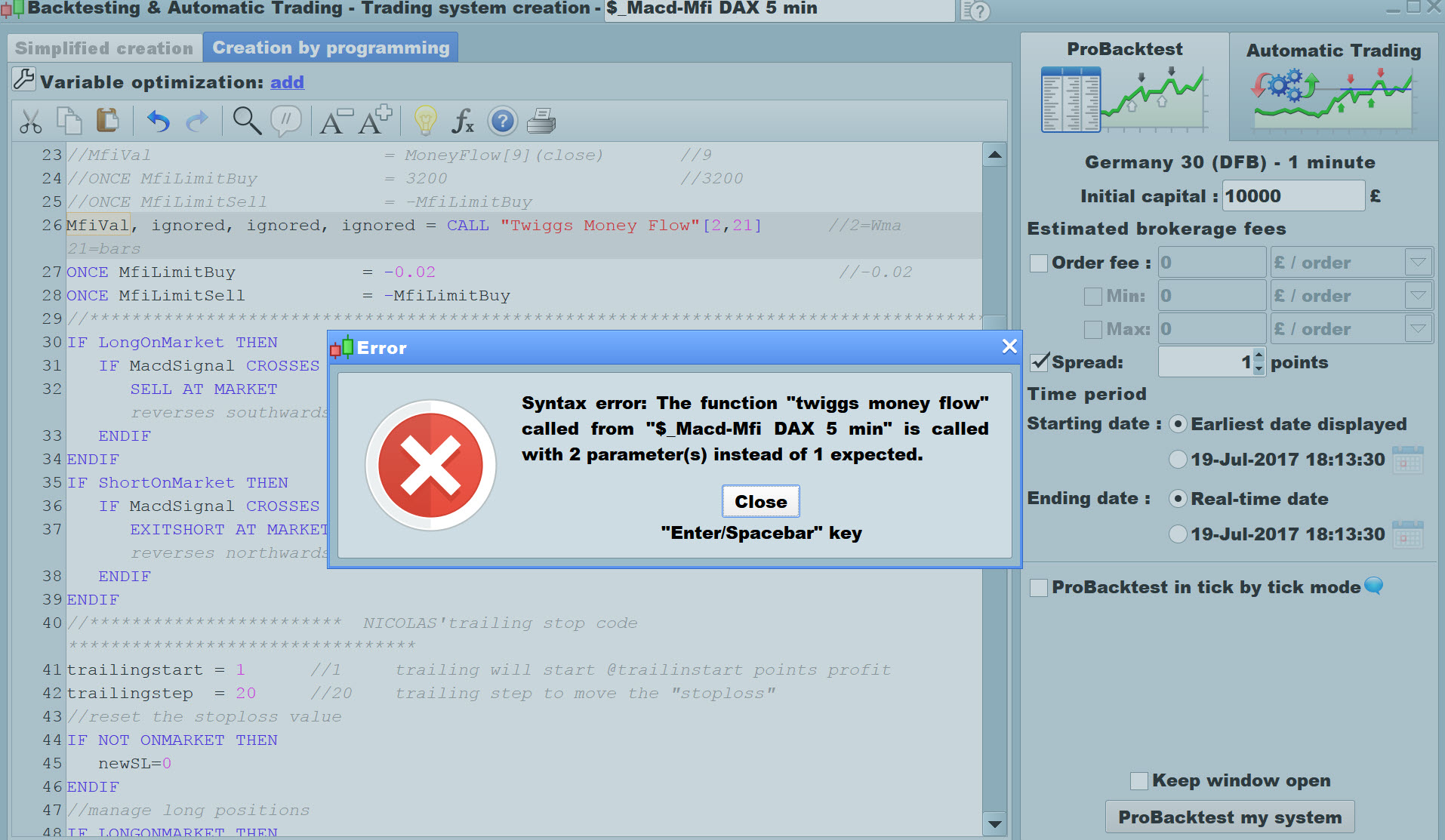

MfiVal, ignored, ignored, ignored = CALL "Twiggs Money Flow"[2, 21] //2=Wma 21=bars

ONCE MfiLimitBuy = -0.02 //-0.02

ONCE MfiLimitSell = -MfiLimitBuy

//***************************************************************************************

IF LongOnMarket THEN

IF MacdSignal CROSSES UNDER MacdVal THEN

SELL AT MARKET //Exit LONGs when MACD reverses southwards

ENDIF

ENDIF

IF ShortOnMarket THEN

IF MacdSignal CROSSES OVER MacdVal THEN

EXITSHORT AT MARKET //Exit SHORTs when MACD reverses northwards

ENDIF

ENDIF

//************************ NICOLAS'trailing stop code *********************************

trailingstart = 1 //1 trailing will start @trailinstart points profit

trailingstep = 20 //20 trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//***************************************************************************************

// LONG trades

//***************************************************************************************

a1 = close > open //BULLish bar

a2 = MacdSignal CROSSES OVER MacdVal //MACD goes North

a3 = (MfiVal < MfiLimitBuy)// AND (MfiVal > MfiVal[1]) //< Mfi limit AND > previous

IF a1 AND a2 AND a3 THEN

BUY nLots CONTRACT AT MARKET

ENDIF

//***************************************************************************************

// SHORT trades

//***************************************************************************************

b1 = close < open //BEARish bar

b2 = MacdSignal CROSSES UNDER MacdVal //MACD goes South

b3 = (MfiVal > MfiLimitSell)// AND (MfiVal < MfiVal[1]) //> Mfi limit AND < previous

IF b1 AND b2 AND b3 THEN

SELLSHORT nLots CONTRACT AT MARKET

ENDIF

//

SET TARGET PPROFIT TP

SET STOP PLOSS SL

//GRAPH MfiVal AS "Mfi"

and the code for the oscillator:

REM TWIGGS MONEY FLOW

// adaptación del código de LazyBear en tradingview para PRT

// parámetro t (tipo de media en cuadro de variables):

//

// 0 = SMA

// 1 = EMA

// 2 = WMA

// 3 = Wilder

// 4 = Triangular

// 5 = End point

// 6 = Time series

//

DEFPARAM CalculateOnLastBars = 200

//

length=21

//

trh=MAX(close[1],high)

trl=MIN(close[1],low)

trc=trh-trl

if trc=0.9999999 then

trc=trc

endif

//

adv=VOLUME*((close-trl)-(trh-close))/trc

wv=VOLUME+(VOLUME[1]*0)

wmV=Average[length,t](wv)

wmA=Average[length,t](adv)

//

if wmV=0 then

wmV=0

else

tmf=wmA/wmV

endif

//

RETURN tmf as "twiggs money flow",0 as "0",0.20 as "0.20",-0.20 as "-0.20"

As for variables a3 and b3 I commented out the reference to the previous bar, since it’s performing slightly better.

I attached a wrong picture, the correct one is the one with V2 in the name.

I still don’t know how to reference a username with a link, sorry for that!!!

Roberto