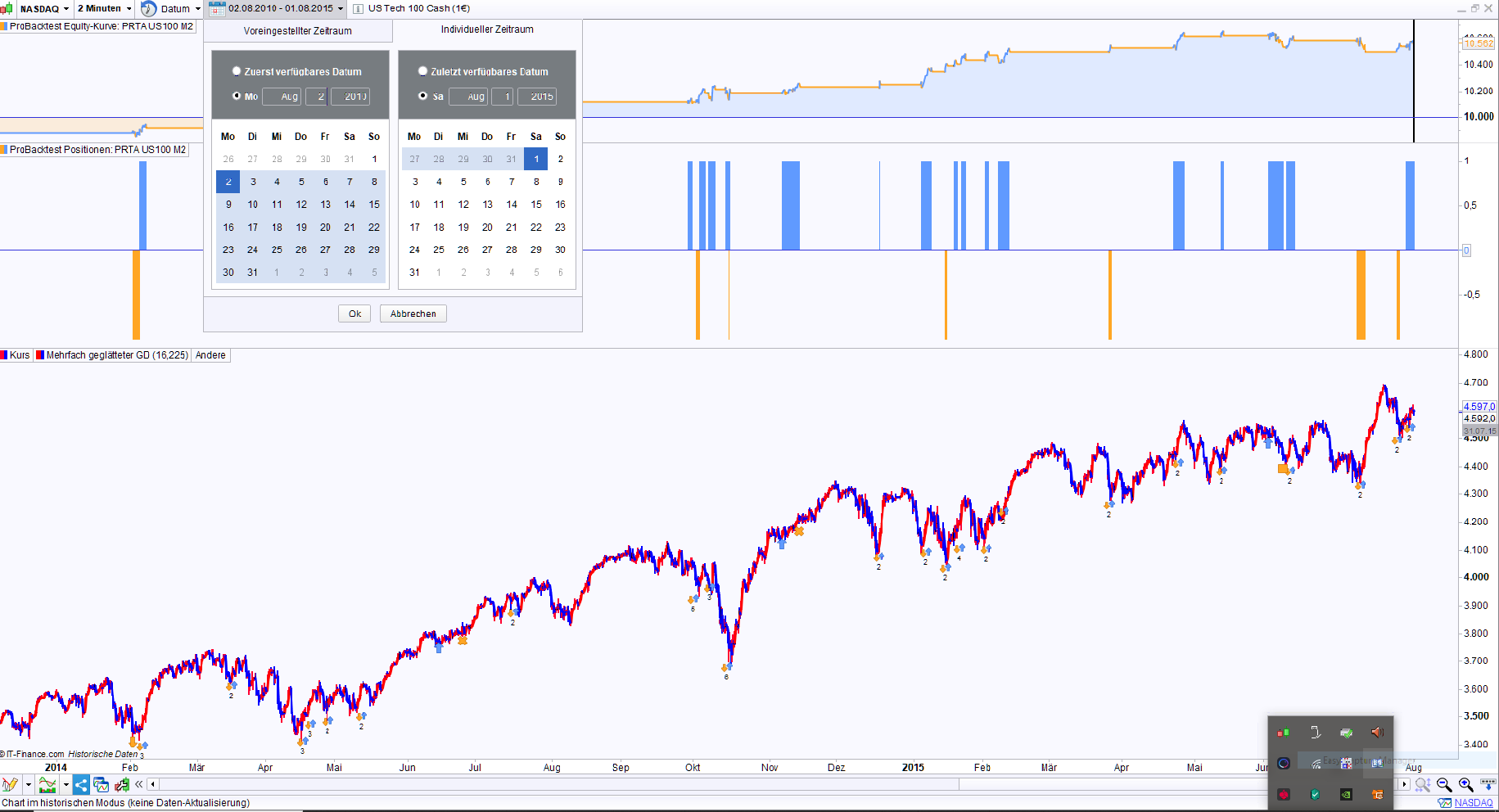

Thanks @XORANDNOT but it seems we can’t select previous period as you can see on the picture (PRT 11.1)

And how can have backtest results with 2 periods, on the same picture ?

Thanks and hae a nice day

You can’t backtest 2 different periods on the same picture. You have to do two separate backtests in two separate windows in historical mode.

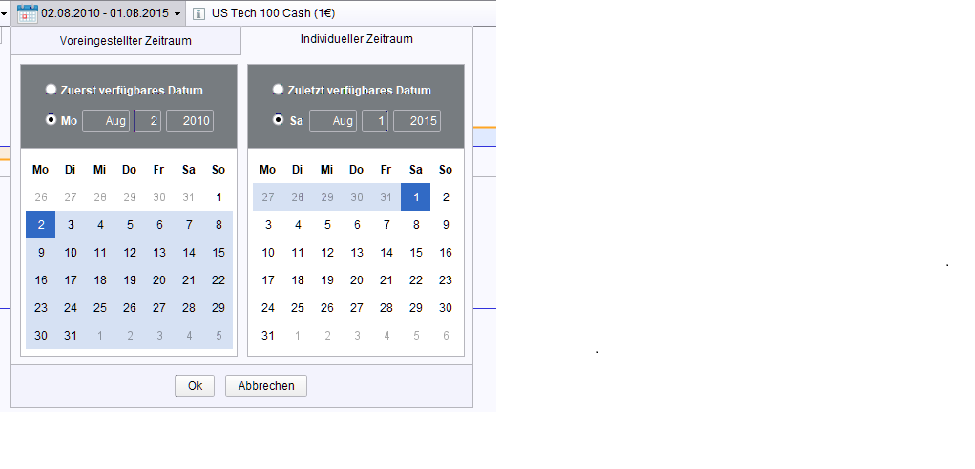

In case you can’t change the dates in your example, select first “première date afichée” or August, 02, 2010 on the left hand side. Then you can change also the final date on the right hand side.

Yes excel. Now with totals

Thank you. How much would have been the purchase price for all of these algos to get the 1801 points total ?

And how much is the total capital exposure ? 20 algos * 10.000 Euro (very roughly) capital per index contract would be 200.000 Euros real capital requirement (no leverage), and 1801 points after 10 weeks would mean about 9000 Euros gain after one year on 200.000 Euros capital = 4.5 %. Not so bad, but not that good, either.

Thanks @XORANDNOT but it seems we can’t select previous period as you can see on the picture (PRT 11.1)

Example : If you want to do a backtest from August, 2010 to December, 2014, enter August, 01, 2010 on the left hand side first, and then December, 31, 2014 on the right hand side.

Thanks, but I don’t succeed (I can’t select 2010 for example)

Does someone does ?

Yes excel. Now with totals

Thank you. How much would have been the purchase price for all of these algos to get the 1801 points total ?

And how much is the total capital exposure ? 20 algos * 10.000 Euro (very roughly) capital per index contract would be 200.000 Euros real capital requirement (no leverage), and 1801 points after 10 weeks would mean about 9000 Euros gain after one year on 200.000 Euros capital = 4.5 %. Not so bad, but not that good, either.

If you do it with the usual leverage at IG, you pay about 5000 Euros overnight fees (assuming that there is a position open every night) on 200.000 € total capital, plus 2500 Euro purchase price for all 20 algos. In this case, 9000 Euro gain become 1500 Euro after one year, or 75 Euro per contract and algo. Estimated very roughly for one contract per algo.

Thanks, but I don’t succeed (I can’t select 2010 for example)

Click “first date available” and “last date available” first and then try to enter dates manually. For me, it works, at least for small time scales such as 1 or 2 minutes, on DAX (Germany 30).

Maybe it depends on the instrument. If there are no tick-by-tick data then you can’t select the dates, I think.

Thanks, but I don’t succeed (I can’t select 2010 for example)

Does someone does ?

Do you have the PRT premium version ? The normal IG version (“PRT complete”) will give you only 100.000 or 200.000 bars backwards, not the entire time until August 2010.

Yes excel. Now with totals

Thank you. How much would have been the purchase price for all of these algos to get the 1801 points total ?

And how much is the total capital exposure ? 20 algos * 10.000 Euro (very roughly) capital per index contract would be 200.000 Euros real capital requirement (no leverage), and 1801 points after 10 weeks would mean about 9000 Euros gain after one year on 200.000 Euros capital = 4.5 %. Not so bad, but not that good, either.

If you do it with the usual leverage at IG, you pay about 5000 Euros overnight fees (assuming that there is a position open every night) on 200.000 € total capital, plus 2500 Euro purchase price for all 20 algos. In this case, 9000 Euro gain become 1500 Euro after one year, or 75 Euro per contract and algo. Estimated very roughly for one contract per algo.

You would not need that much, for most of the algos you will have enough with £ 2 K. Some of them £ 1 K is enough. Combining all of them together with the suggested position size, you could also reduce your total capital. I have not done the final calculation but £ 10 K is probably enough for all algos.

Regarding backtesting one can also argue that going back before 1 August 2010 , reduces the validity of the backtesting as there isn’t tick by tick data availability prior that date.

Thanks, but I don’t succeed (I can’t select 2010 for example)

Does someone does ?

Do you have the PRT premium version ? The normal IG version (“PRT complete”) will give you only 100.000 or 200.000 bars backwards, not the entire time until August 2010.

I am also unable to select 1-Aug-2010 for DAX M2 (for example). I have premium version.

When selecting the initial 1 M records , PRT will return a number slightly smaller than 1 M , saying these are all available data. Goes back to 15-May-2015.

Trying to change the dates from 1-Aus-2010 to 15-May-2015 , I am getting an error (in tick mode or not)

If you do it with the usual leverage at IG, you pay about 5000 Euros overnight fees (assuming that there is a position open every night) on 200.000 € total capital, plus 2500 Euro purchase price for all 20 algos. In this case, 9000 Euro gain become 1500 Euro after one year, or 75 Euro per contract and algo. Estimated very roughly for one contract per algo.

You would not need that much, for most of the algos you will have enough with £ 2 K. Some of them £ 1 K is enough. Combining all of them together with the suggested position size, you could also reduce your total capital. I have not done the final calculation but £ 10 K is probably enough for all algos.

Capital with leverage and real capital without leverage are two different things. You need to calculate the total return on investment based on the total capital when holding 1 contract. For 1 DAX, this is 14.650 € at the moment. You give IG 5% margin (or less, depending on your country) and borrow the rest, which you pay overnight interest for.

Your total risk is based on the real total capital on 1 DAX contract. When DAX loses 2% and you run into stop loss, you lose 2% of 14.650 €. When you calculate returns only on margin required, you deceive yourself.

1800 Euros return within 10 weeks on 20 contracts of 10.000 Euro total capital each are 4.5 % of 200.000 € within one year. Then you need to subtract capital cost (2.5% p.a.), because you trade on margin, and the algo price, of course.

I am also unable to select 1-Aug-2010 for DAX M2 (for example). I have premium version.

When selecting the initial 1 M records , PRT will return a number slightly smaller than 1 M , saying these are all available data. Goes back to 15-May-2015.

Trying to change the dates from 1-Aus-2010 to 15-May-2015 , I am getting an error (in tick mode or not)

Strange. For me, it works. May be you should call PRT and ask them what t do.

Thanks @XORANDNOT

I tried on demo version. I will try on premium version

But it’s strange you can, because it would mean you can backtest not on 1 million unit but on all historical unit 2010-2021

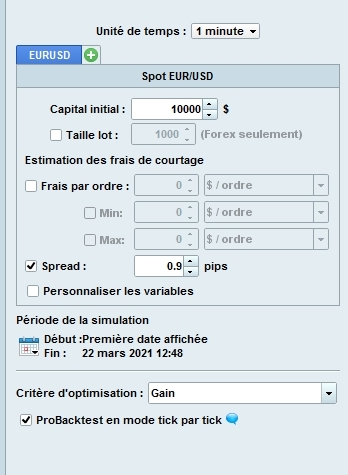

Whatever the strategy, can you do a copy of a backtest window with dates and a copy of the prices with unit, times and so on like on these pictures

Thanks and have a nice day

Regarding backtesting one can also argue that going back before 1 August 2010 , reduces the validity of the backtesting as there isn’t tick by tick data availability prior that date.

When you run a backtest in tick-by-tick mode, it starts automatically on August, 2, 2010 because there are no tick-by-tick data available prior to that date. Even when the detailed report still may show its faulty time scale.

because it would mean you can backtest not on 1 million unit but on all historical unit 2010-2021

Yes, you can backtest on all historical data back to 2010. Even on a 1 second time scale, if you wish (don’t know what this would show, however).