@Vonasi : sometimes I tell myself that automatic trading is perhaps just a utopia… a great utopia… and some others times i think it is not a utopia and i try again and again…

Balmora74 – Yes sometimes it is like bashing your head against a brick wall and at some point you think ‘I need to try a different wall’. Then later you think ‘Hey – I’m gonna try that wall again’. Some good comes from every impact even if it is just reassuring you that it is definitely the wrong wall that you keep bashing your head against.

@Vonasi : so trading is a dilemma that can hurt your head … and your piggy bank 🙂

so trading is a dilemma that can hurt your head … and your piggy bank

Rather my head than my piggy bank any day of the week!

Edurecio – A while back I spent a lot of time trying to create a self optimising strategy that checked what had worked best recently and then used those settings until the self optimisation said that something else worked better recently. It produced nice equity curves in back testing but completely failed in forward testing. In every strategy there is some sort of variable that is fixed – whether it is an actual value or just using closing price instead of median price. So something is optimised and fixed in every strategy before we even try to check what worked best recently for other variables and hope that it works for a bit longer with a new value for them. I gave up on the concept of self optimisation and it proved to me that regularly re-optimising does not work either.

Just my humble opinion.

Good Morning.

Vonasi, I agree with you.

But you talk about reoptimizing. I do not speak of optimizing, but of looking for average values that make the system work without pretending to be optimized.

I presume that an optimization of a time series will not work in the future, since then, I am looking for an average obtained with the accumulated optimization of each month. As always, there will be months with better results, months with worse results and even some negative months.

Negative months: for example last month, which was so flat for this system with market exits based on weeklypivots, that would not work under any logical forecast.

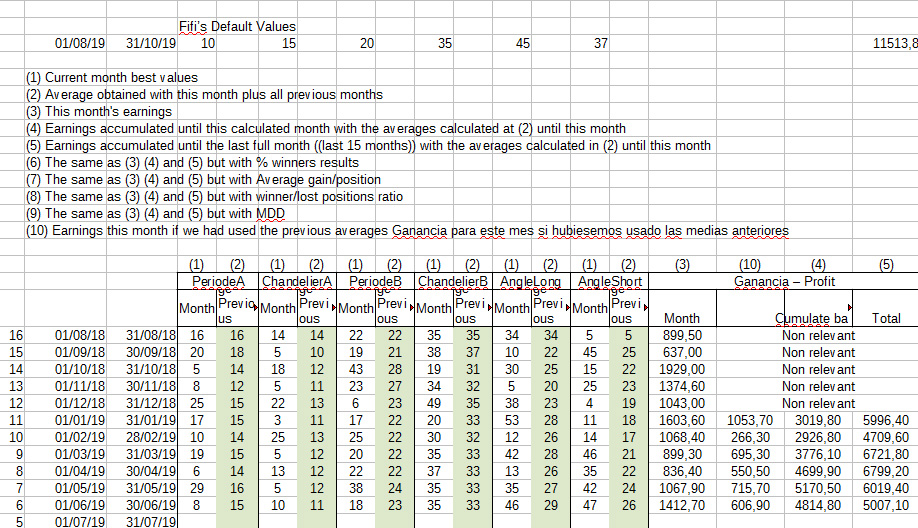

I leave a series of data obtained until June.

What I would put in July the average data (blue) obtained until June in the system. I would see how many gains that data gives me (10) but at the end of the month, I would calculate what the optimized data would have been (3) to have an average to use again in August. And so month after month, observing a trend in the means towards a midpoint of gains in the system.

I am not looking for an optimization, I am looking for an average of valid values.

It will not be a perfect system because I think there is not, but it seems to me an approximation that should be valued.

I am looking for an average of valid values.

“of valid values” from the past? Then we could also designated that as “Optimization” 😉 Don’t take it wrong, but valid values would have been the ones that you could have been robustly validated in a OOS period.

So the way you do is not bad, but it is the same as simply using optimized variables, if you don’t make a robustness test, you will never know that they were the good ones or the good way to calculate/define them.

I am looking for an average of valid values.

“of valid values” from the past? Then we could also designated that as “Optimization”  Don’t take it wrong, but valid values would have been the ones that you could have been robustly validated in a OOS period.

Don’t take it wrong, but valid values would have been the ones that you could have been robustly validated in a OOS period.

So the way you do is not bad, but it is the same as simply using optimized variables, if you don’t make a robustness test, you will never know that they were the good ones or the good way to calculate/define them.

I don’t take it wrong, I try to learn.

“… but valid values would have been the ones that you could have been robustly validated in a OOS period” We have the possibility to validate in a OOS Period every month (I’m in no hurry), comparing the data obtained with the previous accumulated average with the data of a theoretical optimization for only that month. Also see how much convergence deviates from the mean with each new monthly calculation as a robustness sample.

I do not consider myself with “the truth”, I know very little compared to many of you (Nicolas, you are really an expert and I am a rookie !!) but I think that way exists and can be combined with other forms of evaluation of variables

Greetings.

We have the possibility to validate in a OOS Period every month (I’m in no hurry)

You don’t need to validate your model in live OOS, do it in the past before or after your IS period, whatever. I ensure you that there is no “truth”, at the end of your journey through exploration of automated trading, you will find that the best robustness test you can do is just by running it live in present or in the past, in one or multiple OOS periods.

Personally I think that the best way to make money with System trading is to transform your Trader systems into trading systems, then put them on demo for at least a year, then if everything still works put them in real …….. But this is just my way of building trading systems …..

Hello Fran55

Can you post for everyone this good version? (to avoid errors)

All others are garbage

Same old story, repeating over and over again: optimization without validation always lead to the same conclusion. The walk forward tool is there to assist you in that task, use it!! 🙂

I’m preferring the first one the most too, although I have made slight changes, not completely happy with it yet.

with V6.2 I really like the auto Reinvest Position Size element, is there a write up about this anywhere?…(regarding max drawdown ect) save me going through the 900 lines of code?

Fran55

The first … of Balmora.

—————

= original, first post of the discussion? Vectorial-DAX-M5-2.itf ?

Balmora74 has made several improvements (exemple Paul on the first page).

itf please 🙂